Many of us have heard the expression that the most dangerous phrase for investors is “it’s different this time.” It’s true that markets have a bad habit of ignoring history and making similar mistakes to those in the past, particularly as it pertains to excessive optimism, FOMO, and falling into the illusion that “valuations don’t matter.” However, the reverse is also true, and saying “this time is never different” can be just as dangerous. The truth of course is a painfully obvious middle ground – that investors need to adapt to a rapidly changing world without forgetting the lessons of the past.

This is about as insightful as saying something like “the Blue Jays either will or will not win the World Series,” but it’s still worth remembering that successful investing requires maintaining balance between these two investing dynamics.

With that in mind, the trends we are “following” are themes that have made it into mainstream investing discourse, but which we believe are still in the early innings and have further to run. Trends we are “fading” are themes we believe have run their course or are likely to hit an inflection point soon – we believe investors should avoid exposure to those themes.

Debasement – Follow

Debasement can be thought of as the cousin of inflation, except it’s less well understood and arguably even more important. Debasement is the phenomenon of a constantly growing money supply that reduces the value of currency relative to scarce assets (land, commodities, intellectual property) or productive assets (stocks, private business ownership, income generating real estate). Inflation is the reduction in purchasing power for the things we buy as consumers.

These two concepts are closely linked but are not the same. For example the period following the Global Financial Crisis saw a great deal of debasement, but very little inflation: things like gold, real estate, tuition, and professional services increased significantly in price in the years following the GFC, even though the overall inflation basket rose at an unusually slow pace. You can read our June Capital Currents for a more fulsome view on the nature of debasement.

Debasement certainly isn’t a new concept – in fact it’s the central concept underpinning the financial system of all developed markets. Nonetheless, the prospects for debasement have accelerated considerably since Trump’s inauguration, despite the brief period in Q1 of last year where Trump was pursuing an austerity platform (spending cuts, raising taxes via tariffs). Trump is still using tariffs as a lever to extract concessions from trading partners, but the magnitude of these tariffs is just a small fraction of what it was 9 months ago.

Trump will be choosing Fed Chair Jay Powell’s replacement in just a few months. One of the top 2 candidates is Rick Rieder, who just a couple weeks ago spoke at an internal DS conference. Whoever Trump appoints is very likely to continue easing monetary policy through rate cuts, but at the conference Rieder made comments about the importance of getting the 10-year yield down (which rate cuts impact only indirectly). Kevin Warsh or other potential Chair nominees are also likely to emphasize getting long term yields lower. Directly impacting long term yields requires much, much more force than simply bringing down short rates, and we put a high probability that de facto money printing from the Fed accelerates in 2026, and is a key reason why we believe portfolios must be well positioned to protect against and take advantage of higher debasement and inflation than what we became used to in the post-GFC period. Scarce assets such as gold are a vital diversifier in a world of accelerating debasement.

Gold and silver have been the most obvious beneficiaries of the debasement trade

Source: Bloomberg

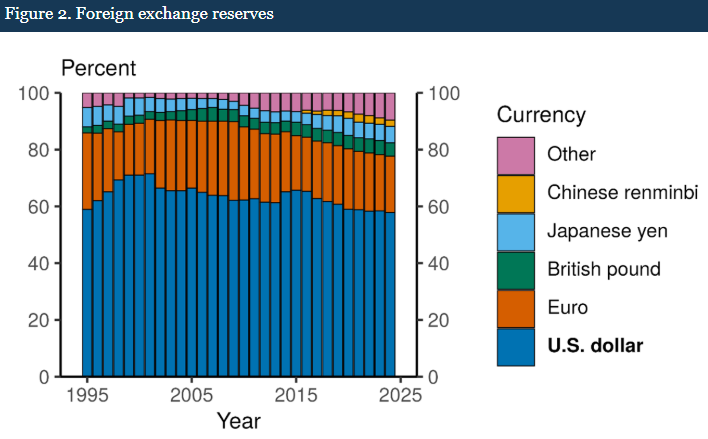

From a Unipolar to a Multipolar World – Follow

Prime Minister Carney generated some attention with his speech at Davos this week, stating that “the old order is not coming back.” We agree with this assessment, and we believe Trump does as well – the role that the U.S. plays in global socioeconomic and geopolitical affairs is shifting. We certainly do not see anything overtaking the US dollar as the world’s reserve currency, or that previous geopolitical alignment is going to break into a highly fractious set of dynamic alliances. Nonetheless, it’s clear that things are changing, and that both sides of the American electorate are increasingly rejecting the externalities that come from being the “center” of the financial and military world.

