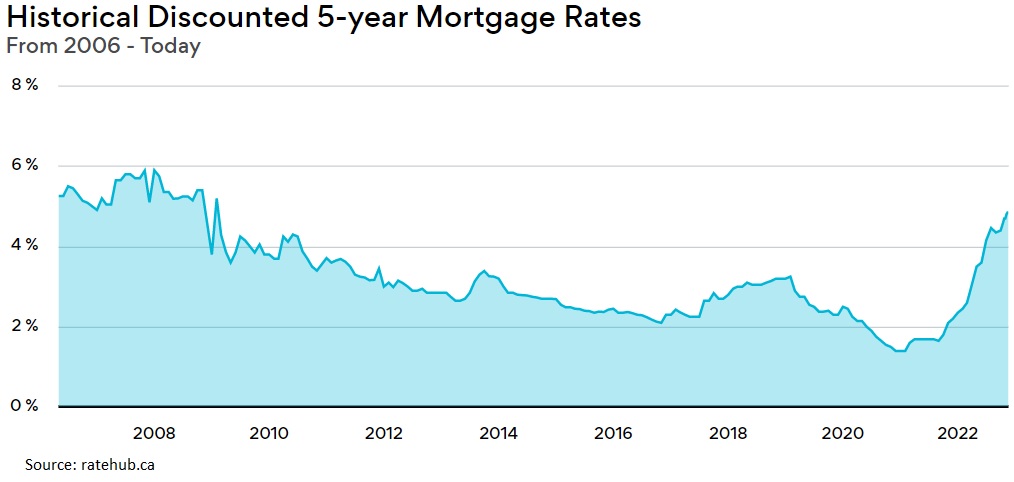

With the financial conditions tightening meaningfully this year, it should not come as a surprise that an interest-sensitive sector like housing has experienced a fairly significant decline. The Bank of Canada started raising its benchmark rate in March from 0.25% to the current rate of 3.75%. There is also an expectation of another 0.25-0.5% increase in the next month. As a result, mortgage rates, on average, have risen from a low of 2% earlier this year to now well over 5%. The chart below illustrates the sharp incline in 5 year fixed mortgages.

With a combination of higher mortgage rates, economic uncertainties, and tightening financial conditions, Canada’s housing transactions have contracted after hitting record prices in the early spring.

