It was another week in which markets made little headway, finishing roughly where they started. It was a week that served to remind investors that improvements may be met with setbacks, both with respect to the coronavirus and the economic recovery. We offer some key thoughts on the week that was.

Coronavirus Update

Seemingly, there was a reversal of fortunes this week with respect to global coronavirus trends. The U.S. experienced some stability in contrast to the rest of the world which has been faced with a resurgence.

Positively, the U.S. witnessed stable to modestly lower rates of new infections in some of its most populated states, including California. Notably, some states across the Midwest appear to be experiencing rising cases, though the levels are not alarming at this point. Overall, the average number of new daily cases across the country remains elevated at well over 60,000 – but, this level has not increased for the second week in a row. Unfortunately, the number of fatalities has been rising. While tragic, this is not surprising as deaths lag new infections. Encouragingly, the mortality rate remains well below the levels witnessed in the country months ago, despite infections being meaningfully higher.

Developments were less encouraging throughout the rest of the world. Elevated new cases remain a challenge across India, parts of Central and South America, South Africa, and Southeast Asia. This week was noteworthy for the increasing number of countries that appear to be experiencing relatively new outbreaks. The list includes Australia, Japan, China, Hong Kong, Vietnam, Belgium, Poland, France, Germany, and Spain, among others.

Company Earnings and Economic Wobbles

The second quarter earnings season is roughly half way complete. Thus far, results from companies in Canada, the U.S., and Europe have been in-line to slightly better than expectations on average, helping reassure investors to some extent. The large and growing technology sector has garnered a lot of attention and focus, and deservedly so, as results confirmed what many investors already understood – these companies’ business models are well positioned to deal with an environment that remains far from normal. Revenue and profits from companies across a range of industries also followed the positive trend of being as good as or better than investor expectations.

Despite the positive narrative, significant challenges persist. Many management teams suggested visibility remains limited and difficulties still lie ahead once government aid programs expire. Furthermore, many entrepreneurs with small and medium-sized businesses are struggling with restrictions imposed by governments and overall weak demand. Additionally, many don’t benefit from the kind of financial flexibility and workforce agility of some public companies. Furthermore, there continue to be signs that suggest the positive economic momentum is wobbling, particularly in the U.S. The number of people filing weekly jobless claims, which had been improving (i.e. declining) for many weeks, has stalled and has begun to reverse course over the past two weeks.

Pressure continues to mount on the U.S. government to come up with another round of stimulus. Finding some compromise is clearly proving to be more challenging than expected; nevertheless, we continue to believe some resolution will surface in the not too distant future.

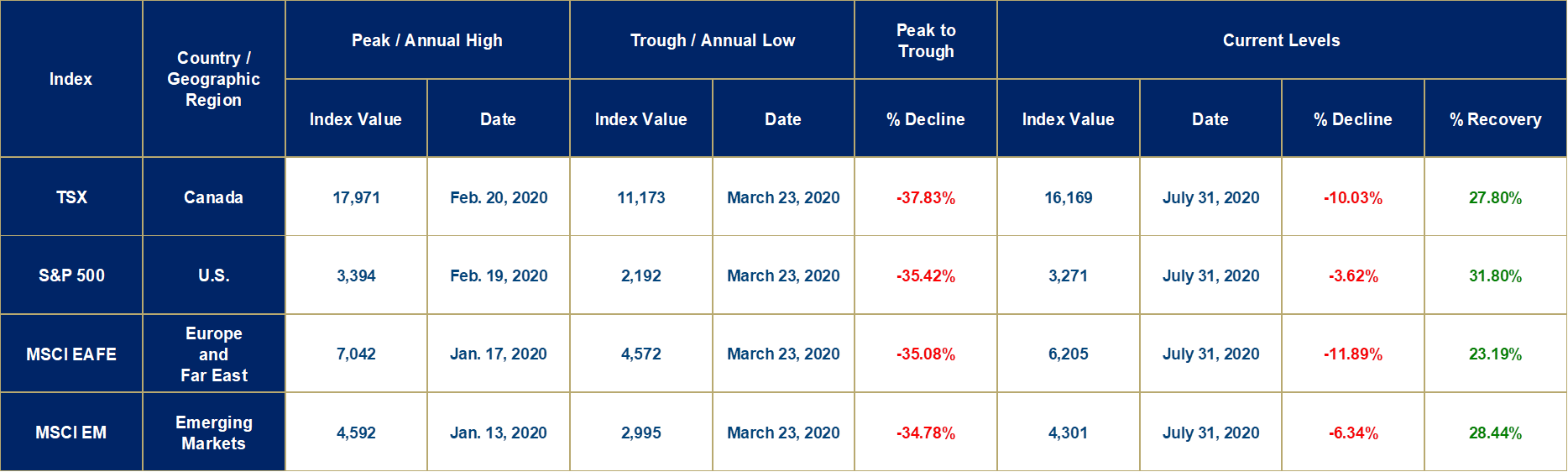

Market Decline and Recovery Results

The peak-to-trough numbers for the current market decline and subsequent recovery are provided in the table below, as of today’s closing prices. This week, markets were up slightly in Canada, the U.S., and the Emerging Market countries, while countries in Europe and the Far East were down marginally.

As always, if you have any questions or concerns, please don’t hesitate to reach out.

Warren