The Most Rewarding Investment

By Emmanuel Athanassakos, CIM, CFP, Investment & Wealth Advisor, RBC DS

What if I told you that the most rewarding investment has no monetary value at all?

Let me start with two key principles.

First: Money can, and often does, facilitate happiness. You will notice I didn’t say money brings about happiness. Why? Because you can have all the money in the world and still be miserable. But if there are activities or experiences that make you happy, chances are they cost money. Some cost a lot of money, some cost a little money, and yes, some cost no money at all. But many of the things that bring the average person joy can be traced back to a price. Even if not directly, then indirectly. For example, a father’s greatest joy may be to watch his son play the violin. The act of watching may not cost money, but every moment leading up to that recital, from the facilities to the teacher to the equipment, would have cost money. You give me life’s greatest pleasures, and I can probably trace it back to a financial commitment of some sort.

Second: One of, if not the greatest goal is to lead a happy and fulfilling life. Sometimes, our actions are not consistent with this, and we may even set some goals along the way that have conflicting aims, but we tend to look at all major life decisions within the context of long-term happiness and fulfillment.

So, if we agree that money can facilitate happiness, and we agree that happiness is the ultimate goal, then the next question becomes obvious: how do we best allocate our money to accomplish said happiness?

This is where the Harvard Study on human happiness comes into play. In 1938, Harvard researchers embarked on a study that observed people from all over the world. It started with 724 participants; boys from troubled families in Boston as well as Harvard undergraduates; but eventually branched out to include the spouses of the participants as well as more than 1,300 descendants of the initial group. The study took place over 85 years, and asked the participants detailed questions about their lives at 2-year intervals. It is the longest study on human life ever done. The goal of the study was to answer the following question: What factors lead to a fulfilling and happy life? The Good Life, a book by Robert Waldinger and Marc Shulz, will walk you through the observations, but allow me to skip to the end and give you the answer: Positive relationships. The stronger our relationships, the more likely we are to live happy, satisfying, and healthier lives.

Seems obvious, right? However, we don’t always put our relationships first. In 2018, the average American spent 11 hours every day on solitary activities such as watching television and listening to radio. With the enhancement of handheld technologies, I bet that number has only grown over the past 5 years. I mean, two of the largest companies in the world, Apple and Meta, are in a race to develop the best mixed-reality headset. And these companies have a combined $210 billion in cash on hand as of Q3 2024! So, you know this headset is going to do a pretty good job encouraging further solitude for those who will be able to afford one. Ultimately, we need to be more intentional about how much time and effort we put into our relationships. Why? Well, you will notice that the answer to the study wasn’t just relationships, but POSITIVE relationships. To maintain a positive relationship, the relationship must be nurtured over a long period of time. So, I want to talk about one very effective method of nurturing a relationship: money. Yes, I said it. Money. It isn’t the only way to nurture a relationship, but it sure is effective. When you buy a loved one a generous birthday gift, or you pick up the bill on a double date with your favorite couple, you are investing in those relationships in a very meaningful way.

Ultimately, you should ensure your primary needs are looked after first. Do the planning and budgeting to ensure you are allocating enough money to things such as food, shelter, retirement savings, etc. Heck, Toronto is one of the most expensive cities in the world; owning a home is a pipedream for most young couples, rent is sky high, and we just came off a 12-month period a couple years ago where inflation averaged 8%. But, when you are staring excess earnings in the eye, and you are trying to decide the best way to allocate those dollars to create the maximum amount of happiness, I want you to consider investing in a relationship that is important to you. I want you to look at buying a friend dinner the same way you would look at buying yourself a new pair of shoes. Because if there was one thing that this study hammered home for me, it was that relationships were a greater determinant of happiness than material goods.

Unfortunately, there are many people who don’t have the means to take care of themselves AND invest in relationships in a financial capacity. This doesn’t mean low-income individuals will have bad relationships. In fact, I know many low-income individuals who have better relationships than some of the wealthiest people I know. I am simply stating that if you have the finances to support it, money can be a very powerful tool for facilitating positive relationships, which in turn, have been proven to lead to a happy and fulfilling life.

Send your mom some flowers for no reason. Book a vacation with two of your closest friends. Heck, buy their plane tickets if you can afford it. Get out there and invest in your relationships, because the quality of our relationships has proven to be the number one source of happiness once we get to the end.

What am I Enjoying Right Now?

In search of nostalgia, I decided to re-watch this legendary series. A flashback to a crazier time, this show has some of the best character development and writing of all time. A true period-piece drama.

Just Keep Buying is a data-driven guide to personal finance. I love his opinion on what he calls the biggest lie in personal finance: He believes "the biggest lie in personal finance is that you can cut your spending to build wealth. Cutting spending is a short-term solution. The data is evident: the most reliable path to building wealth is to grow your income."

