Whether you already own your business, are thinking of starting a business from scratch or are buying an existing business, choosing the right business structure can have a major impact on the future success of your enterprise as well as your personal tax and estate planning.

Your decision should take into account a range of factors including the nature of your business and where it’s located, the number of people involved, taxation considerations, your potential exposure to liability and the company’s financial requirements.

Consult an experienced legal professional and tax accountant. Your professional advisors can help ensure that you are well informed about the legal and taxation issues you may encounter and that you understand the personal and business implications of your decisions.

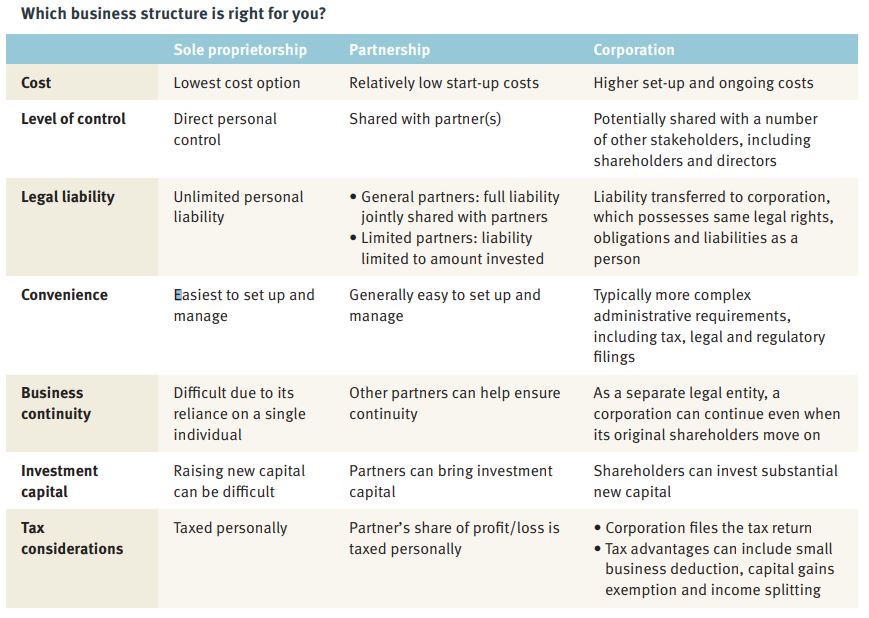

A sole proprietorship is the simplest form of business organization and is often the most inexpensive to set up.

Sole proprietorships

A sole proprietorship is the simplest form of business organization and is often the most inexpensive to set up. This can be a good option for small enterprises or when you are just starting your business because you, as the business owner, have direct control over business decisions and receive all the profits. However, with this kind of structure, you are legally responsible for the debts and obligations of the business. This means that both your business and A sole proprietorship is the simplest form of business organization and is often the most inexpensive to set up. personal assets may be subject to the claims of creditors. This is called “unlimited liability”.

How is a sole proprietor taxed?

You must file a personal tax return to report your business income. You should include the income, or losses, from your business on your personal tax return as part of your overall income for the year. Your net business income is taxed as personal income, so there are limited tax planning opportunities; however, you may be able to deduct your business losses from your other income sources.

Partnerships

Partnerships can be relatively easy to set up and often have low startup costs. A key advantage of having partners is that they generally bring additional sources of investment capital and provide a broader management base. However, finding suitable partners can be a challenge. In addition, this kind of business structure can mean a division of authority, so there is potential for conflict between the partners.

A written partnership agreement, though not required, can help minimize potential conflict. In many cases it sets out the terms of business, protects the interests of individual partners in the event of disagreement or dissolution of the business and generally defines how the partners will share the business profits.

Your personal liability for the business and the actions of your partners can differ depending on the type of partnership. Be prepared for the possibility that your partners’ decisions will be legally binding on you, and ensure you discuss all aspects of this decision with your legal advisor.

If you are considering investing in a partnership, you should review the tax and legal implications carefully with your professional advisor.

How is a partnership taxed?

A partnership is not a taxable entity. This means that instead of the partnership paying tax, the partnership’s income or loss flows to the individual partners, who report their proportionate share of income or loss on their personal tax returns.

Corporations

Corporations are a very popular business structure. A corporation is a separate legal entity from its shareholders and has the legal characteristics of an individual. It can own property, incur legal liability, lend, borrow and carry on a business.

If you’re thinking of starting or investing in a corporation, there can be a number of advantages. It can provide greater business continuity as shares can be bought and sold without affecting the company’s continued operation. It is also easier to raise investment capital for a corporation, and you may find that the size and resources of an incorporated business make it easier to attract specialized management expertise. In addition, as an owner-manager and a shareholder, your liability is generally limited to your shareholding, so your personal assets are protected from the company’s creditors unless you have provided personal guarantees for loans to the corporation.

It’s important to obtain legal advice when setting up or acquiring an incorporated business. Corporations are more closely regulated than sole proprietorships or partnerships and may be more costly to set up. You will be required to hold annual shareholder meetings, meet certain record-keeping obligations and comply with requirements under the legislation governing the corporation. This can mean more administrative, legal and accounting expenditures.

How is a corporation taxed?

Since a corporation is a separate legal entity, a corporation files its own corporate tax return and pays taxes on the income it earns. A corporation’s income is calculated separately from the business owner’s or shareholder’s personal income.

| Business planning quick tip Inexpensive and simple to set up, sole proprietorships are generally more suitable for smaller enterprises with a single owner/manager who wants direct personal control. Costs are usually higher for partnerships and corporations, but it’s easier to raise investment capital, making them a better choice for larger enterprises. They also offer tax and legal advantages that may appeal to certain enterprises regardless of size. The good thing is that you can change your business structure as your business develops and circumstances change. |

Tax planning for corporations

As an owner-manager, you may be able to benefit from some of the tax planning opportunities available to incorporated businesses:

- The small business deduction provides potential tax-deferral opportunities and a reduced corporate tax on active business income up to the small business limit that is retained in the corporation. Be aware that there are a number of rules that reduce the corporation’s ability to claim the small business deduction.

- If your business qualifies as a qualified small business corporation (QSBC), all or a portion of any gain realized on the sale of the shares can potentially be sheltered from personal taxation using the capital gains exemption.

- By incorporating, you may have the opportunity to split income and reduce taxes by paying dividends to adult family shareholders in certain circumstances.

- Adding other family members as common shareholders directly or through a family trust (referred to as an “estate freeze”) can allow you to transfer future tax liability on the growth of the company to lower income family members and multiply the use of the capital gains exemption on the sale of QSBC shares.

Talk to your professional advisors about the structure that’s right for your business or whether your current structure is providing what you need to achieve your goals.