RBC Capital Markets recently hosted a call on the state of the Canadian Housing Market. In this note, we will summarize a few key thoughts from this presentation.

The pandemic created very strong demand for residential housing, with a bigger increase seen in rural versus urban homes.

In general, Canadian house prices are down 15 % from their peak of 2022, but we are still above pre–pandemic levels. Toronto prices are down 20 %, Vancouver 13 % and Montreal 11 %. Presently, we are not seeing “forced selling “ based on the low levels of listings and almost no mortgages payments in arrears in the banking system.

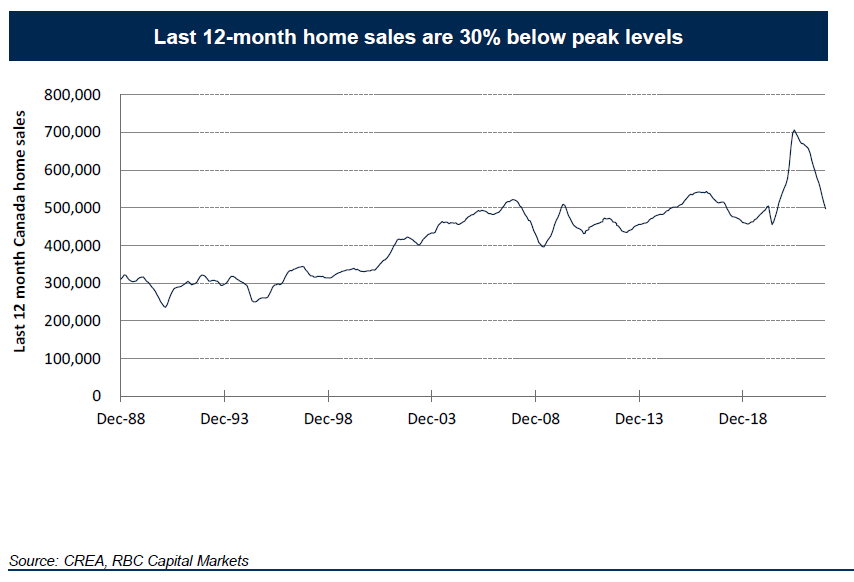

In the last 12 months in Canada, home sales have fallen by 30 % to a level similar to pre-pandemic.

