Equity markets have made up much of their lost ground since their March lows as COVID-19 infection and mortality rates have improved in North America and Europe, and as rays of light have started shining into the quarantine tunnel. Markets are anticipating major economies will reopen on a rolling basis sooner rather than later. The Federal Reserve’s unprecedented $2.3 trillion intervention into the U.S. credit market has also boosted equities, as it staved off what could have been a painful credit crunch.

But there are still some caution signals flashing. We examine the historic plunge in North America’s crude oil benchmark, which has weakened equity markets around the world in recent trading sessions. We also provide updated thoughts on the economic outlook for the U.S., Canada, and other major economies, along with what we see in store for global growth.

Crude oil: The perfect storm

Global economic crises—the COVID-19 pandemic certainly qualifies—often bring with them eye-popping and head-scratching knock-on effects. The collapse of North America’s crude oil benchmark is one for the ages.

For the first time ever, the futures contract for West Texas Intermediate (WTI) crude oil plunged into negative territory, settling at -$37.63 per barrel in New York on Apr. 20. It dipped below zero once again during the following trading session. In addition to the fundamental factors that pressured the market, there are some complex technical and financial dynamics that caused WTI oil futures to dive as the May contract headed toward expiration in what seemed to be a highly speculative, illiquid trading environment that was also challenged by physical oil storage constraints in the U.S. We think the fundamental factors behind the overall pressure on oil prices over many weeks, rather than the peculiarities of the WTI futures market during two days of trading, are more important for individual investors to grasp.

In our view, there are three key takeaways from the recent downward acceleration of oil prices. First, demand for crude oil, and for products such as gasoline and jet fuel derived from it, has collapsed due to the mass-scale shutdowns associated with the COVID-19 pandemic. Second, this collapse occurred when the oil market was already greatly oversupplied due to a lack of restraint by many major oil producing countries. Third, the combination of very weak demand and sky-high supplies means that physical storage capacity for oil is getting close to filling up or is already spoken for, and therefore storage has become very expensive, especially in the U.S. These factors weighed heavily on the WTI futures market in recent weeks, and could leave it—and other crude oil benchmarks—vulnerable over the near term until these pressures begin to ease.

RBC Capital Markets, LLC Commodity Strategist Michael Tran recently said that “COVID had just completely taken the oil market hostage and the near-term outlook continues to be quite grim.” Millions upon millions of people around the world are barely driving and have largely stopped flying due to COVID-19 shutdowns. For example, automobile traffic congestion is down by 84 percent in Chicago, and departures at Chicago O’Hare International Airport are down 74%. While these are temporary phenomena, the severe drop-offs in gasoline and jet fuel demand are replicated all over the U.S., as the tables below show, as well as in many other large cities around the world. This has led to significant global crude oil demand destruction. Anemic demand, combined with the unique features of commodity futures contracts and nearly full U.S. storage capacity at a time when significant cargoes of unneeded Saudi Arabian oil are heading toward the Gulf Coast, created the perfect storm that drove WTI oil futures prices to previously unthinkable levels.

While crude oil’s rapid descent began in March with a vicious production and price dispute between Saudi Arabia and Russia, that issue was overtaken weeks ago when COVID-19 shutdowns began to ravage oil demand, tilting the market far more out of balance than it already was. RBC Capital Markets’ commodity team anticipates the recent OPEC+ deal to cut oil production by at least 9.7 million barrels per day, which is set to take effect in May, will help diminish the supply/demand imbalance over time. There are already signs the cuts could be deeper and might even come sooner than originally advertised. Either way, it will take months to chew into the oversupply by any meaningful degree.

Tran believes the more important factor in getting the oil market headed toward a healthy state of equilibrium will be the timing and magnitude of oil demand recovery as governments lift COVID-19 restrictions on a rolling basis in many cities and countries. In a recent audio interview for our clients, Tran said, “The bottom line is that the U.S. inventory potentially filling to the brim over the course of the next month or so is almost like watching a slow-motion car crash. You know it’s coming. Inventories are rapidly filling. We need to turn off the [oil production] taps before the bathtub overfills. And whether that comes from government policy or from free markets given how weak oil prices are, either way until something happens—i.e., the U.S. production rolls [declines] hard or COVID clears in the coming weeks, which seems unlikely—oil prices will remain extremely challenged over the near term.”

As economies open up and people return to work and day-to-day life amid the relaxing of COVID-19-related constraints, Tran expects global demand to pick up. It is worth noting that weekday traffic congestion in major Chinese cities is back up to pre-outbreak levels (although weekends remain quiet). Following a turbulent period, his crude oil forecast calls for improvement in the second half of this year and better conditions in 2021 as supply cuts come into effect and demand strengthens. Tran sees the WTI and Brent crude oil benchmarks averaging $35.25 and $38.75 per barrel, respectively, in the second half of 2020. For 2021, he believes the benchmarks will rise to averages of $43.77 and $46.14 per barrel, respectively.

Vehicle traffic congestion, major U.S. cities

U.S. cities: COVID-19 shutdown vs. 2019 traffic congestion

| City | Deviation from normal |

|---|---|

| New York | -93% |

| San Francisco | -86% |

| Chicago | -84% |

| Boston | -81% |

| Los Angeles | -79% |

| Dallas | -78% |

| Houston | -78% |

| Atlanta | -77% |

| Seattle | -75% |

| Denver | -63% |

Source - RBC Capital Markets, TomTom

Flight cancellations by major U.S. airports

U.S. cities: Flight departures

| Airport/city | Deviation from normal |

|---|---|

| John F. Kennedy Intl. Airport (New York, NY) | -87% |

| McCarran Intl. Airport (Las Vegas, NV) | -82% |

| Houston Bush Int’ctl. Airport (Houston, TX) | -81% |

| San Francisco Intl. Airport (San Francisco, CA) | -79% |

| Hartsfield-Jackson Intl. Airport (Atlanta, GA) | -77% |

| Los Angeles Intl. Airport (Los Angeles, CA) | -75% |

| Chicago O’Hare Intl. Airport (Chicago, IL) | -74% |

| Dallas-Fort Worth Intl. Airport (Dallas, TX) | -69% |

| Seattle-Tacoma Intl. Airport (Seattle, WA) | -69% |

| Denver Intl. Airport (Denver, CO) | -68% |

Source - RBC Capital Markets, FlightAware

How do you spell relief?

