Quarterly commentary - Spring 2024

In our Q4 2023 commentary, we discussed the beginnings of a divergence between the US economy and most other economies worldwide. A disparity has continued to show itself in the expected monetary policy of the respective countries. Some measures of economic activity like business insolvencies and unemployment are continuing to trend in a direction pointing to a weakened economic backdrop in most countries except the U.S. This difference can be explained by the fact that the US economy is less sensitive to interest rate hikes and demonstrates a higher productivity rate. This has been confirmed in the recent higher-than-expected inflation data print.

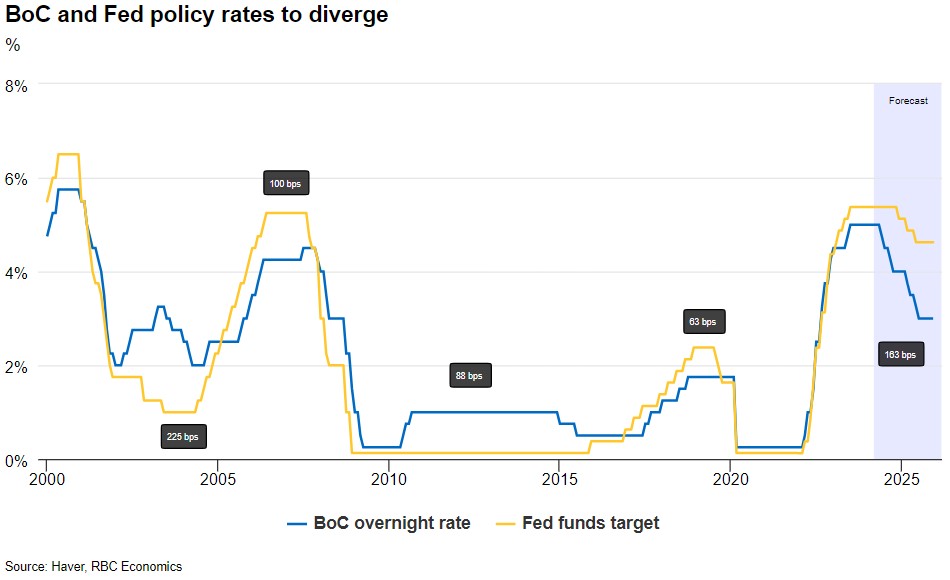

An increasingly pronounced gap in economic performance warrants a divergence in expected monetary policy by the Bank of Canada (BoC) and the US Federal Reserve, with the BoC now expected to begin cutting its key rate as early as June for a total of 4 rate cuts in 2024, and the Fed to delay its first and only rate cut until December of this year.

An increasingly pronounced gap in economic performance warrants a divergence in expected monetary policy by the Bank of Canada and the US Federal Reserve

Consequently, US bond rates are still the highest of the developed countries. For example, the US 10-yr rate exceeded 4.5%, while the Canadian 10-yr rate hovered around 3.7%, the UK’s at 4.1% and Germany’s even lower at 2.4%.

When the market struggled in 2022 and in much of 2023, it was often dogged by inflation fears (and the related significant Fed interest rate hikes and rising Treasury yields) and elevated recession risks. Importantly, earnings growth also declined during part of that period. For the past six months, those headwinds had largely receded.

However, the reality is that the risks that held back performance in 2022 and much of 2023 never really went away.

Performance at March 31st 2024

The results in CAD of the various indices for the quarter ended March 31st 2024: +6.6% for the Canadian S&P/TSX index, +13.0% for the US S&P 500 index and +7.3% for the Europe-Asia-Far East index.

Interest rates increased slightly again over the first 3 months of the year, leading to a marginally negative performance in fixed income. The benchmark FTSE TMX Canadian Bond Index posted a negative return of (-1.2%). The appreciation of the US dollar against the Canadian dollar had a positive impact of +2.2% on US strategies over the same period. Canadian dollar results for a balanced portfolio are around +5.0% for the last three months.

Balanced portfolio returns over the last twelve months are generally between +9.0% and +11.0% in CAD.

Outlook & market observations (from RBC Wealth Management’s Global Insight Weekly April 11th):

With the S&P 500 perched near the 5,000 level, we think it’s prudent to keep an eye on three nagging risks:

- Inflation could remain sticky or rise,

- GDP growth could decelerate

- The ongoing geopolitical and military clashes in the Middle East and Eastern Europe could widen

Inflation: The fight’s not finished

RBC Capital Markets points out that the higher-than-consensus March Consumer Price Index (CPI) headline and core data are not the only yellow lights flashing on the inflation front.

Inflation pressures in March were broad. More than half of the items measured within the consumer inflation basket rose. Also, goods prices picked up following an eight-month stretch of month-over-month declines.