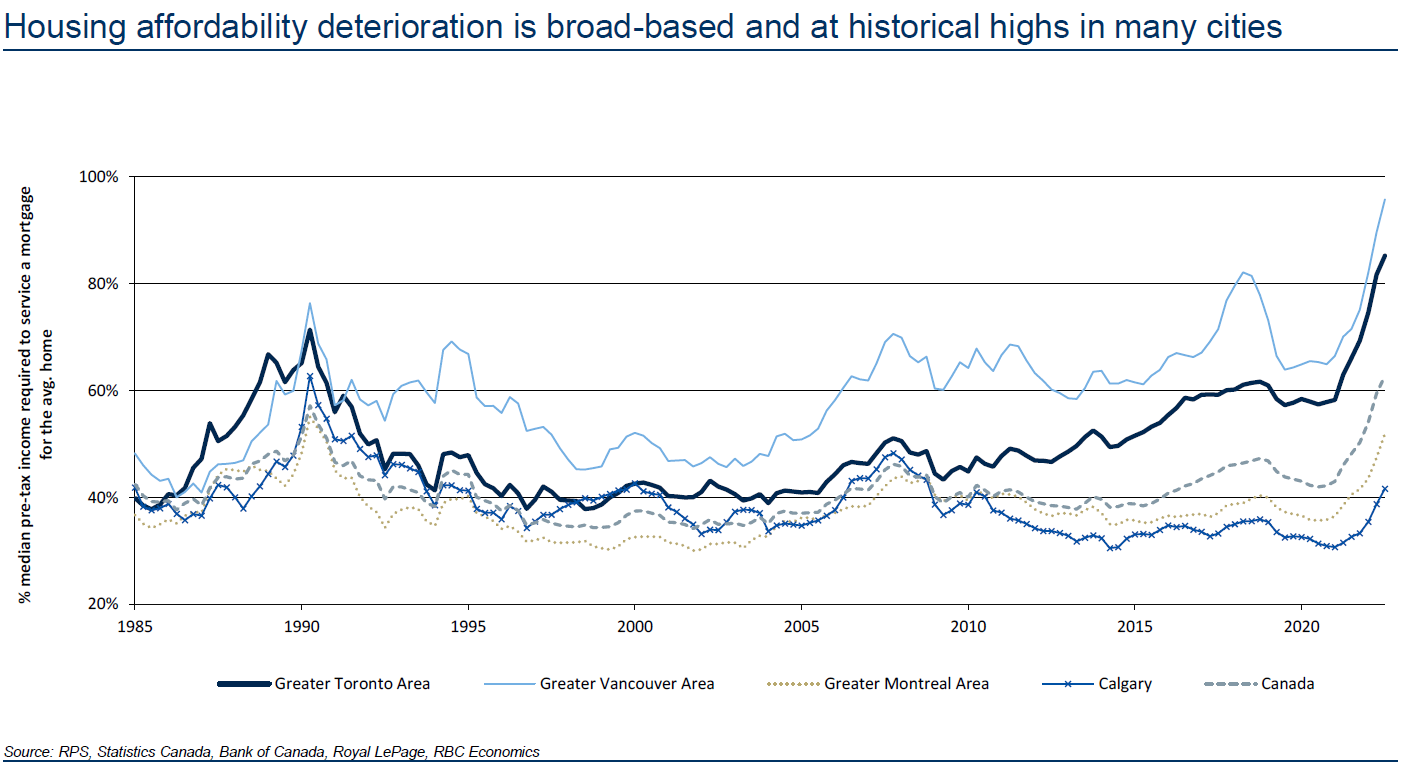

Housing affordability is still difficult. For the average home in Canada, you need 65 % of a median pre-tax income to service a mortgage. In Toronto and Vancouver, that number is closer to 80 %.

As rates rose in the first half of 2022, we saw a shift in demand from fixed rates to variable rates. Variable rates are tied to the Bank of Canada overnight rate. This rate went from 25 basis points (0.25%) to 425 basis points (4.25%) as the Bank of Canada fell behind the curve as the economy re-opened post pandemic, causing a sharp increase in demand with supply chain challenges.

