Commodities seem to have finally gotten their mojo back like the ‘good ol days’ of the early-2000’s. Investing in commodities and related companies has been frustrating for well over a decade. The last mini bull cycle for commodities lasted a few years after the Financial crisis, driven by infrastructure spending from China. Oil prices topped $100 per barrel and have since spiraled downwards. Capitulation was seen on April 20, 2020, where a perfect storm of Covid and a price war between the Saudis and Russians led oil futures to a historic low of -$37/barrel (yes, negative!).

The Covid pandemic brought along an immediate collapse in economic growth and demand for many commodities like oil, base metals, and lumber. This drop was short-lived as commodity markets quickly reflected supply chain disruptions (forced operating closures, transportation disruptions, and reduced capital investment). In other words, prices were initially driven lower by the drop in demand but then turned higher to reflect the drop in supply.

The rebound in prices was exacerbated when the demand side regained its footing from the discovery of effective vaccines, a raging housing market, and expectations for a large Biden infrastructure bill. In the past 12 months, prices are near historic highs with a 90% increase in both oil and copper and a 300% increase in lumber. Below is the chart for lumber, which we track out of pure amazement!

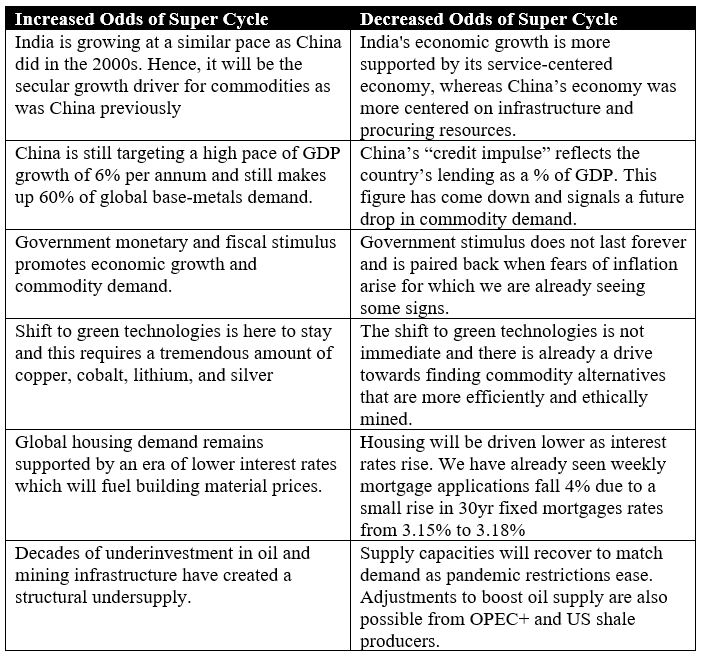

With all that said, is this just an example of a “bull run” or is it the start of a longer-term commodity supercycle? By definition, a supercycle refers to a decade-long period where the prices trade above the historical trend. These events are not common and in the past required a significant demand shock to occur. This was the case in the 2000s with the surge in economic growth from Brazil, Russia, India, and China (BRIC). Together they represented 2.6 billion people, which represented approximately 40% of the world’s population. These four countries required a momentous amount of materials, food, and energy commodities to support their rapid growth and industrialization. Below we table both sides of the debate as to whether we are entering a super cycle.

In the shorter term view, commodity-related companies will likely show increased earnings growth and improved cash flows that will help reduce the debt on their balance sheets. Shareholders will in return be rewarded with dividend increases and buybacks. Volatility, however, should be expected.

This generation of investors has become numb to the idea that extreme outlier events like a “supercycle” cannot occur. They have simply experienced too many supposed “once in a lifetime” milestones. Phrases like “fastest drop since xxxx”, “largest drop since xxxx”, “worst health crisis since xxxx”, have all become regular headlines. We even have our own lived example of a “tulip-mania” through cryptocurrencies. Regardless of whether this is a ‘super cycle’ or just a momentary ‘bull run’, we believe resources and commodity exposure should be a part of all balanced portfolios. What was previously a group of ignored sectors, are now screaming at you to pay attention.