So, you think you’re having a bad month? While many have lamented the election of Donald Trump to a second presidential term, we bring you Porter Hanks (no relation to Tom, or at least none that we are aware of). Mr. Hanks, who only lived to 27 (more on that in a moment), led a fairly noble, albeit somewhat less celebrated life. At the age of 20, he joined the army and by the age of 27, he had gained the rank of lieutenant and was placed in command of Fort Mackinac on Mackinac Island. For those not familiar with Mackinac, it is an island off the tip of Michigan that lies in the Strait of Mackinac between Lake Michigan and Lake Huron. It also happened to be the westernmost military post for the United States in the year 1812.

In case you missed history class that day, the United States decided in 1812 that it was not happy with Great Britain for reasons we will not get into and so in late June of that year, the U.S. declared war on Britain and its allies; the problem was – nobody bothered to tell Lieutenant Hanks and his men (had no one heard of a phone?). We imagine that Lt. Hanks and his men were enjoying a fine early July morning when Captain Charles Roberts (no relation to the Dread Pirate, or at least none that we are aware of) he of the British forces in Canada marched up (or floated, considering it was an island) to Fort Mackinac with 40 of his own men and roughly 600 recently recruited Canadian voyageurs and First Nations warriors and demanded Hanks’ surrender. Hanks with only ~60 of his own men and also completely unaware that there was a war going on, obliged without incident.

Hanks and his men were afforded the “honors of war” and allowed to leave the Fort peacefully; although, according to the rules of the day, they were not allowed to fight until they had crossed back into friendly territory. Eventually, they reached Detroit, where Lt. Hanks faced court martial for surrendering his command, even though he was unaware that he was fighting a war. Anyway, in August of 1812, while Lt. Hanks stood trial, the British attacked Detroit with a volley of cannon fire. One such fusillade hit the very courtroom where Lt. Hanks faced prosecution and while it apparently spared everyone save two (the poor bloke standing beside Hanks), it decapitated Lieutenant Hanks, thus ending a very, very bad month.

While there have been few bad months in 2024 – at least from an investor’s perspective – we will use the above as a segue into our 2025 outlook. We will break this down into four “big” calls for 2025.

Interest Rates – The BoC Rate/Prime Rate will reach 2.25%/4.45% by YE 2025

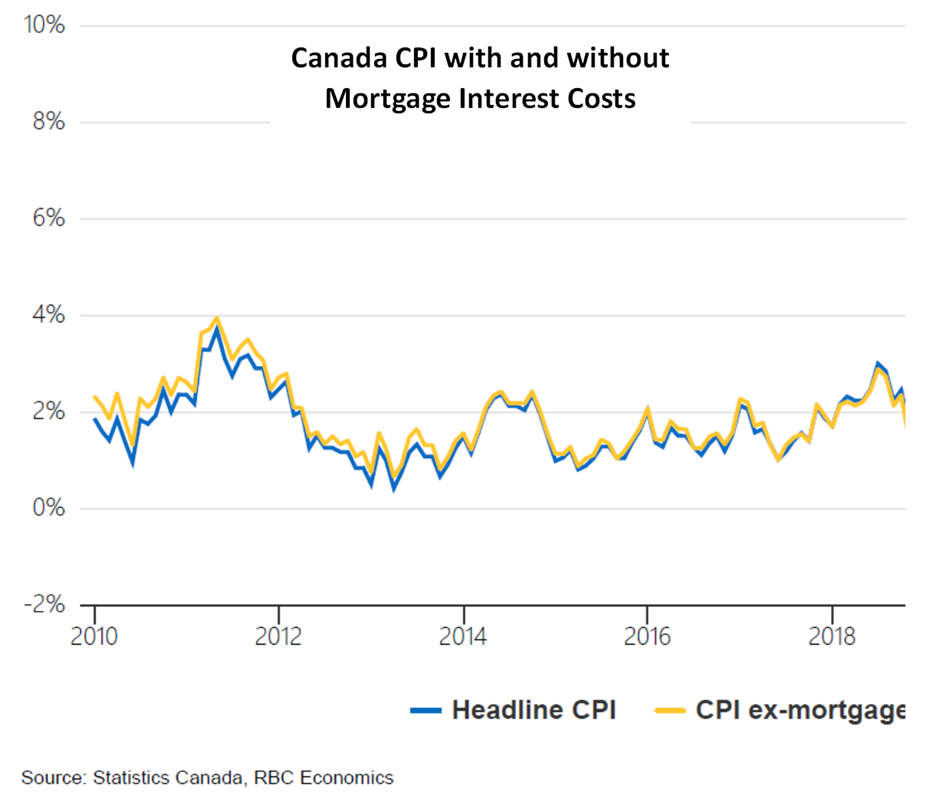

The Bank of Canada rate currently sits at 3.75% following 125 basis points worth of cuts. Add to that the 50-basis point cut we are likely to see this week and the BoC rate should reach 3.25% by year-end 2024, implying a prime rate of 5.45%. Let’s look at a chart and then comment:

