The long-term secular outlook for U.S. equities remains constructive, with generational expansion cycles suggesting the upside could extend into the mid-2030s. Based on historical precedents from prior secular bull markets, the structural trend remains supportive of materially higher equity prices over time. Importantly, this outlook no longer relies on unusually aggressive growth rates; instead, expected annual returns are now consistent with long-term historical averages, helped by the possibility that productivity gains from technological innovation may offset demographic headwinds.

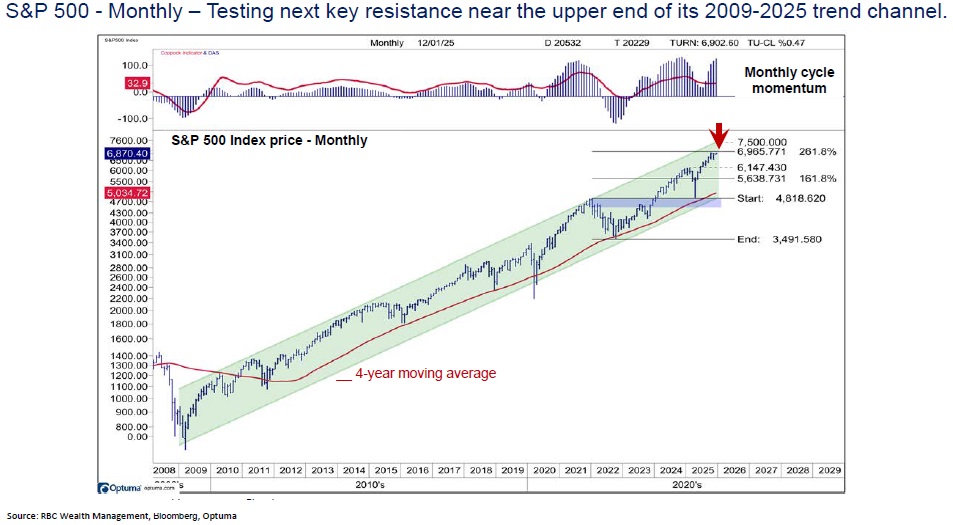

While the secular uptrend remains intact, the market is no longer early in its cycle. The current advance is approaching the upper end of the long-term trend channel that has defined the market since 2009. As a result, upside potential remains, but volatility and consolidation risks are increasing.

Position Within the 4-Year Cycle

Structural bull markets are composed of smaller multi-year cycles, typically lasting 2–4 years and driven largely by liquidity conditions, central bank policy, and corporate earnings momentum. Historically, these cycles have delivered strong gains during secular uptrends but have also experienced meaningful corrections along the way.

The current 4-year cycle is judged to have bottomed in Q4 2022 as inflation and interest rate pressures peaked. With the market now up nearly 100% from those lows and entering the later stages of the cycle, the probability of a pullback in 2026 is rising. This would be consistent with both cycle history and mid-term election year behavior. Even so, history suggests it is entirely possible for equities to post a fourth consecutive positive year, albeit with lower returns and larger intra-year drawdowns.

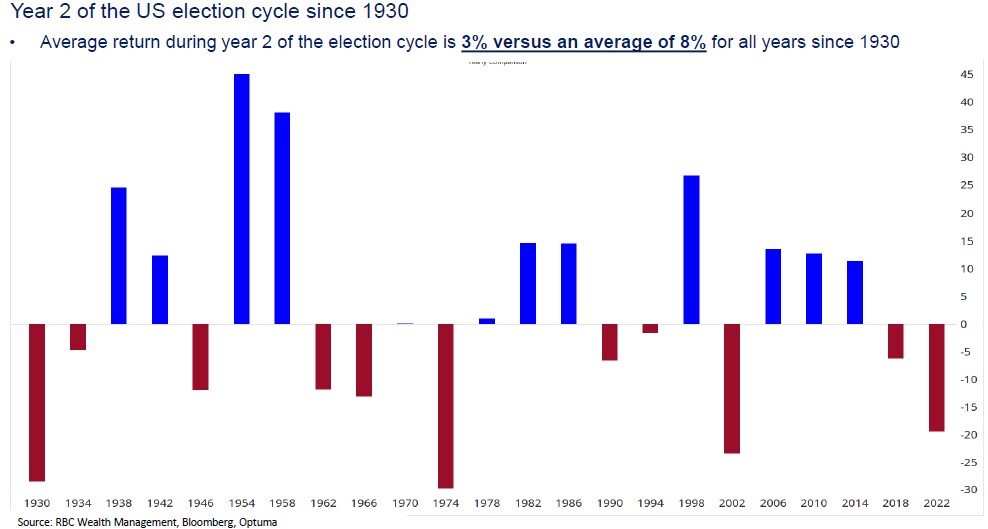

Year 2 of Presidential Cycle

From a historical perspective, year two of the presidential cycle has produced the lowest average returns (+3%) and the largest intra-year drawdowns (-20%). While the average return for year two is modest, the year has historically finished positive after experiencing a significant correction along the way. This pattern aligns with expectations for 2026: continued longer-term upside potential, but a higher probability of a 15–20% pullback, particularly in the first half of the year.

Bottom Line

The secular bull market remains intact, but it is maturing. Expectations for 2026 should center on more modest gains, higher volatility, and a greater likelihood of meaningful pullbacks. Broadening participation and sector rotation support near-term upside, but investors should avoid chasing extended leadership and instead focus on diversification, rebalancing, and risk management. Rising long-term interest rates remain the key variable that could disrupt the positive longer-term trend.