In more peaceful times it can be easy to forget just how fundamental energy is to the global economy. In fact I would argue that all economic activity is simply the transformation of energy, with virtually all of that energy aside from geothermal and nuclear coming from solar rays. Human labor of course is also ultimately powered by the sun, but that labor does not scale well – the explosion in technology in the last few centuries has been from our ability to take extremely dense forms of stored solar energy and transform it into things we wouldn’t have thought possible just a dozen generations ago – airplanes, computers, motor vehicles, etc. I have always taken it for granted that even when living through -30C winters on the Canadian prairies that I would have immediate access to fresh fruit grown thousands of kilometers away – something that would have been an almost impossible luxury even for royalty in previous centuries.

All this is to say that the transformation of dense energy stores is extremely important. And by far the most important sources of stored energy are hydrocarbons: primarily coal, oil and natural gas, which together power roughly 80% of global energy consumption. Of course the inexorable trade-off with these energy sources is that we are effectively relocating vast amounts of carbon from deep underground out into the atmosphere on an ongoing basis. And while non-hydrocarbon sources of energy are growing and our use of hydrocarbons is becoming much more efficient, there is currently no viable alternative to this energy source that is capable of sustaining the food and energy needs of 8 billion humans (not to mention the many vital materials we derive from hydrocarbons, from plastics to fertilizers to explosives to solar panels.)

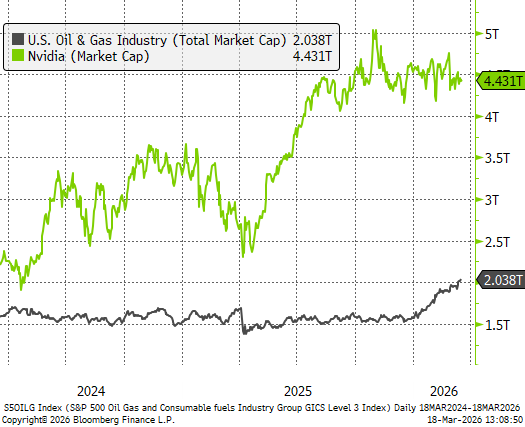

So with all this considered, one might reasonably conclude that the hydrocarbon industry underpinning the majority of the global activity must be absolutely enormous. In reality, “big oil” makes up a vanishingly small part of the global economy. The value of the entire U.S. oil and gas industry is less than half of just Nvidia. In fact up until a few weeks ago, Nvidia’s market cap alone was larger than the global oil and gas industry. This is a good reminder that monetary value is driven not just by utility but also scarcity. Oxygen and water are perhaps the two highest utility substances in the world, but for most people they’re essentially free because they’re not scarce.

Regardless of the reason why, it’s a fact that we place very little value on the initial steps of the energy transformation process (extraction and refinement), and a great deal of value on the latter steps of the energy transformation process (manufacturing, computation, etc). But as it is with water and oxygen, utility and value can tell two vastly different stories.

So what does any of this have to do with markets? In our view, the dramatic disconnect between the relatively high utility of stored energy and relatively low monetary value of extracting/refining this energy leaves the average investor exposed to one of humanity’s key recurring risks: war. I certainly won’t make the argument that the conflict with Iran is the start of a global catastrophe, and in fact the market is clearly seeing this as a transitory disruption. But it is nonetheless a vital reminder of the role energy exposure can play in diversifying some of the risk to assets from geopolitical violence.

As mentioned previously, the average North American investor has meaningfully less exposure to the entire energy sector than to any one of Nvidia, Apple, Microsoft, Google or Amazon. This means a key source of geopolitical diversification is missing from their portfolios. From 1980 through to 2020, the investing playbook said that long government bonds are the best protection in any kind of downturn. But this was during a 40 year period of gradually declining interest rates, and unless you think this will be repeated over the next 40 years (which would require rates to end up at -14%), then we simply cannot rely on what historical correlations tell us is a well diversified portfolio. We’ve seen that play out post-COVID: when the market declined in 2022, H2-2023, Q1-2025, and Q1-2026, long-dated bonds have been neutral at best, and is part of why we greatly prefer short duration bonds to long.

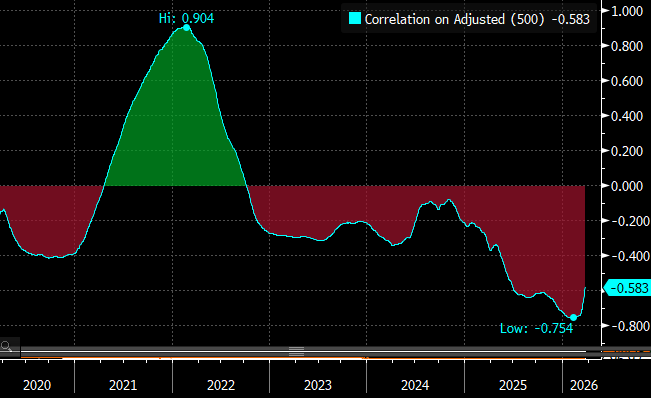

In contrast to long duration bonds, we’re seeing the energy sector increasingly step up as that diversifier in hard times, particularly when the threat to markets comes from violence or geopolitical conflict. This year it’s an especially acute effect given what’s happening with the Strait of Hormuz, but the same was true during the Russian invasion of Ukraine in 2022. The chart below shows the correlation between US stocks and the price of oil. When positive it means that the price of oil and stocks tends to move in the same direction, and vice versa for negative. The turning point was the Russian invasion of Ukraine – since then, the price of oil has been inversely correlated with the performance of the stock market, and has provided a great deal of diversification for investors who are overweight the sector.

It certainly doesn’t hurt that this is a sector that enjoys high cash flows and relatively modest capital expenditure needs, particularly here in Canada where our extraction assets have extremely long depreciation schedules. For this reason an overweight position in energy is something we believe should be present in any well-diversified portfolio, both for the geopolitical risk mitigation and the quality of underlying businesses.

The takeaway from all this is that most investors only think about the energy sector when it becomes scarce or is disrupted, and underappreciate its importance in times of abundance, peace and stability. But despite its relatively small presence in stock markets, energy extraction is the crucial first step in the energy transformation process that underpins global economic activity, and portfolios should reflect this reality. Ensuring appropriate exposure to this sector is one of the key ways investors can improve portfolio resilience in an increasingly uncertain world.