- One common concern we hear from investors is that the market has gone up too much or has advanced for too long and is destined for a fall.

- The trend in recent years is for both the ups and downs in markets to be exaggerated compared to what we had in the past, so concerns over corrections generate a higher state of anxiety.

- Unlike a carton of eggnog, history suggests that bull markets in stocks don’t have a “best before” date.

- To get something more meaningful than a run of the mill 5-10% correction the ingredients have typically included tight money from central banks, and often times, a U.S.-led recession.

- As it stands today, the Federal Reserve is cutting interest rates and economic growth forecasts are rising, suggesting the chance of the Fed “killing” the bull market are receding.

- Nonetheless, we construct portfolios with the mantra of “expect the unexpected” because anything can happen and often does when we least expect.

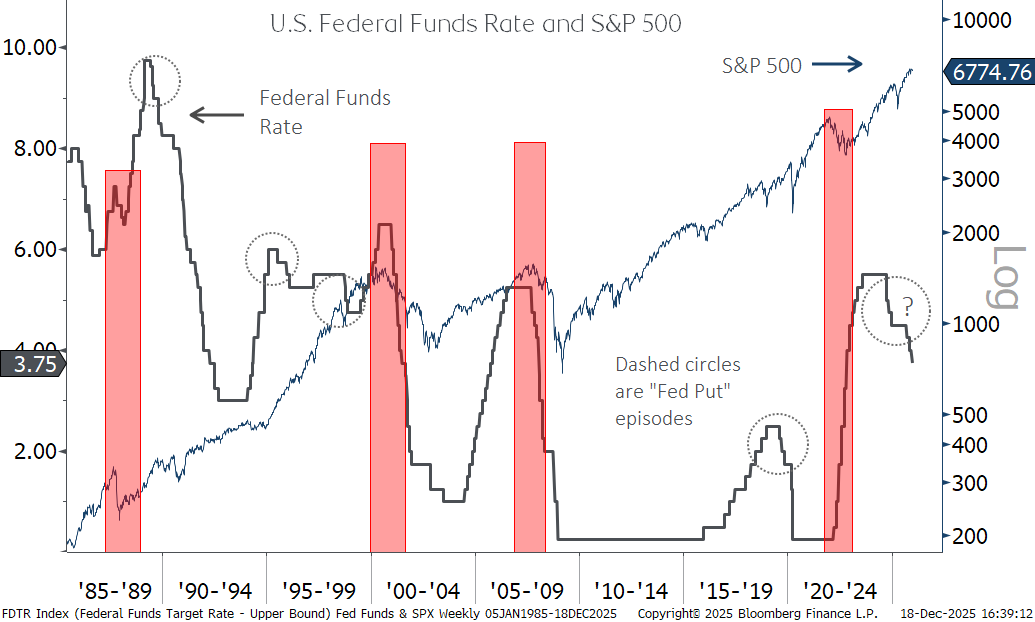

The adage "Bull markets don't die of old age; they are killed by the Federal Reserve" is one we have been thinking about a lot lately. It suggests that economic expansions and rising stock markets don’t simply "run out of steam" as time goes on. Instead, they usually conclude when the central bank—specifically the U.S. Federal Reserve—raises interest rates to a point that stifles growth or triggers a recession. This is not to suggest that all Federal Reserve rate hiking cycles end in tears. In fact, there have been many episodes where the so-called “Fed Put” comes into play. These are instances where the central bank recognizes that risks to the economy are imminent, and they cut interest rates in time to protect stocks from a more prolonged decline.

The Fed has its share of guilt for causing investors pain…

The chart above (Federal Funds Rate in grey and indexed on the left; S&P 500 in dark blue indexed on right) would argue the view that high interest rates are generally the precursor to sharp stock declines is generally true. The shaded areas indicate periods where a push higher in central bank interest rates heralded a meaningful decline in stocks, and if we look at all the major declines since the 1980s, they all began when interest rates were on their way higher or were paused at a high level. The one exception is of course the COVID-19 pandemic in 2020, an exogenous shock to the economy (and the world at large!) if there ever was one.

… but it also has a history of prolonging the cycle with timely policy shifts

Also evident in the chart are episodes where the Federal Reserve reversed course from a rate hiking trajectory, prolonging the upward trend in stocks. Prime examples of this are when stocks stood on the precipice of descending into bear market territory (a 20% drop from all-time highs), only to have the Federal Reserve adjust policy and renew investors’ faith in the market. The starkest examples are in 1998, when the Russian debt crisis precipitated an emergency rate cut, and as recently as 2018 when markets sold off sharply headed into the holidays, bottoming on Christmas Eve. The cause that time? Investor concerns that continued interest rate increases after years of near-zero interest rates were set to push the economy into recession, only to see the Fed adjust their stance after a near-20% drop in the S&P 500.

Expect the unexpected in 2026

It feels like we use the phrase above ever year, but it is with good reason. The world has a habit of throwing us curveballs, and over the last several years the impact on markets has been more magnified. The ups are getting bigger, but so are the drops. Little wonder why investors are nervous after three years in a row of healthy returns. We would note that a bull market that is 10 years old is not "due" to end any more than one that is 3 years old, provided the economic environment remains stable. In case we needed more proof, we mentioned last week that investors since 1988 who have bought at all-time highs have on average seen stronger returns than investors who bought on any other day.

As we round the calendar into 2026, we have economists upping their U.S. economic growth estimates and a lower rate trajectory from the Federal Reserve. Those alone don’t guarantee gains in 2026, but they also don’t suggest a market calamity. It wouldn’t surprise any of us to have a more normalized rate of return in 2026 and as always volatility lurks. This argues for continued prudent portfolio management and asset allocation, like any other year. We don’t see anything that suggests investors should substantially deviate from a robust financial plan. In fact, doing so at inopportune times is a sure-fire recipe for long-term disappointment.

The Harbour Group

416-842-2300

Putting you first, every time, to help you navigate the complexities of managing your wealth. All of our team members, all of our resources, all of our collective insight: ALL FOR ONE: YOU™.

The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. RBC Dominion Securities Inc. and its affiliates may have an investment banking or other relationship with some or all of the issuers mentioned herein and may trade in any of the securities mentioned herein either for their own account or the accounts of their customers. RBC Dominion Securities Inc. and its affiliates also may issue options on securities mentioned herein and may trade in options issued by others. Accordingly, RBC Dominion Securities Inc. or its affiliates may at any time have a long or short position in any such security or option thereon. Mutual funds are sold by RBC Dominion Securities Inc. There may be commissions, trailing commissions, management fees and expenses associated with mutual fund investments. Read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member CIPF. ®Registered Trademark of Royal Bank of Canada. Used under licence. RBC Dominion Securities is a registered trademark of Royal Bank of Canada. Used under licence. ©Copyright 2019. All rights reserved.