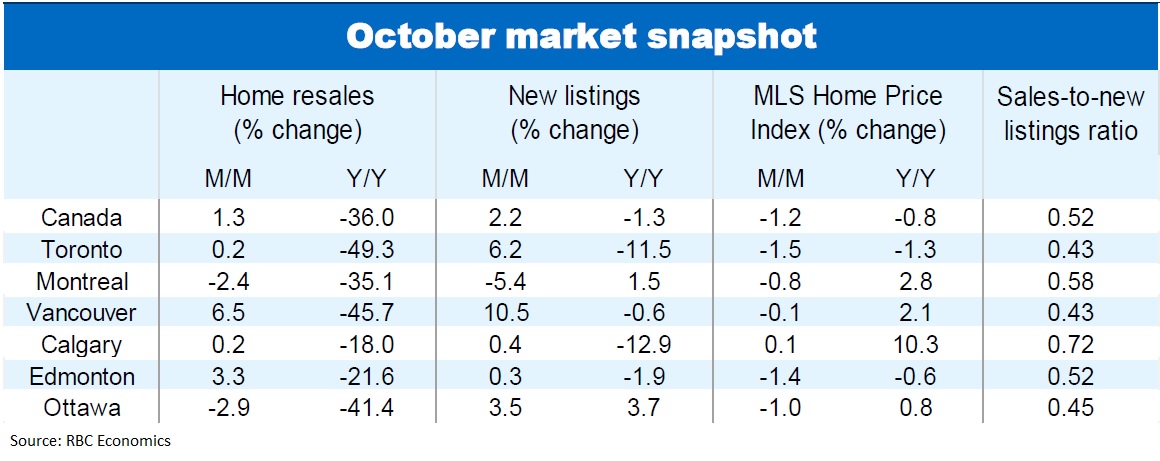

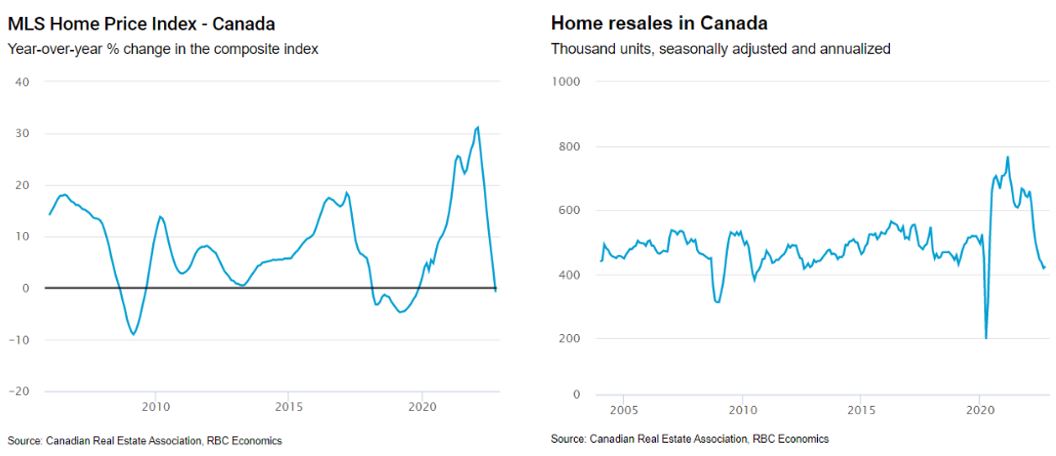

With the most recently published October data, the downward trend in home prices has yet to find a trough. As depicted in the charts below, the aggregate MLS Home Price Index for Canada slipped for an eighth straight month in October (down 1.2% from September). It slipped below its year-ago level (-0.8%) for the first time in three years, and it is now down 11% since the February peak. That being said, if affordability conditions continue to degrade, there is reason to believe that further downward pressure on property values will materialize.

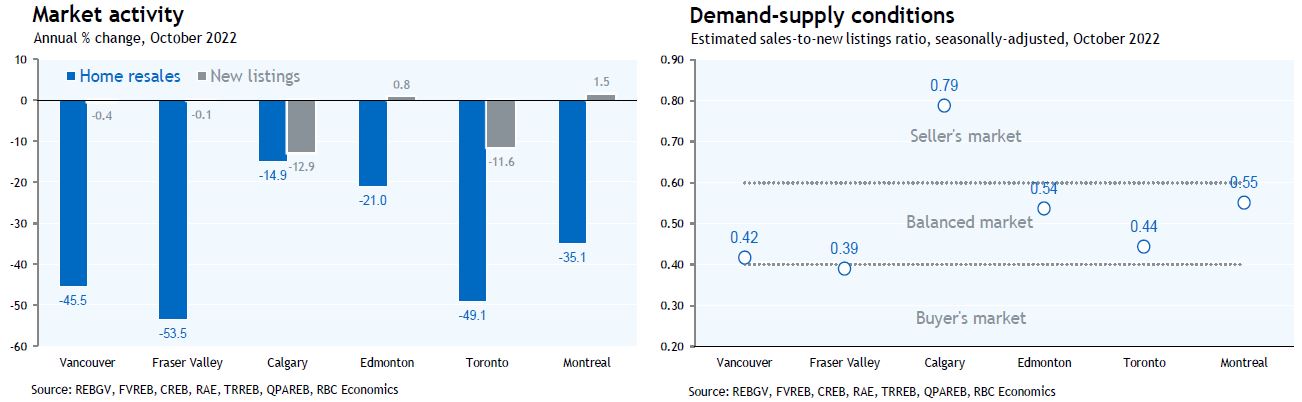

The market related to home resale has also been dire, with key geographic markets like Toronto and Vancouver experiencing a 50% decline in activity. The amount of new listings has also been mostly flat to negative on a year-over-year basis. One of the few bright spots arising from this sudden decline in activity is that supply and demand dynamics are becoming better balanced. The ratio of ‘sales-to-new-listings’ is one measure of supply & demand, with a ratio above 0.6 signaling a “seller’s market” and a ratio below 0.4 signaling a “buyer’s market.” Anything between 0.4-0.6 is considered balanced, and currently, many of the major cities are sitting in that balanced range.

Our view is that the housing market will stay generally soft over the coming months. The massive interest rate increases to date and further expected rate hikes from the Bank of Canada by year-end will continue to significantly challenge buyers. Asset classes like stocks can quickly benefit from the central bank ending their rate hiking plans. After all, liquid equity markets are forward-looking, and a pivot in monetary policy provides clarity to corporate earnings immediately. However, for real estate, even if the central bank pauses their interest rate increases, the incremental buyer is still priced out of purchasing a home as interest rates remain elevated. It is foreseeable that real estate needs rate cuts to fuel demand and improve affordability before prices can recover meaningfully. Hence, the recovery in real estate may be slower than some may expect. For those readers based in Toronto, the MLS Home Price Index declined for the seventh straight time in October and is now off 18% (or $237,000) since the March peak, reversing almost half the $504,000 increase earlier in the pandemic. The single-family detached segment (down 3.7% y/y) accounted for most of the depreciation. Condo prices are holding up better, with their index remaining 7.5% above where it was a year ago. RBC expects these diverging trends to persist in the near term.

RBC Economics’ forecast calls for the national benchmark price to drop 14% from peak to trough. With rising interest rates and the loss of affordability, market activity should remain quiet into 2023, with the chance of bottoming prices around spring. With the prospect of higher interest rates, and a housing market that has yet to bottom and potentially slow to recover, we recommend clients review how one’s real estate portfolio may impact their overall financial plan.