Housing trends and affordability - COVID-19 edition

Highlights:

- Pandemic has soured the outlook almost overnight: Social distancing and the economic shock will cut home sale activity to a trickle near term. The timing and speed of the eventual rebound is uncertain.

- We expect property values to fall briefly: Surging unemployment and the market’s illiquidity will compel a growing number of tight-squeezed sellers to make price concessions.

- Oil-producing regions are the most at risk: The oil price plunge will compound the damage to housing demand at a time when Prairie markets still struggle with excess inventories.

- Policy response will soften the impact: Interest rate cuts, government financial support and banks’ offer to defer mortgage payments will help many households navigate through the storm.

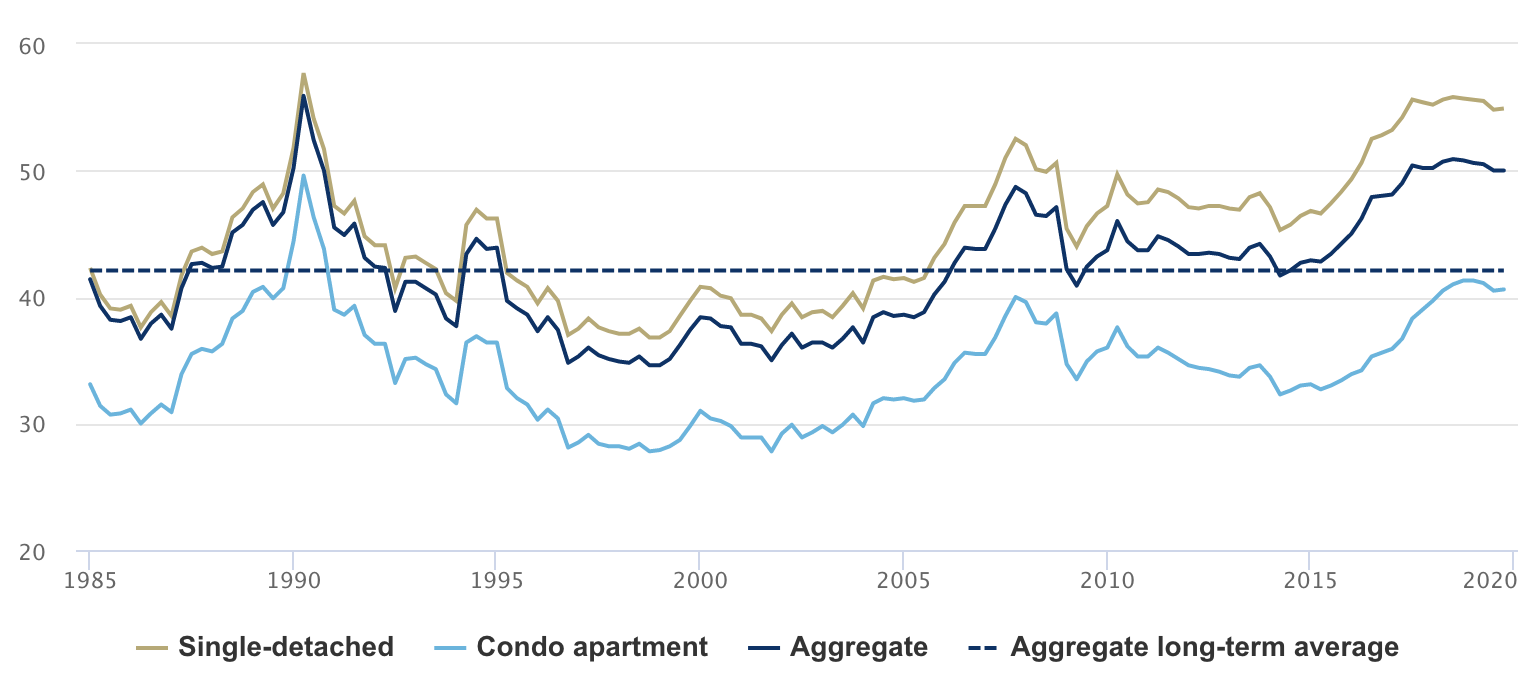

- Housing affordability will take a back seat: Though it’s still a big issue in Vancouver and Toronto, the pandemic and economic turmoil will draw more attention near term. RBC’s aggregate affordability measure for Canada was unchanged at 50.0% in the fourth quarter of 2019, after improving slightly in the three previous quarters.

The share of income a household would need to cover ownership costs (in %)

RBC housing affordability measures - Canada

Ownership costs as % of median household income

Social distancing to severely disrupt spring house hunting season

Canada’s housing market will slow to a crawl this spring as Canadians follow social distancing orders in order to combat the spread of COVID-19. We expect realtors to suspend open houses and cut any private showings to a bare minimum. Signs were starting to point toward a significant pullback even before governments stepped up restrictions on social gatherings and despite the adrenaline shot from the Bank of Canada’s back-to-back interest rate cuts this month. Equity markets’ freefall, mounting job losses, reduced work hours, the shutdown of Canada’s borders (stemming the flow of in-migrants) will hammer confidence and cool demand. Investors and speculators also are likely to sit things out for a while. There will be plenty of reasons for sellers to wait and see as well. A shock like this one is an inauspicious time to get full value for a property. We expect for-sale inventories to shrink, which will further contribute to stall activity.