The inflation rate is now down to ~2%, which when coupled with an economy that continues to stumble gives the Bank of Canada cover to continue reducing rates into 2025. As RBC Economics notes, a cut to 3.25% would bring the overnight rate to the high end of the BoC’s targeted range of 2.25% to 3.25%, implying that the Bank is simply “easing off the brakes”. Given the overall poor growth backdrop and the encouraging inflation data, we would expect the Bank to actually “step on the gas” in 2025, bringing the overnight rate to the bottom end of its targeted range by the end of 2025.

Housing – Bubble Risks Rising

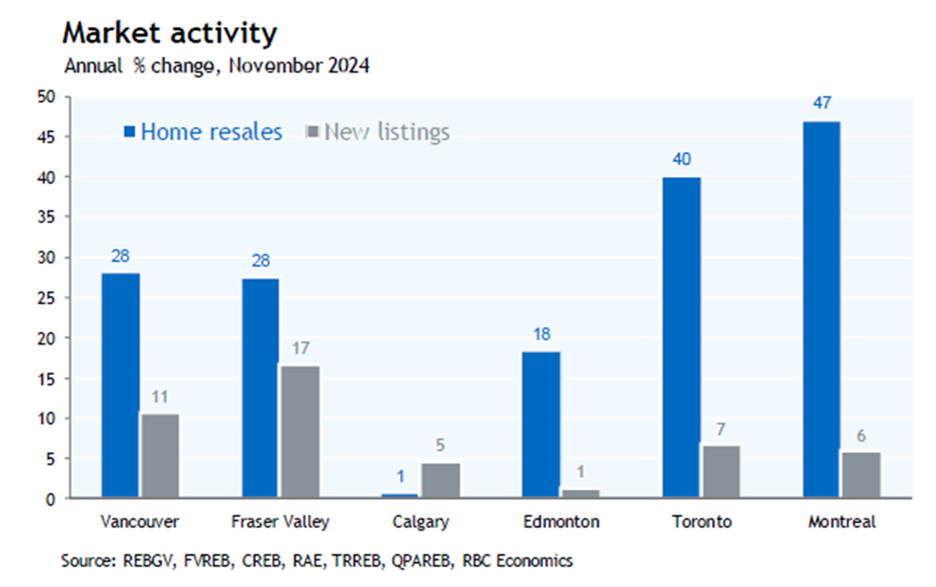

We wrote back in 2023 about the risks of another bubble in Canadian housing. This was based on a general lack of supply in single-family detached units and growing pent-up demand from increased immigration and high mortgage rates, which sidelined many would-be buyers in 2023 and 2024. At some point, when interest rates and thus mortgage rates began to return to more stimulative levels, there was going to be a conflict between this lack of supply and pent-up demand. Let’s look at a chart and then comment:

We have already seen major markets start to see a sales recovery with resales up significantly year-over-year in most major markets. Add to this ~150 basis points of further interest rate cuts (see above) and we would expect that this predicted sharp rise in home prices is likely to begin unfolding in 2025.

Canadian Dollar – Surprising Resilience

The obvious answer for the Canadian dollar would likely be lower, potentially breaching the $0.70 level as it did in the early 2000s. The Canadian economy remains in a self-inflicted funk, while Trump 2.0 promises to bring tariffs and higher U.S. oil production (negative for oil prices and thus CAD). And yet, we would not be surprised to see CAD hold around current levels and potentially even surprise back to the mid-$0.70’s range as the year progresses. Let’s first look at a chart and then comment:

We are looking at a chart of the Canadian dollar vs. the U.S. dollar over the past decade. As you can see, CAD has now spent the better part of the past 10-years between $0.70 and $0.80 – in fact, 90% of all trading days between the beginning of 2015 and now. This is remarkable stability that has withstood Trump 1.0, two periods in which oil prices dipped below $30/boe, COVID, a massive growth gap relative to the U.S. and a myriad of other challenges.

