All eyes were on the U.S. Federal Reserve this past week. And, it did not disappoint, at least with respect to the buzz generated within the investment community. The Fed, as it is often referred to, appears to be preparing for a shift in its approach to monetary policy. While there was some weakness in bonds and segments of the equity markets, the most notable action occurred in the currency markets. We explain more below.

This past week, the Fed provided an update on its economic and inflation projections as well as the anticipated path it foresees for interest rates and bond purchases. Investors had been accustomed to a Fed that had to this point exhibited substantial patience and resisted the temptation to alter its approach despite a domestic economy that has improved and pricing pressures that have surfaced. As a result, some investors were surprised by the new estimates and comments released this week that suggest policymakers are preparing for a transition away from ultra-accommodative monetary policy.

The Fed’s projection for economic growth for the year was revised higher, but its inflation forecast saw the biggest boost, with the estimate now expected to be slightly above its preferred target through the next few years. Moreover, Chairman Jerome Powell acknowledged that while they still view the uptick in inflation as temporary in nature, there is the possibility it could be higher and longer lasting than expected. He indicated that committee members have begun to talk about when to start reducing their monthly bond purchases which they have been using as another means of fostering favourable financial conditions. Many expect a formal announcement of such a plan later this summer.

Not surprisingly, investors zeroed in on the fact that an increasing number of Federal Reserve committee members moved up their estimated timeline for interest rate hikes. Of the 18 members, 11 expect at least two rate increases in 2023, while 7 see rates potentially beginning to move higher next year, up from 4 members just a few months ago.

The reaction in the markets was noteworthy, particularly amongst currencies. The U.S. dollar rose meaningfully relative to most currencies, putting more pressure on some commodities that had already been weaker of late. But the U.S. currency still has a ways to go to unwind the underperformance witnessed against many currencies since last year. While it has some wind at its sails for now, an improving economic backdrop outside of the U.S. should be more supportive of other currencies.

In the grand scheme of things, the developments this past week were not too surprising. The economic wounds that arose last year have been closing, and the pending shift in approach of the Federal Reserve, and other central banks for that matter, reflect a return to a more normal environment, which should come as a relief to many. Nevertheless, interest rate hikes over the next number of years, should they occur, increase the odds of entering an environment where access to credit becomes more difficult. Most major market declines have coincided with recessions, and most recessions have occurred when financial conditions become restrictive. Thankfully, we envision a very gradual transition in monetary policy, and don’t envision those kind of conditions arising any time soon.

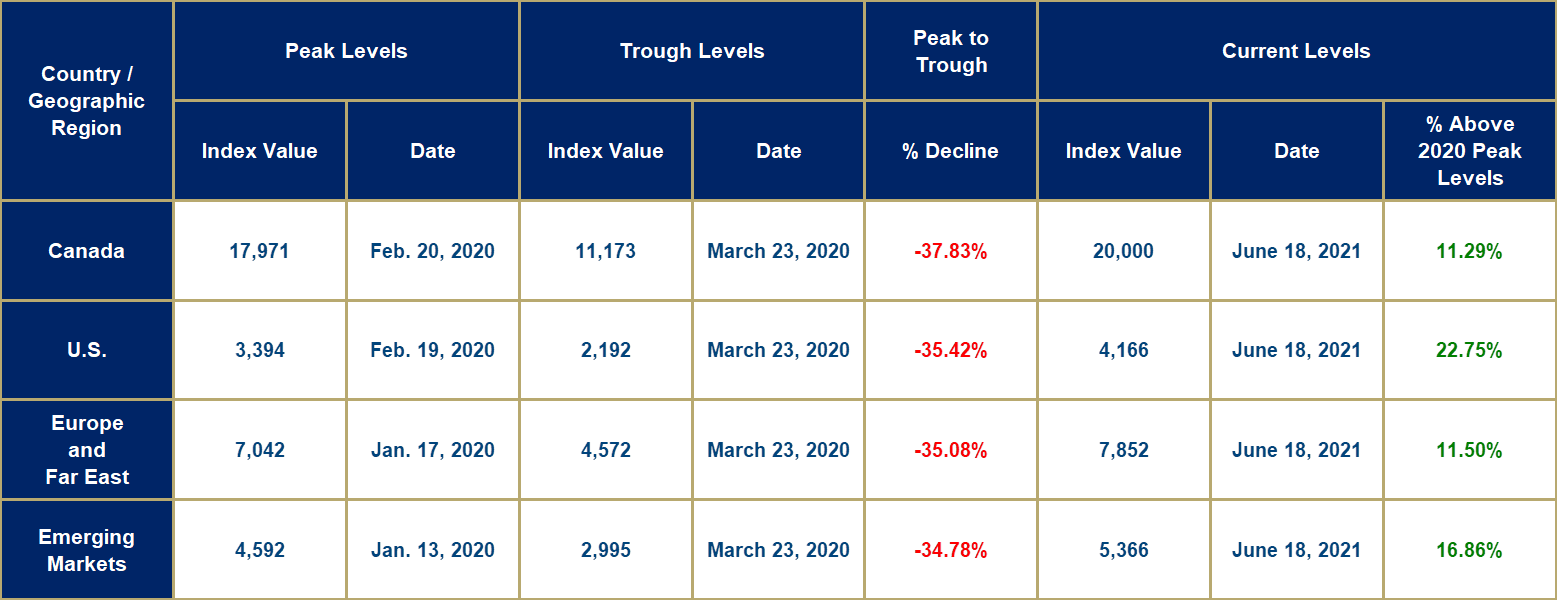

Market Decline and Recovery Results

The peak-to-trough numbers for the COVID-19 market decline and subsequent recovery are provided in the table below, as of today’s closing prices.