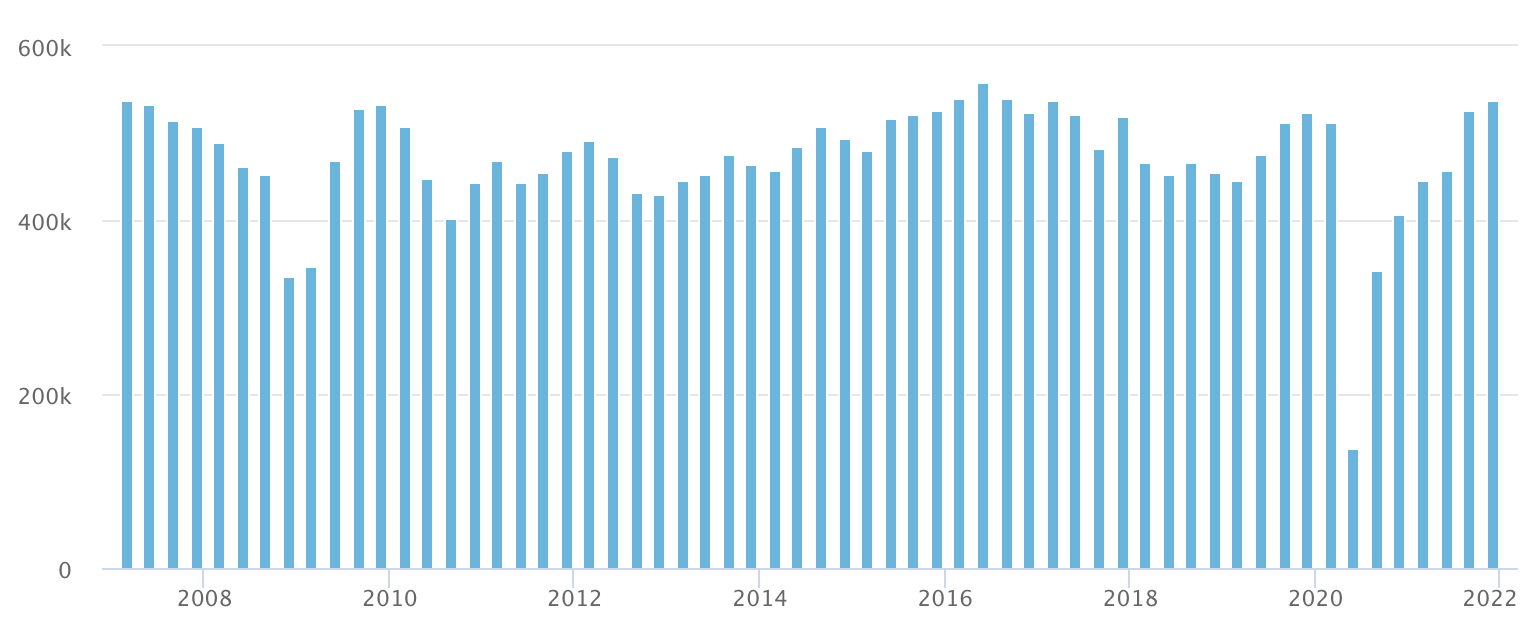

COVID-19 to knock the wind out of the housing market this spring

Home resales in thousands of units, seasonally adjusted and annualized, Canada

Source: Canadian Real Estate Association, RBC Economics, *Forecast - from March 2020 onwards

The pandemic will be a temporary shock

Housing activity will resume once the health crisis comes under control and authorities lift containment measures. The timing and speed of the recovery is uncertain at this point. We’re currently penciling in early-summer as the restart date. We think the recovery will come in stages—taking buyers up to a year to regroup and rebuild confidence amid high unemployment. Based on these assumptions, we project home resales to dive by nearly 30% this year in Canada to a 20-year low of 350,000 units. We see the outlook improving markedly next year in most markets. Exceptionally low interest rates, strengthening job markets and bounce-back in in-migration will generate substantial tailwind. We project home resales to surge more than 40% to 491,000 units in 2021.