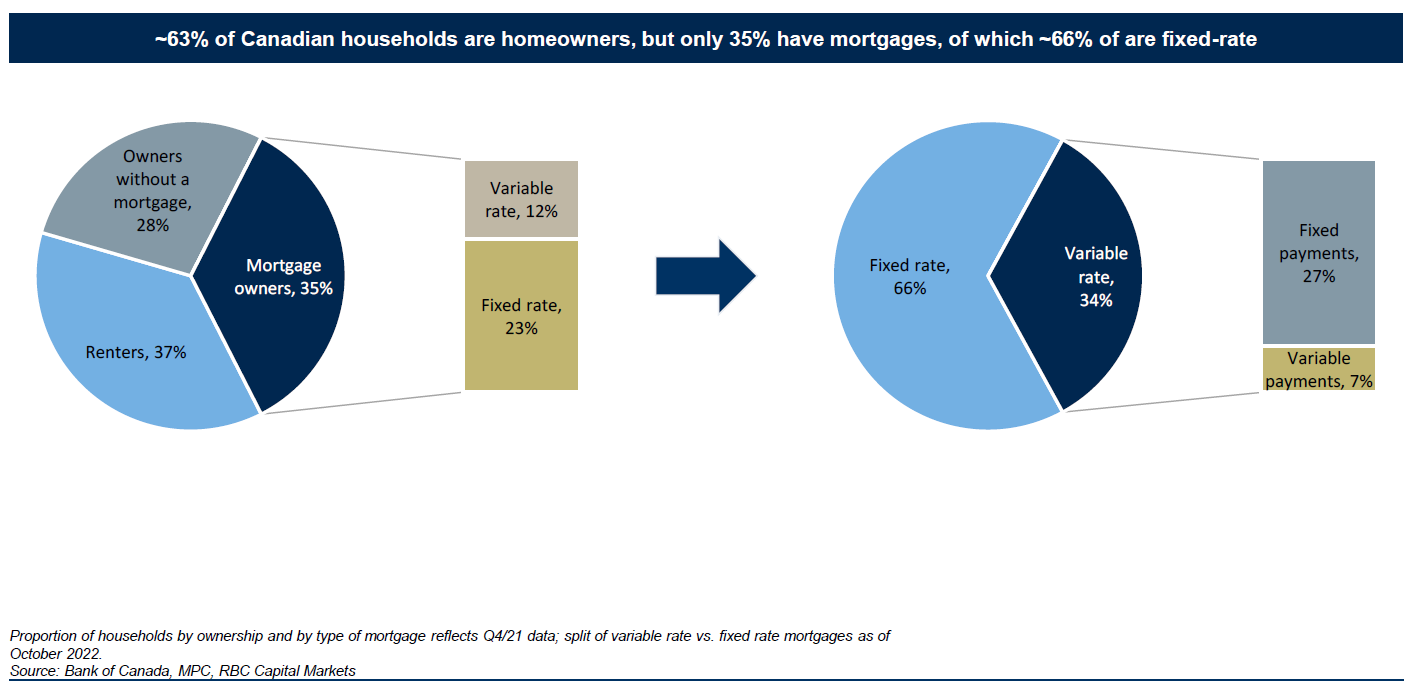

The Canadian mortgage market is 2.1 Trillion dollars and 75 % of theses mortgages are held by the big 6 Canadian Banks. 35 % of Canadians have a mortgage, 37 % are renters and 28 % own their homes debt free.

For this note, we will focus on the 35 % of Canadians that have a mortgage. Of those Canadians that have a mortgage, 66 % are on a fixed rate mortgage, typically this would be a 5 year fixed rate with an amortization term of 25 years. Of the remaining 33 % that are on a variable mortgage, 80 % of these people are on a fixed payment variable mortgage, which means that if variable rates go up, their payments do not change, only the split of capital payment vs interest payment changes up to a certain trigger point which might cause some adjustments on the terms with the bank. The other 20 % (7 % of Canadians) on a variable mortgages would be directly and immediately affected by increasing overnight rates.

With regards to fixed rates, if one assumes that you would need to renew your 5 year fixed rate mortgage today, your payment would go up by approximately 20 %. In this time period, in Toronto as an example, the average disposable income has come up by 27 %. So as you can see, disposable income growth was superior to the increased in financing costs. Also again in Toronto, the average home value went form 900,000$ to 1.3 million$ in that time period. If we assume that 5 years ago, you put down the minimum deposit of 5 %, your loan to value (LTV) would have gone from 95 % to 58% today.

Mortgage delinquency rates are low in Canada and stand at 0.15% of all mortgages. In the early 90’s, delinquency rates were closer to 0.60%. As a side note, Quebec’s delinquency has greatly improved from 1990 from 1% to 0.15% today. This is another sign that shows that the improvement in the economy in Quebec in that period was remarkable.

As another comparison, during the Great Financial Crisis of 2008/2009, delinquencies in the US rose to 500 Basis points.

A few positive factors today in Canada compared to the early 90’s is that the unemployment rate in the 90’s was around 13 % vs 5 % today. The mortgage rate was 14 % then vs 6.5 % today.

In early January, RBC held a Canadian Banks CEO conference. All CEOs were comfortable with their mortgage books. Not to say that arrears will increase, but the FICO* score, the loan to value metrics and the remaining cash deposit balances from the pandemic were still 30 % above pre pandemic level.

It would also be our view that the Canadian banks today have a lot more tools available to them to monitor their client’s financial health. Canadian Banks also have a different loan mix compared to the 90’s. In the 90’s, banks held a lot more commercial loans and commercial real estate loans vs residential mortgages. Banks were also less sophisticated in risk management back then. An example of a significant loan default in the early 90 ‘s is the Canadian Imperial Bank of Commerce that underwrote a loan to Olympia and York commercial real estate that was equivalent to 65 % of its equity value ! This would be totally impossible in today’s risk management world.

