The upward pressure on bond yields that had been so notable of late was less pronounced over the past week, driven by a confluence of factors that we explain below. Meanwhile, trends on the virus front have deteriorated. The next wave of the pandemic may have less meaningful investment implications this time around given the rollout of vaccines, but it suggests the world is not quite out of the woods just yet.

Coronavirus Update

Frustratingly, the rate of new infections is increasing once again in some countries. In Canada, the 7-day average rate of new daily infections stands at over 3,000 for the first time in a month. The country’s largest province, Ontario, is mostly responsible as it has experienced a noticeable uptick in cases, driven largely by new variants of the virus. But, Manitoba has also seen an increase. Most other provinces have continued to see declines.

Meanwhile, parts of Europe are struggling to contain a third wave of the virus that is already well underway. Most notable has been Eastern Europe, with the Czech Republic, Slovakia, Hungary, and Poland all experiencing some of the largest infection rates in months. Even Italy and France are dealing with rising figures. Elsewhere, Turkey, India, and Brazil are all examples of other countries around the world that are contending with rising infection rates.

The U.S. continues to experience declines. However, the rate of improvement has slowed, and a few states are now seeing rising trends.

Bond Yields Face Some Resistance… For Now

Global bond yields faced a bit of resistance this past week, which provided some support to global equity markets and led some like the Canadian stock market to reach a new high for the year.

There were a number of factors at play that helped limit the upward pressure on bond yields. First, the inflation readings out of the U.S. for the month of February were relatively tame, which served to remind investors that the economy is still in the early stages of recovering and that any signs of pricing pressures have yet to materialize.

Secondly, the European Central Bank decided to take action to offset the recent move higher in bond yields by committing to buy government bonds at a faster clip, hoping to drive bond yields lower as a result. This adds to a similar decision undertaken by the Reserve Bank of Australia the week before. It underscores the notion that monetary authorities remain focused on ensuring that financing conditions – such as borrowing costs for businesses and consumers – remain very accommodative.

Lastly, bond markets were supported by a sizeable debt auction by the U.S. government that went reasonably well. Many governments are issuing increasing amounts of debt to fund the massive amounts of aid and stimulus that have been announced since the onset of the pandemic. This includes the $1.9 trillion stimulus package signed into law by the U.S. administration in recent days. The bond auction resulted in reasonably healthy demand from investors this past week, including large institutions such as pension funds for example.

Ultimately, markets were reassured to some extent that inflation is not yet an issue, central banks remain proactive, willing and able to intervene to counteract forces that could jeopardize an economic recovery, and there remains sufficient investor demand to absorb a growing supply of low yielding government bonds, despite inflation concerns.

We still expect markets to be tested in the months to come as inflation readings should rise as we lap the spring period from a year ago. The potential to overshoot inflation expectations in the near-term remains a possibility given the high amount of savings, pent-up demand, and new rounds of stimulus. Over the longer-term, we are less convinced that inflationary forces will prevail. As always, we remain vigilant and prepared for any additional market wobbles.

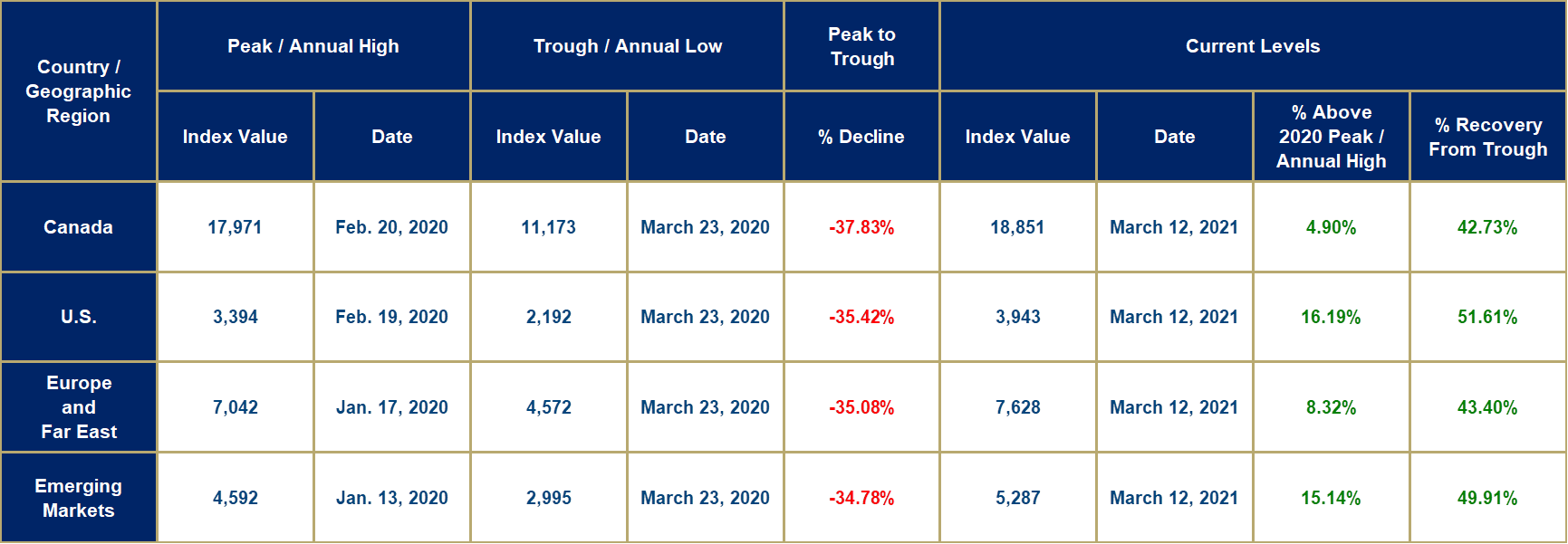

Market Decline and Recovery Results

The peak-to-trough numbers for the current market decline and subsequent recovery are provided in the table below, as of today’s closing prices.