Property values will fall briefly

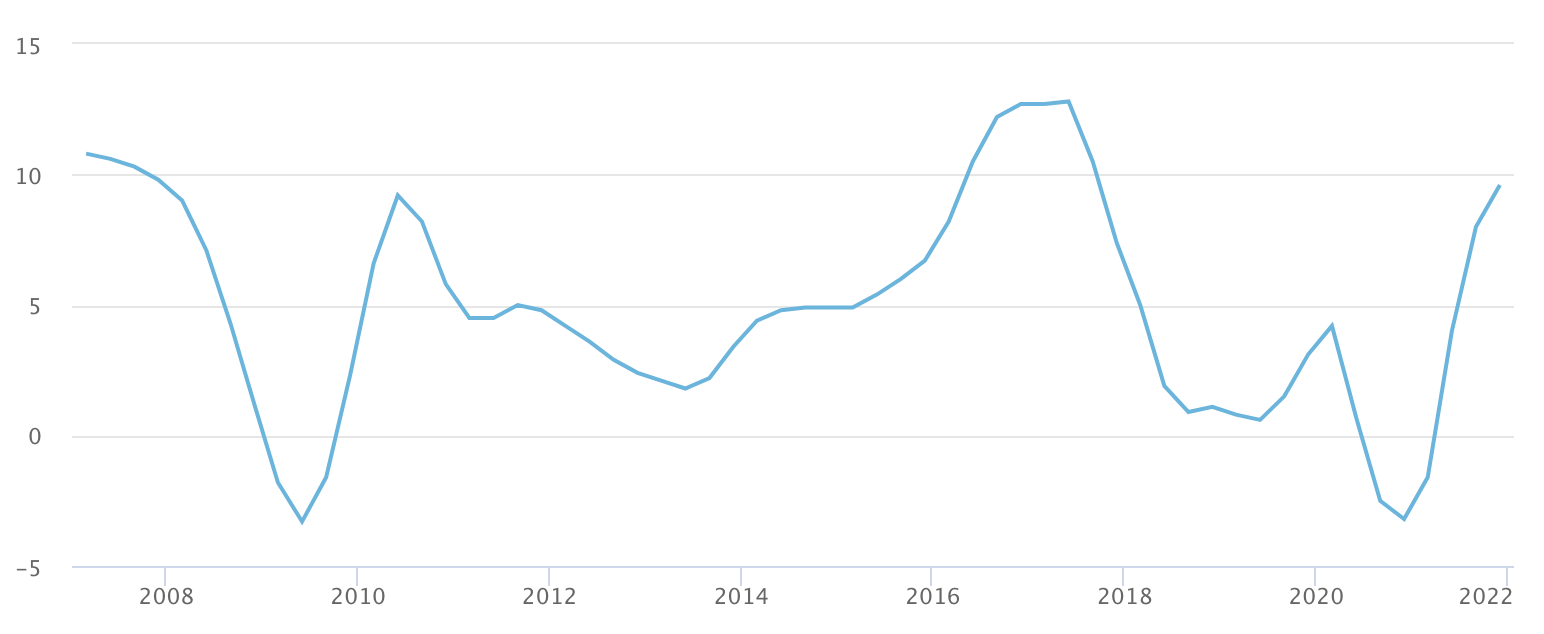

Property values have received strong support from tight demand-supply conditions in the majority of markets since mid-2019. We expect some degree of support to hold initially as both buyers and sellers go into hiatus. Lower interest rates, governments’ financial help to vulnerable Canadians and banks offer to defer mortgage payments will provide some downside protection. This won’t last. In a matter of weeks or months, surging unemployment and the market’s illiquidity will compel a growing number of tight-squeezed sellers to make price concessions. We project Canada’s composite benchmark prices to fall briefly over the second half of 2020 by an average of 2.9% year over year. The surge in activity we expect in 2021 will tilt the scale back in favour of sellers and swing the price dynamics around.

Rising unemployment illiquid market conditions to briefly ding prices

Annual % change in the composite price benchmark, Canada

Source: RPS, RBC Economics, *Forecast - from March 2020 onwards

Oil price plunge puts Prairie markets at greater risk

The outlook is bleaker for markets in oil-producing regions where the plunge in oil prices will deepen and prolong economic hardship. Price declines are bound to re-accelerate significantly in Prairie markets. High inventories have been an issue for some time and the situation is likely to get worse. We see little prospects for prices to rebound anytime soon.

Housing affordability picture was stable overall in the fourth quarter of 2019

The string of quarterly affordability improvement in Canada ended at three. RBC’s national aggregate affordability measure stalled in the final quarter of 2019 at 50.0%. This was down slightly from 50.8% a year earlier. More significant improvements were recorded in Vancouver, Victoria, Calgary and Saint John over that period—though the changes in Vancouver and Victoria didn’t alter their status as Canada’s least and third-least affordable markets. RBC’s measure rose the most in Toronto and Ottawa relative to the third quarter, reflecting accelerating prices. In Montreal, buyers benefit from a strong income gain which more than offset a solid price advance.

Robert Hogue is a member of the Macroeconomic and Regional Analysis Group, with RBC Economics. He is responsible for providing analysis and forecasts for the Canadian housing market and for the provincial economies. His publications include Housing Trends and Affordability, Provincial Outlook and provincial budget commentaries.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.