The Federal Reserve raised interest rates by 25 basis points (bps) in March as it seeks to balance inflation risk and financial stability risk. The liquidity issues that arose amongst US regional banks have caused a tightening in lending conditions that could dampen economic growth and inflation. As a result, the need for further monetary policy tightening has been reduced as the Fed has signaled that they may be near the end of the tightening cycle.

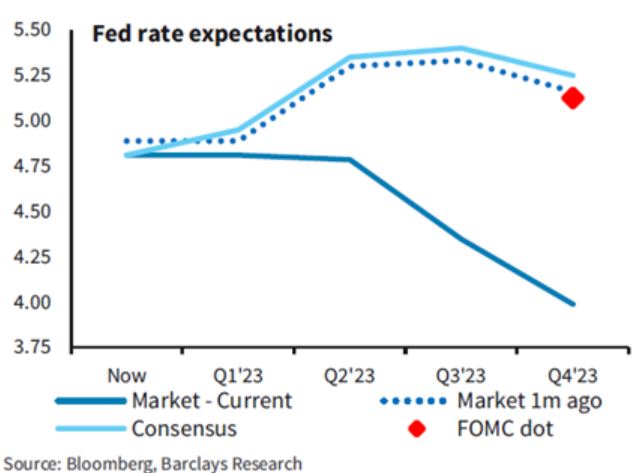

How quickly things have changed. Just a month ago, both the market and the Fed were in “agreement” that the year-end Fed rate would end up between 5% to 5.25%. This can be seen in the chart below, where the Fed expectations (red dot), the market forecast (dotted line), and the consensus estimates (pale blue line) all converge. However, with the recent US regional banking instability, current market estimates have now significantly undershot to the downside towards 4% (dark blue line). This implies that the Fed could potentially deliver ≈100 bps (1%) of rate cuts through the end of the year and that it may start as early as Q2. One could argue that the lowered interest expectations reflect the progress made in the February economic data, as we received reports of declining inflation (CPI & PCE), producer prices (PPI), retail sales, and wage growth. Although these are positive trends for a Fed that wants to see a cooling in prices and economic activity, the timing and steep drop in interest rate expectations best coincide with the regional banking instability.

The initial reaction of investors may be that this is a fortuitous and positive development. Investors may be enticed to go on the offensive in their asset mix positioning as a less hawkish fed and potential rate cuts would alleviate the uncertainty on corporate earnings and the economy. After all, if rates increases held the markets back, then rate cuts should release the market higher. That being said, history tells investors to remain patient as the S&P500 rarely finds its cycle trough before the Fed’s first rate cut.

Within the timeframe between the last rate hike to the first rate cut, the S&P500 (SPX) returns have been mixed but still produce a positive median return of 4.1% (see chart below). The pattern of equity performance after the first rate cut also suggests some caution, with a -2.9% median return 6 months after the first rate cut. This may be explained in part by rising recessionary worries that typically emerge and were likely the basis for the rate cut in the first place. The outlook improves 12 months after the rate cut with a median return of +9.8%. Hence, should a recession be avoided or only become mild in nature, longer-term investors should expect positive returns during this transition toward loosening monetary policy.

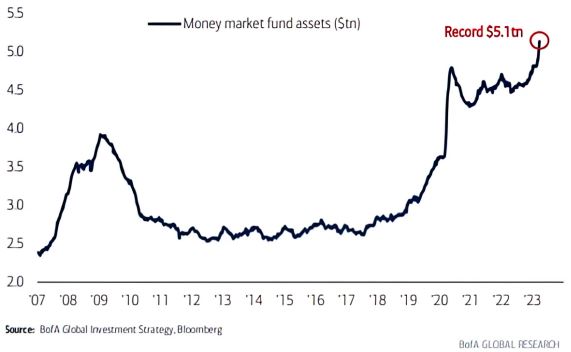

From a sector perspective, Defensives (such as Health Care, Staples, and Utilities) have typically performed well relative to Cyclicals (such as Financials, Materials, and Industrials) during the period between the last Fed rate hike and the first rate cut. Although we respect the data above and would refrain from 'aggressively' positioning into stocks, we also do not feel the need to be overly fearful. Current market positioning has already tilted bearish and pessimistic, as evidenced by the record levels deposited into money market fund assets (see chart below). As of March 22, 2023, institutional and retail investors held a combined $5.1 Trillion in money markets, which dwarfs the levels seen during COVID and the Great Financial Crisis. This is not to say that all market and financial uncertainty has already been priced in; however, it is important to appreciate that investors are already positioned for the downside.

For the time being, investors who already have equity exposure should remain patient and await a stabilization in the banking sector to see where yields and interest rate expectations settle. Keeping a nimble and balanced portfolio is recommended as we approach earning seasons and receive further economic data. Speak to your advisor to discuss when and how the percentage of one’s equities could be added or subtracted to fit this dynamic market environment.