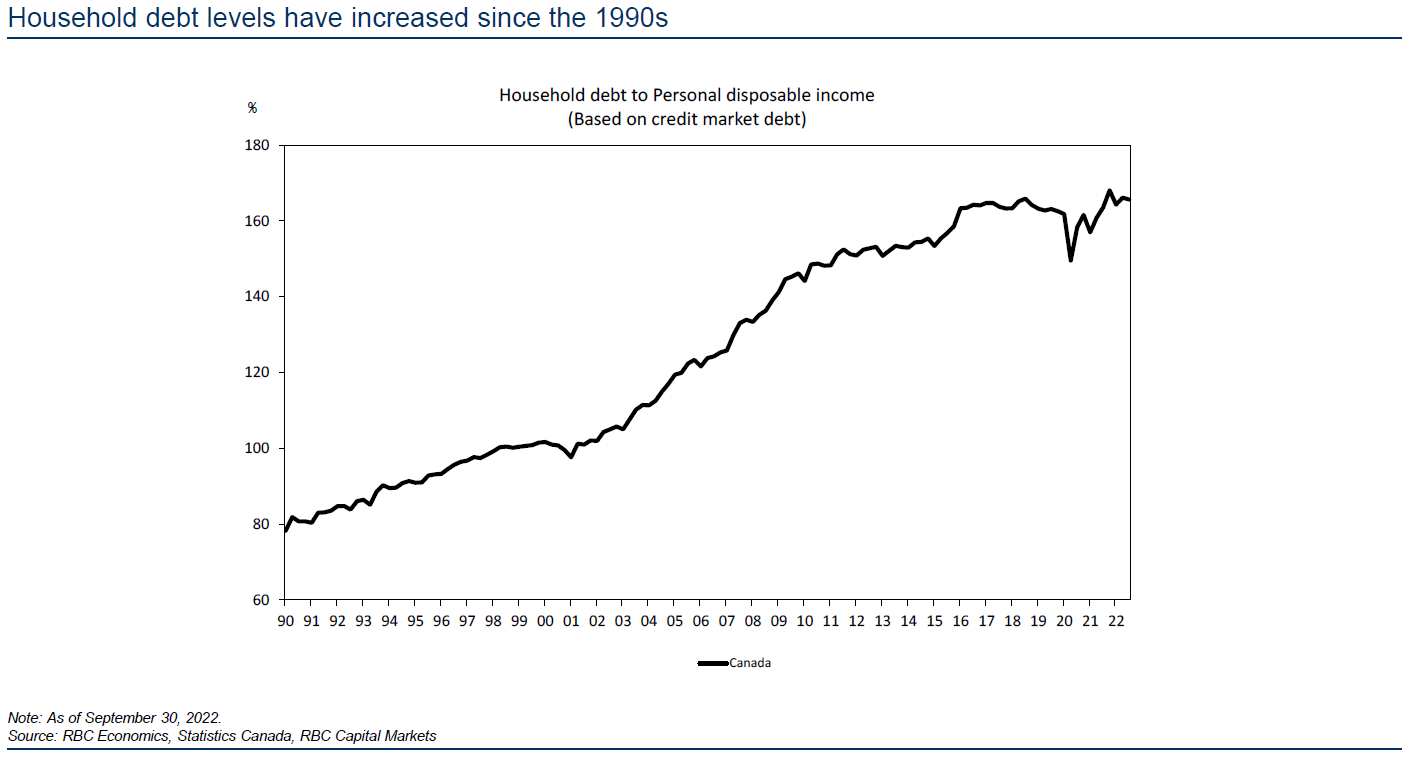

We are NOT saying there is no risk. One ratio that concerns us is the household debt to disposable income ratio. Today, this ratio in Canada is at a 30 year high at 160 %. We think that OSFI‘s (Office of the Superintendent of Financial Institutions) recent increase in the Domestic Stability Buffer** is in part related to this and the increase in the use of variable rate mortgages.

In conclusion, even though we remain cautious because of the high debt to disposable income ratio of household in Canada, we believe that the Canadian housing and mortgages market as well as the Canadian banks are in a good position because of low unemployment rates, still low interest rates compared to recent history, the high quality underwriting standards on mortgages and the banks improvement in risk management.

Regards,

Steve, Alex and Phil.

*FICO: A credit score used by lenders to evaluate a borrower’s credit rating.

** Domestic Stability buffer is a capital buffer that banks are required to set aside to be able to cover losses during uncertain financial times.