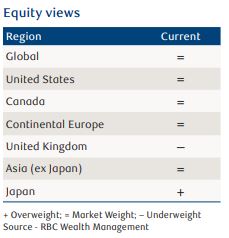

Your Global Equity Update

The equity market advance from the depressed lows of 2022 has now been running for 24 months. The only pullback of note was the three month, 10% correction in the spring of 2023. Since that point, there has only been one instance with a monthly close lower for the S&P 500. The same, more or less, can be said for every stock market in the developed economies.

Alas, there is no monthly “count” that tells us when the next correction is “due.” The gap between one painful occurrence and the next has varied widely between a couple of months and several years. This current advance could have further to run, in our view. However, two measures— sentiment and valuation—are providing much less support than they were two years ago.

At the market lows in October 2022 several measures of investor sentiment were extremely downbeat. Over the intervening 24 months investor attitudes have gradually bubbled higher: bullishness is now consistently posting well above-average readings and bearishness well below. While we think sentiment can’t yet be rated as “frothy” or “irrationally exuberant,” “complacency” is very much in evidence.

Valuation tells a similar story. At the October 2022 low the S&P 500 was trading at a very reasonable 16x that year’s earnings—fractionally above its long-term average. Today it’s at a rich 23.2x this year’s consensus earnings estimate of $247 (up 11.2% y/y) and 20.5x next year’s projected $280 (up 13.3% y/y). “Priced for perfection” probably overstates the case, but “priced for a continuation of above-average earnings growth” looks like the correct assessment to us.

Price-to-earnings (P/E) ratios moving up from depressed levels is a welcome signal to us that the outlook for the economy and corporate profit growth is moving back to normal. But as we see it, P/Es moving up from already extended heights smacks of investors coming to believe that higher-than-average earnings growth is here to stay—rarely a sustainable expectation.

That said, recent annual revisions of past data have revealed that corporate revenues and profits for the past year, as well as consumer incomes and savings, were higher than first reported. Those revisions for the overall U.S. economy won’t change the earnings already reported for the S&P 500 but are likely to make analysts more comfortable with their estimates for this year and next. (The revisions have not pushed any of our Recession Scorecard indicators back into more favorable readings.) It is unclear to us whether this better-than-reported economic data will make the U.S. Federal Reserve any less inclined to cut rates at upcoming policy meetings.

Our focus is on the U.S. consumer (approximately 70% of GDP). Not only have households’ assessments of current conditions sagged sharply from the beginning of the year, but a growing percentage of respondents in the Conference Board’s monthly Consumer Confidence Survey for September are reporting that “jobs are hard to get,” a statistic that correlates well with the unemployment rate. Some consumer behavior is reflecting these concerns.

The Mortgage Bankers Association reports that mortgage applications in the U.S. have risen sharply since the spring. However, those applications relating to the purchase of a home have been comparatively subdued, while the number of applicants looking to refinance an existing mortgage has surged dramatically (up 20% in the most recent week) and accounts for most of the action. Since rates have not fallen enough to suddenly make refinancing for financial advantage very enticing, we look for another rationale.

It would make sense to use lower-cost mortgage debt to pay down high-cost consumer debt: credit card rates are now at 23%, up from 9% two years ago, while car loan rates are at 9%, up from 4%. But so far, we see little evidence this is happening. Credit card balances and auto loans continue to rise as do loan delinquencies.

So, mortgage refinancing looks to be headed toward supporting existing spending levels rather than paying down debt, a worrying trend but not yet a dire one.

We expect U.S. GDP growth to slow through 2025—perhaps by enough to induce a recession, perhaps not. Central bank rate cutting almost everywhere is welcome, especially from the Fed, but monetary policy acts with a lag so these preliminary rate cuts are unlikely to show up in improved economic activity before midsummer of next year. Nor should one count on rate cutting by itself to head off a recession: the Fed had already begun cutting the funds rate before the start of eight of the last 10 recessions.

Corrections can arrive seemingly “out of the blue.” It would be tempting to predict one will arrive soon, given today’s rich P/E multiples together with the prevalence of investor optimism or, at least, complacency. However, we will resist that temptation, acknowledging that the odds of being wrong are high either way.

That said, we will again point out that one very reliable precursor of an impending bear market (as opposed to a correction) is so far nowhere in sight—namely, a trend breakdown in market breadth. Both the S&P 500 advance-decline line and the “equal-weighted” version of the S&P 500 have been racing ahead making a succession of new highs, with the more closely followed S&P 500 capitalisation-weighted index quickly following suit.

Things proceed differently when a bear market is in the offing. The advance-decline line turns lower as the majority of stocks fall into downtrends, even as an ever-smaller number of heavily weighted, high performing stocks push the index on to a final cycle high. No such divergence is apparent today.

As long as market breadth remains “in gear” with the broad averages, we are inclined to give stocks the benefit of the doubt.

However, were a new market up-leg to emerge, wherein breadth measures failed to participate and moved into a downtrend, a deeper, broader retrenchment for equity markets might be in the works. All the more reason why we believe a cautious, watchful approach is called for.