The March CPI report, combined with other deteriorating inflation trends earlier this year, prompted RBC Capital Markets to decrease its forecast for Fed interest rate cuts from three 25 basis point (bps) cuts to just one this year, and it thinks it would come in December, after the U.S. presidential election the month before.

RBC Capital Markets still forecasts only two rate cuts next year (one in January, the other in March). In this scenario, the Fed would stop cutting its target interest rate at 4.75 percent—a much higher level than the four previous major rate cut cycles since 1990.

We don’t think the equity market is particularly sensitive to the exact number of rate cuts that the Fed might implement for the remainder of 2024. But should the Fed end up cutting rates by just 75 bps throughout its rate cut cycle as RBC Capital Markets is now forecasting, we think the market would need to adjust because it’s probably currently factoring in more than just three cuts.

GDP: Marginal growth does not have a marginal impact

The Bloomberg consensus forecast for 2024 GDP growth has risen notably, from 0.6 percent in mid-2023 to 2.2 percent currently, and RBC Capital Markets anticipates it can exceed this pace. The well above-trend GDP results from the second half of last year and sturdy underlying employment metrics along with improving manufacturing data so far this year support the notion that 2024 GDP growth could exceed 2.0 percent, in our view.

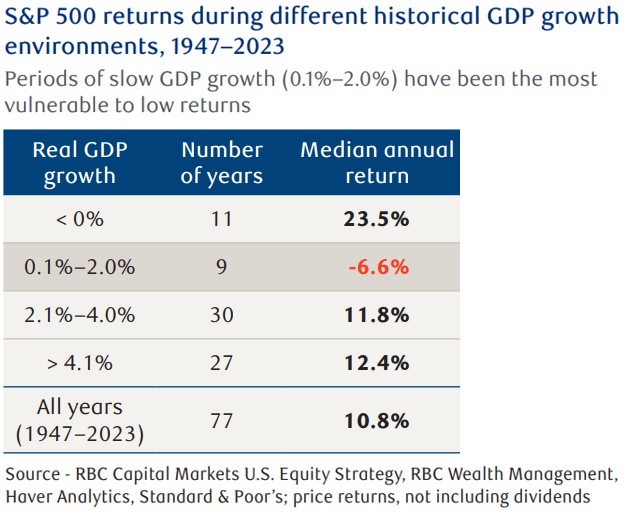

Annual GDP growth above 2.0 percent corresponds to historical periods of good gains for the S&P 500. The index rose 11.8 percent on a median annual basis when annual GDP growth was between 2.1 percent to 4.0 percent, according to a study by RBC Capital Markets U.S. Equity Strategy.

However, note that when GDP was within a more sluggish 0.1 percent to 2.0 percent zone, equity market performance often stumbled, with the S&P 500 falling 6.6 percent on a median annual basis. Among the four categories of GDP growth that RBC Capital Markets segmented, S&P 500 performance for this category was by far the weakest, as the table at right shows.

If GDP growth decelerates meaningfully later this year—a possibility that can’t be ruled out according to our leading economic indicators—we think the equity market could run into some bumpy patches.

Geopolitical: Crude connection

Another risk for the market is that the military conflicts in the Middle East and Eastern Europe, and the geopolitical tensions associated with them, could widen.

Equity markets have historically absorbed military clashes and related escalations rather quickly. In the 19 previous key events that occurred since World War II, the S&P 500 fell an average of 6.3 percent, but then traded back up to even in just 29 trading days, on average. However, the market and economy tended to struggle more and for longer when oil prices rose for a sustained period.

Striking a balance

When it comes to equity positioning in portfolios, we recommend balancing out the risks associated with inflation staying sticky or reaccelerating and GDP growth decelerating into a sluggish phase, with the possibility that the U.S. economy could sidestep such risks and remain resilient.

We will also closely monitor changes in interest rates, particularly the 10-year government bond rate. At the time of writing, inflation’s persistent showing above the 2% target has caused the American benchmark bond to rise above 4.50%. Remember, this same rate started the year 2024 at 3.90% (more accommodating for equity markets) and it is now approaching 5%, reached in November 2023 (in restrictive territory for equity markets).

We maintain a neutral equity weighting relative to the target as defined by your investment policy statement. Especially after a market rally that lasted 5 full months (between November 2023 and March 2024). It is very likely that we will go through a period of consolidation in the coming months.

Spring reading

We invite you to read the following two in-depth articles which appeared in our monthly publication Global Insight during the month of March. These articles specifically address the upcoming US elections, and serves as a reminder that 2024 is also a very busy election year globally.

Article 1 – Key things to know about U.S. elections

Do not hesitate to contact us if you have any questions about your situation.

We wish you an excellent start to the spring season and look forward to speaking with you soon!

Mathieu & Anthony

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that action is taken on the latest available information. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / TM Trademark(s) of Royal Bank of Canada. Used under licence. © 2024 RBC Dominion Securities Inc. All rights reserved.