Why Markets Feel Calm and Chaotic at the Same Time

We’re not even two months into 2026 yet we could make the claim that we’ve already seen a full year’s worth of economic and geopolitical headlines:

- US forces capture Venezuelan President Nicolas Maduro in a night-time raid

- Widespread violence erupts in Iran, with Trump building up forces in the region and threatening to depose the Khamenei regime

- Trump attempts to acquire Greenland, including a threat of military action

- US government shuts down partially twice over political disputes

- The Supreme Court strikes down Trump’s tariffs, but are partially reinstated immediately by the White House

- Kevin Warsh is chosen as the new Fed chair, whose views on balance sheet management differ significantly from his predecessors

This of course is in addition to the already existing potential flashpoints in Gaza, Ukraine, and Sudan, not to mention the sharp increase in cartel related violence in Mexico. It’s true that one of the more acute side effects of the Information Age is that a constant bombardment of news can make it feel as though the world is in a continuous state of upheaval and violence, even though data suggests we live in one of the most peaceful times in human history.

Nonetheless, there is no question that the first two months of the year have produced an unusual number of market-moving events. Yet markets have barely moved at all, with the S&P 500 having traded in a top to bottom band of less than 3.8% since the beginning of December. Even forward-looking measure of volatility are hovering at below average levels, despite a modest pick-up so far this year.

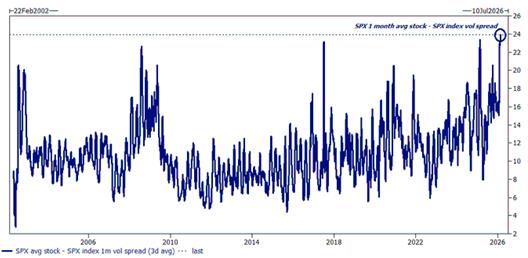

But beneath the surface of this ostensibly calm market is a flurry of volatility in individual stocks – for example the difference between the volatility of the average stock in the S&P 500 and the volatility of the S&P 500 itself is at a record high, as seen below.

In portfolio management these two types of volatility are delineated as “systematic risk” (the aggregate volatility in the stock market) and “idiosyncratic risk” (the volatility in any given individual name). What we’ve seen so far in 2026 is an unprecedented bifurcation between very low systematic/aggregate volatility and high idiosyncratic/individual volatility.

Well that’s all very jargony, you might say – but what does it mean? It means that investors in aggregate are relatively confident in the stock market, but when looking deeper are grappling with a great deal of disruption and sector rotation. The epicenter of this phenomenon is the software sector, which after being the darling of the market for the past three years is now down a staggering 32% in just four months. This software sell-off was accelerated by the release of an autonomous AI model developed by Anthropic designed to automate complex legal and administrative workflows. In our view, markets are taking these fears too far and are underestimating the potential for software companies to actually benefit from these tools.

Another notable example is the recent multi-billion dollar sell-off in trucking stocks, which began with an announcement from a company that previously manufactured karaoke machines, saying they had a developed an AI model that could significantly increase logistics efficiency. Clearly investors collectively are optimistic about the broad margin expanding potential of implementing new AI technologies, but at the same time are highly anxious about which industries may lose out from this shift. In our view, the market is more likely to overestimate the damage done from these disruptions and underestimate how long it will take these disruptions to become integrated.

In any case, the highly unusual dichotomy between low volatility at the aggregate level and high volatility at the individual level is notable, and passes the intuition check: things feel both calm and chaotic at the same time. Individual stock volatility is something we welcome as portfolio managers, since volatility is not only risk but opportunity – our objective as this bifurcation evolves is to look out for stocks where near-term panic is disconnecting the stock’s price from its fundamentals.