The narrative in the global markets hasn’t changed much over the past few weeks. The volatility in bond markets, caused by growing inflation concerns, continues to be the central issue of focus for investors. This has led to some weaker equity market performance. More noteworthy has been the strong rotation out of certain sectors and groups of stocks and into others. We explain this phenomenon a bit more below, and provide a brief update on the virus.

Coronavirus Update

New daily infection trends across North America were somewhat mixed over the past week. Canada’s 7-day average rate of new daily infections stands at 2,900, roughly where it has been over the past few weeks. The meaningful rate of improvement witnessed over the past month has stalled. From a provincial perspective, Manitoba has witnessed the most meaningful improvement recently, while the East Coast has been mixed with slowing infections in Newfoundland and New Brunswick helping to offset higher new case levels in Prince Edward Island and Nova Scotia. Encouragingly, in the U.S., the 7-day average rate of new daily infections has dropped over the past week, with levels standing at just under 60,000, versus the 70,000 from the week ago period.

The Great Rotation

Global equities have struggled to make new highs over the past month. They have been weaker, driven by rising inflation concerns that have unleashed bond market volatility. The recent market weakness has been relatively tame as far as pullbacks go, and can be characterized by a meaningful rotation out of “growth” stocks that appeared to be on a never-ending run through recent years. Investors have instead been favouring some of the forgotten, less heralded, and in some cases unloved parts of the market (i.e. value stocks) that have been relatively “cheap” for some time, such as energy, base metals, financials, and even some pockets of retail and leisure.

This great rotation makes sense. After all, businesses such as restaurants, hotels, and stores should arguably benefit the most from an economy that may finally be able to reopen. Meanwhile, commodity prices have already rebounded and the potential for a normalizing global economy as the year goes on should help foster a demand recovery. Global banks may see a better operating environment too, fuelled by strengthening activity and improving lending margins as a result of higher bond yields.

On the flipside, so-called “growth” stocks have been under notable pressure. This group is far ranging, encompassing everything from technology businesses, internet-based and e-commerce companies, and virtually anything tied to climate and clean energy, among other things. While the growth outlook has likely not changed for these businesses, there is an appreciation that the potential rate of change and upside to earnings expectations will be demonstrably higher for the other sectors, at least while the economy is reopening. Furthermore, many growth stocks have done well in recent years, with their prices reflecting the attractive earnings growth that investors anticipate.

Another important, and sometimes underappreciated, factor with high growth stocks is their correlation to interest rates. They are arguably more sensitive to interest rates than other areas of the global equity market. This is largely a function of two issues. First, stocks are traditionally valued by projecting all future cash flows and discounting them back to a current value using what’s called a “discount rate” that is dependent on the level of interest rates. A higher interest rate would result in a lower present value of future cash flows, all else being equal, and vice versa. Secondly, high growth companies by nature have more of their value tied to cash flows that are expected to be generated years into the future. The further out those cash flows are, the more sensitive they are to interest rates. While varying levels of rates don’t necessarily change the earnings growth that a company will deliver in the years to come, they do heavily influence the present value that investors will ascribe to those future earnings.

We continue to think it remains premature to be concerned with longer-term inflationary pressures that could force central banks to raise interest rates. Nevertheless, we are mindful that near-term inflation readings are likely to tick higher, reflecting an economy that is reopening relative to one that was nearly shut in the year prior. Higher yields and concerns over inflation could remain a headwind for a while longer. And so, the great rotation may continue, with the potential that it over extends itself, as markets often do, testing the conviction level of investors.

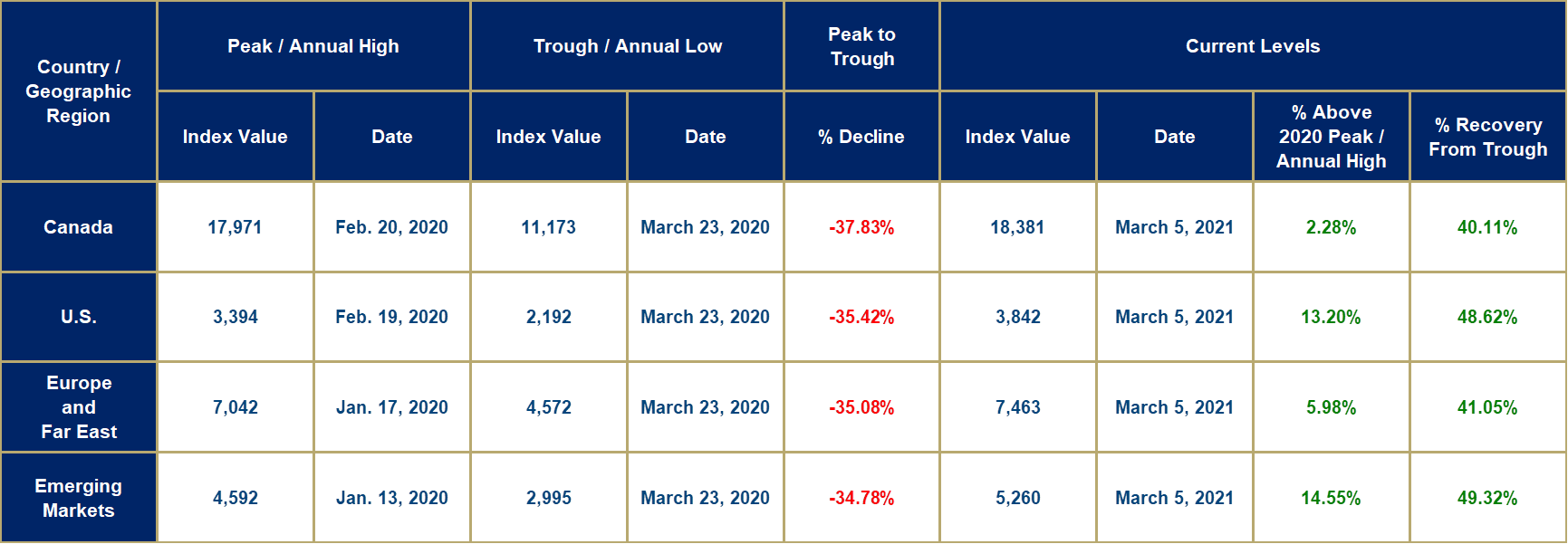

Market Decline and Recovery Results

The peak-to-trough numbers for the current market decline and subsequent recovery are provided in the table below, as of today’s closing prices.