Crude oil demand destruction is just one indication that major economies are facing serious challenges from COVID-19. There is much debate among market participants about whether the pandemic-driven economic recession and recovery will be shaped like a “V,” a “U,” a “W,” or some other letter. Rather than fixate on letters, we are mindful that there are still a lot of uncertainties about the duration of the downturn and the trajectory of the recovery.

RBC Global Asset Management Inc.’s Chief Economist Eric Lascelles said, “The economic recovery is likely to be sluggish for a mix of artificial reasons (governments will only be able to partially restart economies) and natural reasons (skittish post-quarantine demand) … On the aggregate, we feel slightly better about the COVID-19 situation than a week ago, but the prospect of a sluggish recovery is both serious and unwelcome.”

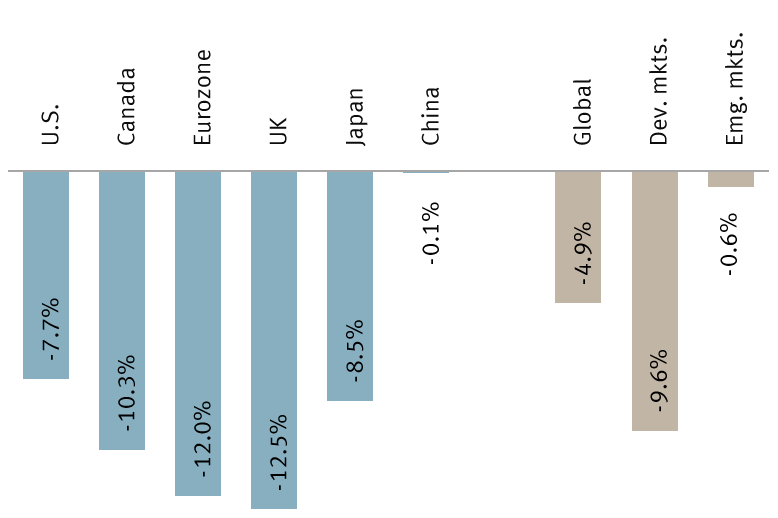

Lascelles’ expectations for the U.S. haven’t changed in the past few weeks: a deep and brief recession is likely. But at least his forecast hasn’t worsened. He still anticipates that GDP will briefly decline by 20 percent from peak to trough, and the decline will last for 12 weeks, largely due to COVID-related shutdowns (we’re already partway through this process). This brief hit to growth, combined with the beginning of a recovery soon thereafter, would leave full-year 2020 GDP down by 7.7 percent—the most severe retrenchment since 1946.

Lascelles anticipates other large economies will come under greater pressure. In a comprehensive weekly report, he wrote, “The U.S. economy does the best of the developed world by virtue of its superior sector mix, lighter quarantine and aggressive stimulus. Japan also does well, mainly because of its extremely light quarantine. Conversely, the eurozone and UK are hit worst of all due to their much stronger quarantining … While Canada’s forecasted peak-to-trough decline of 23 percent and a 2020 GDP forecast of -10.3 percent growth are substantially worse than the U.S, this is for good reason as Canada has enacted more aggressive quarantining than the U.S. and has a less helpful sector mix. Embedded within this sector mix is Canada’s outsized oil sector pain.”

These declines and retrenchments in other countries, if realized, would drag down global growth by 4.9 percent in 2020. By way of comparison, this global growth decline is deeper than the International Monetary Fund’s estimate of a 3.0 percent pullback.

RBC Global Asset Management’s 2020 annual GDP growth forecasts

Annual average % change according to a medium-depth and medium-length recession scenario

Dev. mkts. = Developed markets; Emg. mkts. = Emerging markets

Source - RBC Global Asset Management; estimates as of 4/17/20

Conclusion: Stay alert

We think the combination of lingering economic uncertainties and historic instability in the crude oil market argues for keeping some powder dry. We continue to recommend holding equities at the Underweight level in portfolios for the time being—this is below the long-term strategic recommended level.

While it appears that market participants are bracing for harsh recessions in many large economies, it’s still unclear to us whether they are accurately estimating the magnitude and duration of the downturns. Perhaps even more importantly, it is not yet clear whether they are gauging the recovery trajectory properly. There are still many COVID-19-related challenges that could come into play as economies reopen.

Non-U.S. Analyst Disclosure: Jim Allworth, an employee of RBC Wealth Management USA’s foreign affiliate RBC Dominion Securities Inc. contributed to the preparation of this publication. This individual is not registered with or qualified as a research analyst with the U.S. Financial Industry Regulatory Authority (“FINRA”) and, since he is not an associated person of RBC Wealth Management, may not be subject to FINRA Rule 2241 governing communications with subject companies, the making of public appearances, and the trading of securities in accounts held by research analysts.

In Quebec, financial planning services are provided by RBC Wealth Management Financial Services Inc. which is licensed as a financial services firm in that province. In the rest of Canada, financial planning services are available through RBC Dominion Securities Inc.