Transplants.

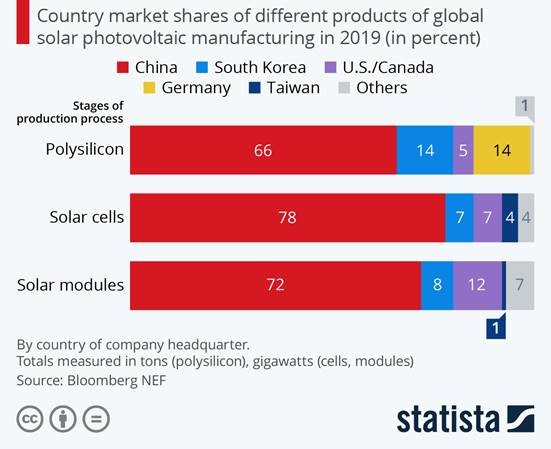

As the chart below shows, today China dominates global inputs for solar panel production. What the chart doesn’t show that their industry takeover, less than a decade in the making, was built in a region dominated by what several countries, Canada included, has referred to as an ongoing genocide. A Sheffield Hallam University study (In Broad Daylight) last year found that nearly half of China’s solar panel inputs originate from what the PRC calls: “…the organized transfer and employment of rural surplus labour.” Think Orwell here. Work camps. Uyghurs

The Sheffield study concludes that China’s rapid takeover of the world’s solar market: “… comes at great cost to the workers… In the Uyghur Region, companies create green energy by consuming cheap, carbon-emitting coal… to improve climate conditions (they) sacrifice humane labour conditions in the bargain.”

We’re not talking about accusations of shortened lunch breaks here. Plucked from home, families are separated, party officials supplant parents, beliefs are outlawed, women sterilized, raped, and unthinkably, there’s credible evidence of organ harvesting. Chinese solar power might just be the new blood diamond.

Gut-check: Lately there’s been much mucky mucking about socially-responsible investing. If that’s a reflection of YIMBY (yes-in-my-back-yard) that’s fantastic. But as for financial analysists and CEO’s as arbiters of ethics, can we agree that they aren’t exactly in their wheelhouse there? As for Hollywood, politicians, and young radicals “speaking truth to power.” Um… Coal-powered slave labour is bad, right?

Hello? ESG? Anyone? Is this thing working?

Crickets.

Other News:

Still preferred? Credit market and interest rate risks are in focus this week as the Fed surprised with its plans to sell its corporate bond holdings. But amid those risks we look to a seemingly unlikely place—the preferred share market—and ask whether it can still provide portfolio income, as well as defense, in this environment.

Regional developments: Canadian real GDP rose 5.6% (annualized) in Q1; U.S. stocks struggle, while meme stocks and commodities gain attention; ECB likely to continue to nurture the nascent recovery; India’s market at a peak despite COVID-19.

More here: Global Insight Weekly

Have a great weekend!

Mark