Quarterly Commentary as of March 31, 2022

2022 began as a year of transition. That is to say, interest rates starting to rise, governments beginning to reduce financial assistance programs and an economy which beginning to slow after a year of extraordinary growth. In other words, the initial stage of the recovery (exit from the crisis) is over and we are now in the middle of the economic cycle. This 2nd phase is characterized by economic growth, albeit at a more normal pace.

Since the beginning of the year, the elephant in the room has definitely been inflation and its implications. When inflation rises, interest rates rise and therefore wages must increase enough for consumers to maintain their purchasing power. Currently, salaries are increasing but net salaries adjusted for inflation have decreased over the last 4 quarters. By raising rates, the central banks’ objective is to curb inflation and restore equilibrium. Central banks will attempt a soft landing. That is, to raise rates without causing too severe a slowdown that could ultimately lead to a recession.

To account for this transition, we reduced equity weightings at the beginning of the year, favored dividend-paying stocks and strengthened the fixed income portion of client portfolios by increasing credit quality.

We expect markets to recover in the second half of the year, once the economy has digested the rate hikes and if central banks manage to regain control of inflation. With a record job market, earnings of good quality companies should continue to grow in 2022.

Leading economic indicators remain favorable for North America; the Canadian economy is expected to grow at a rate of 3.6% in 2022 and the American economy continues to operate at full speed as well.

On the other hand, the outlook is much more nuanced for Europe & Asia. Europe is vulnerable in a context where the price of raw materials remains high and the input shortage disproportionately affects the automotive industry. Moreover, the repercussions of the war in Ukraine spill over the borders and other countries importing raw materials, including Japan, India and China, all of which are suffering the backlash. Another impact to consider, China with its zero COVID policy is facing a surge in cases of the Omicron variant. Containment measures are back and it is reported that 40% of its population aged 80 and over are not yet adequately vaccinated.

At the portfolio level the rapid rise in interest rates, especially in March, had a negative effect on the market value of fixed-income securities. For your information, the Canadian fixed income benchmark has an average duration of 7.5 years and its performance from the beginning of the year until March 31 was (-7.0%). As for our fixed income strategy at Senay Marrocco Group, our positioning was a shorter duration in anticipation of rate hikes. The average duration of our fixed income portfolio was 3.8 years, which enabled us to achieve a better relative performance compared to the benchmark.

Here is why a drop in fixed income market values is normally temporary, not permanent.

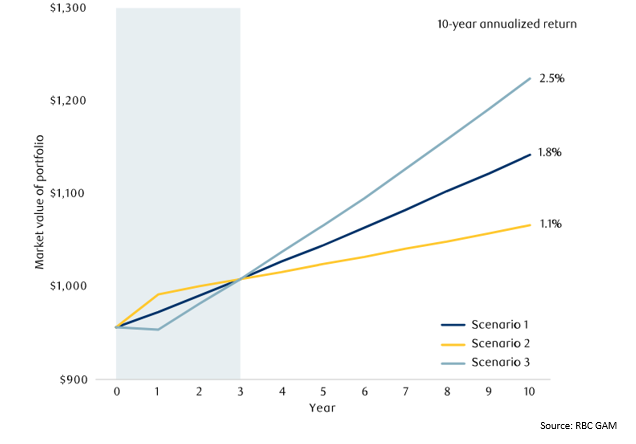

We can chart out the total return potential you’d see if you invested under each of the following scenarios we’ve created. Currently, we are experiencing scenario 3.

- Scenario 1: Yields remain unchanged (dark blue).

- Scenario 2: Yields fall by 100 bps across the curve during Year 1 (yellow).

- Scenario 3: Yields rise by 100 bps across the curve during Year 1 (light blue).

The rising rate portfolio in scenario 3 experiences an initial decline in value as rates rise. However, as time passes, the portfolio hurt by rising rates begins to perform more strongly, while the portfolio that experiences a drop in rates falls behind the original portfolio.

This is because over time new bonds are purchased at higher yields and so the portfolio earns more income than it would have under a scenario where rates remain unchanged. In a scenario where yields drop, the assets are reinvested at lower rates and therefore earn less over the full lifespan of this investment.

These three scenarios may be simplistic. But they highlight how fixed income portfolios can benefit from rising rates over time as the portfolio is reinvested. Although it may be unsettling to see negative rates of return on bond portfolios when yields are rising, having an adequate time horizon and reinvesting at higher rates can be beneficial to overall fixed income returns.

Performance at March 31 2022

The results in CAN$ of the various indices for the quarter ending March 31, 2022: +3.8% for the Canadian S&P/TSX index (positive influence of the commodity weighting), (-5.6%) for the US S&P 500 index and (-7.6%) for the Europe-Asia-Far East index. In fixed income, the benchmark FTSE TMX Canadian Bond Index posted a negative return of (-7.0%). The appreciation of the Canadian dollar against the US dollar had a negative impact of (-1.1%) on US strategies over the same period. Canadian dollar results for a balanced portfolio are around (-3.05%) for the last three months and balanced portfolio returns over the last twelve months are generally between +6% and +7% in CAD. Relatively, the iShares balanced benchmark returned (-5.29%) for the first quarter and +3.56% for the last twelve months.

Spring 2022 Discussion with Jim Allworth

On April 12, Jim and I had a discussion on various current topics such as inflation, the real estate market, the conflict in Ukraine, the coming economic slowdown, the Canadian dollar, and beyond the events that influence the stock market in the short term, what the long-term considerations for investors to bear in mind are. Jim gives us insights from RBC economists and strategists. I therefore invite you to watch the interview and kindly note that the complete transcript will follow shortly.

Please contact us with any questions or comments. Happy spring and thank you for your continued trust.

Mathieu, Roberto and Anthony

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that action is taken on the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / ™ Trademark(s) of Royal Bank of Canada. Used under licence. © 2022 RBC Dominion Securities Inc. All rights reserved.