This report is part of the “New normal, new opportunities” series, in which we examine secular trends in a post-COVID-19 world. The series will cover a range of themes that are emerging as a result of social distancing, the work-from-home imperative, health care developments, corporate implications, and broader societal change. We believe identifying these trends and understanding their investment implications will be critical to navigating the road ahead. Additional reports will be released over the following weeks.

The novel coronavirus has also given rise to novel and unprecedented global economic conditions. This is the first time in modern history that the world economy has effectively been placed in an induced coma. With no real playbook on how to deal with this, governments and their central banks have fallen back on the simplest solution—to shower their economies in money.

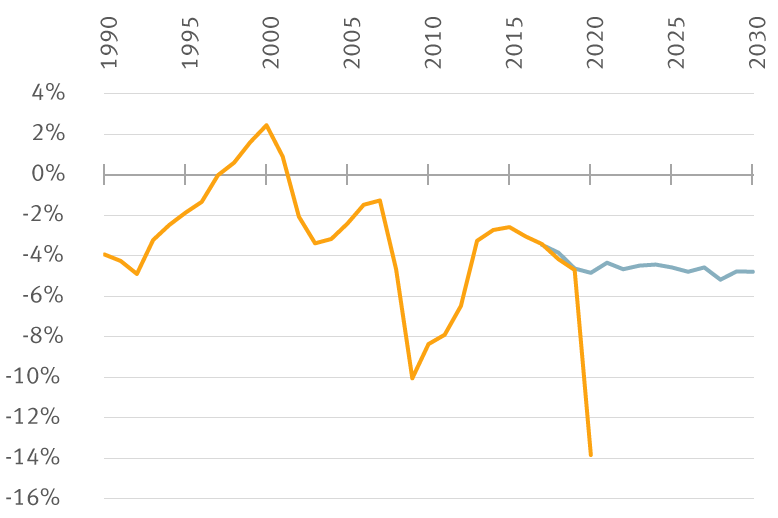

The fiscal response has been fast, large, and widespread. The U.S. was arguably the first developed nation to open the spigot, but its peers followed suit in short order. In 2017, the Congressional Budget Office (CBO) projected an ongoing annual U.S. fiscal deficit of about five percent of GDP. The CBO was correct for the first two years, but the 2020 deficit is now likely to come in closer to 14 percent of GDP.

The CBO forecasts now look a little optimistic

Deficits as percentage of U.S. GDP

Source - Congressional Budget Office, RBC Wealth Management

The U.S. government has had little difficulty financing or rolling over this debt so far, since it’s far from the only country doing this, and foreigners have an appetite for U.S. bonds. But that may usher in a problem further out if overseas investors sour on Uncle Sam. This is because U.S. net external debt is now 55 percent of GDP compared with only nine percent in 2007.

To be sure, fiscal largesse is the right strategy to support an economy in recession. But questions remain. How will this overspending impact the economy as we pull out of recession? Can we get back to balancing the books? What are the long-term implications?

The fiscal packages implemented to deal with COVID-19 will significantly increase the debt levels of most countries. For the developed OECD (Organization for Economic Cooperation and Development) economies, the World Bank projects aggregate public debt to rise from 109 percent of GDP in 2019 to 137 percent in 2020. Typically, academic consensus views debt levels above 90 percent of GDP to be harmful to long-term growth. We believe it’s highly unlikely that governments will implement austerity programs or spending cuts after the pandemic is over, so the default response is more likely to be higher taxes, financial repression, or creative accounting.

The easiest targets for higher taxes are likely to be foreign or multinational companies with overseas income streams. But this runs the risk of tit-for-tat tax hikes on domestic companies, which will probably face political pushback.

So we believe a combination of higher taxes and continued low interest rates may be the most likely prescription. Governments can get away with lower interest rates over the medium term, as aging populations suggest there is continued demand for income-based investment vehicles, which means that bond issuance tends to get snapped up even at historically low coupon rates.

Over the near term, COVID-19 is a disinflationary shock given high spare industrial capacity and high unemployment. But over the longer term, it may act as an inflationary shock due to a combination of higher government spending and trends toward deglobalization. Additionally, higher money supply tends to lead inflation by 2–3 years under normal conditions. Although we see no current inflation pressures, if this were to change, excessive debt loads could effectively be inflated away, although rolling over the debt would become more expensive.

While increasing the debt loads of individual countries in isolation would typically weaken their currencies, the picture is less clear when everyone is doing it. Instead, we would look to relative trends in fiscal deficits to drive currency moves. But if a country starts to meaningfully address its deficit, it would likely be rewarded with an appreciating currency, which would harm its competitiveness. For this reason, we expect a global standoff in deficit reduction until the first country blinks.

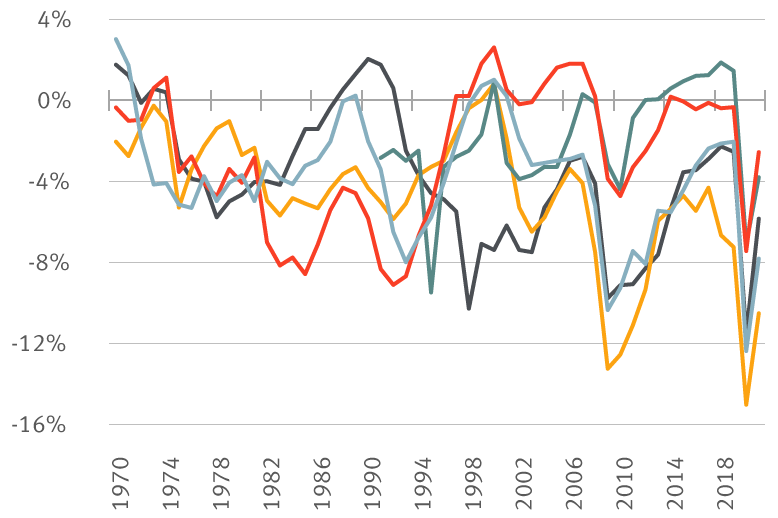

Welcome to the party: Developed nations spending heavily

National fiscal deficits as a % of GDP

Source - Bloomberg, RBC Wealth Management

And if any country can get away with deficits for longer, it’s likely to be the U.S., due to the reserve currency nature of the dollar. Currently, 62 percent of global foreign exchange reserves are in dollars, while the next largest competitor currency, the euro, only accounts for 20 percent of global reserves. Given the liquidity of the U.S. bond market, we don’t expect the greenback to surrender its reserve currency status anytime soon.

Ultimately, high fiscal deficits and debt loads are a political issue, rather than an economic one. As such, it will likely be addressed in a political fashion—by dealing with it when politicians get voter pushback. Given the widespread increase in government deficits globally, and the disincentive to be the first to cry “uncle,” we don’t think that’s likely to happen soon.

This article was originally published on Aug. 31, 2020

In Quebec, financial planning services are provided by RBC Wealth Management Financial Services Inc. which is licensed as a financial services firm in that province. In the rest of Canada, financial planning services are available through RBC Dominion Securities Inc.