This ongoing shift forms a significant part of our view on the relative attractiveness of international equities over US counterparts. Trump is constantly testing every constraint of the established political orthodoxy, including the extremely top-heavy nature of NATO’s military might. As a result, international governments are rapidly increasing their own fiscal deficits and military spending, and those among you who have read our content in the last two years know just how important we think fiscal deficits are as a booster for markets; after all, the public sector’s deficit is the private sector’s credit (and is paid for by inflation, ultimately). Although international markets have outperformed the US by a considerable margin in the last twelve months, the much more forgiving starting valuations in the former means we still believe this trend has further to run.

Foreign central banks have been slowly but consistently shifting away from the dollar

Source: Federal Reserve

Fundamentals and Valuations Don’t Matter – Fade

After any period of strong stock market performance, a growing segment of investors manage to convince themselves that company valuations (i.e. how much you have to pay per dollar of profit to buy a share in a company) don’t matter. If there’s one thing market history has taught us, it’s that fundamentals (margins, growth, competitive moat) and valuations (P/E, P/S, EV/EBITDA) will always matter. Imagine being either a seller or buyer of a private company and saying to yourself “the price doesn’t matter, I just need to get this transaction done at any level.”

It’s as ridiculous to maintain this position in publicly traded equities as it is in a private business transaction, yet without fail this chorus of delusion appears from a segment of investors after every period of FOMO-driven euphoria, including now. We are firmly fading this trend, and you can read our October Capital Currents for a deeper look at how we think about valuations.

Non-profitable tech has underperformed since 2018 despite significantly higher volatility

Source: Bloomberg

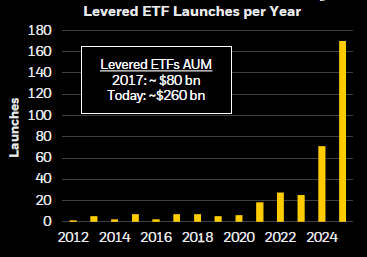

Gamblification of Markets – Follow & Fade

We’re cheating a bit by labeling this as both a fade and follow; the nuance is that we do think increasing levels of gamblification in markets (Robinhood day trading, 0-day options, meme-stocks) will continue in 2026 and beyond, but we feel very strongly that portfolios must be protected against this trend. Memestocks (think Gamestop, or more recently GoPro, Microstrategy, Beyond Meat, or Palantir) are legitimate companies that generate real sales (excluding Microstrategy) but become part of an online investor group that trades purely on hype rather than fundamentals.

The contract undertaken by investors is that you assume risk in return for a positive expected return in the long run; with memestocks and gamblification this relationship is turned on its head, and what you’re left with is plenty of risk with very little prospect for positive returns based on the fundamental realities of the underlying business. Gambling of course can be very profitable in the short-run (and vice versa), but without the long-term positive expected return. Our job is to invest on our client’s behalf, not to gamble or speculate, so we think it’s crucial to avoid the parts of the market that trade in this manner. Simply excluding this segment of the market can reduce the volatility of returns without giving up long-term projected growth. We anticipate writing a deeper review of this trend in a future newsletter.

Levered ETFs have exploded in the “gamblification” age of investing

Source: Blackrock

Closing Comments:

Investing is an act that is inextricably linked with the nature of uncertainty, and we should welcome that fact. After all, if there was no uncertainty, there would be no opportunity; just a single, unchanging, and relatively low risk-free rate of return on all investments. This is a time of higher uncertainty than usual, whether that’s trade, geopolitical, economic, or fiscal policy related uncertainty. This makes diligent analysis of fundamentals even more important, particularly given the unprecedented levels of market concentration and a growing bifurcation between the high-end and low-end consumer. As investment managers, that analysis and constant skepticism is key to the success of our clients’ investments, and we’re always happy to go deeper into why we’ve chosen certain investments or allocations, whether that’s by geography, sector, or security, so please reach out if you have any questions or comments about your positioning.

Wait a minute – a review of major investing trends and I didn’t even touch on artificial intelligence!? Well for starters this theme has been beaten to death and the bull and bear views are generally well telegraphed by thousands of different market observers. Nonetheless, if you’d like to see our views on the AI trade, please read the November edition of Capital Currents.