And yet, the consensus is that CAD is set to buckle and perhaps establish a new trading range between $0.60 and $0.70. Our view is:

- The issues facing Canada and the Canadian dollar are well known. While Trump 2.0 could be worse than Trump 1.0 for Canada, we see no evidence to support that other than some angry Truth Socials (we are legally and morally estopped from calling these Tweets). Further, Trump himself hailed the USMCA as the greatest trade deal ever and while he often makes bold claims like he invented the question mark, we are not sure how casting aside the USMCA supports this “greatest ever” claim. We would also add that ~30% of Canadian exports to the U.S. are oil and other commodities. Imposing tariffs of any size on Canada would risk sparking a new round of inflation in the U.S. not only at the pump, but also across a variety of sectors that require these Canadian raw material imports, which was likely not what people in the U.S. voted for this past November.

- A change of government in Canada is likely coming. As we wrote a couple of weeks back, 2024 was a terrible year to be an incumbent and we do not see any indication that this will change in 2025. Current polls (source: CBC) give the Conservative Party a ~19-point lead and a 94% chance of a majority government. While we will not speculate as to how the Conservatives would actually govern, we think that the “tonal shift” for investors looking at Canada as a potential place for their investment dollars could be a very important one. Our discussions with investors both inside and outside Canada have not surprisingly been largely negative – “why would I want to invest there?” – over the past several years as high tax rates, a spiderweb of rules and regulations, high debt levels and an overall lack of economic growth have combined to stunt investment interest. More recently though, we have begun to see fund flows into Canada pick up and while we have yet to see anyone turn outright bullish, we think there are reasons for optimism, especially given how unloved Canada has become.

Stocks – Continued Strength in the U.S. and Canada

For better or for worse, the U.S. market is generally going to be the tail that wags the dog for equity investors. Thus, we will start with some general thoughts about our outlook for the U.S. market and then pivot to Canada. Let’s start with a chart and then comment:

The U.S. market has been on an incredible tear both in absolute and relative terms since the beginning of 2012 – outperforming most major indices by 200-300%. This has been due to a combination of factors, including better economic growth, a significant reduction in corporate and personal tax rates, and most importantly – much more relative exposure than other markets to major investment themes such as cloud computing and now, artificial intelligence.

This outperformance has driven a significant valuation gap between the U.S. market and all other markets with the U.S. trading ~7x multiple points higher than Canada and 9-10x higher than Europe, the U.K. and Japan. Despite this valuation premium, we think the overall outlook for the U.S. market in 2025 is strong. This is based on a combination of:

- Tax cuts and deregulation: While Trump 1.0 was largely ineffective in achieving most of its policy goals (remember repealing the ACA and “infrastructure week”), it did prove effective in both cutting taxes and rolling back regulations. We would not be surprised to see more of the same in 2025 and this should help create a positive backdrop for stocks, which generally like tax cuts and deregulation.

- A more accommodative Fed: We have been skeptical of the fall Fed rate cuts as we are not sure the inflation genie in the U.S. has been put back into the bottle nor are we entirely sure why a strong U.S. economy needs the relief. Regardless, with Trump returning to the White House, we would expect a more accommodative Fed than the data supports as Trump 1.0 showed that the Powell Fed can and will be bullied. This could create an inflation issue for 2026 as the stimulus from tax cuts and deregulation coupled with interest rate cuts (not to mention deporting a large chunk of the workforce) is potentially a toxic inflation stew, but this is likely something we will worry about in the back half of 2025 as opposed to now.

As for Canada, for many of the reasons we outlined with CAD, we expect 2025 to be a strong year for Canadian stocks. As we have written previously, both the Canadian economy and the Canadian stock market tends to be more interest rate sensitive and with the Bank of Canada likely to cut rates another ~100-150 basis points over the next 12-months, this should help to create an accommodative backdrop. Add to this improving sentiment from investors both inside and outside Canada and valuations that remain reasonable, and we would not be surprised to see the TSX, which currently sits ~25,600, approach 27k or even 28k at some point in 2025.

Final Thoughts

We have an optimistic view of the investment landscape for 2025. While inflation risks, especially in the U.S., have not gone away, we think that this is likely to be a 2026 issue as opposed to a near-term concern. The backdrop should provide cover for the Bank of Canada and to a lesser extent the U.S. Federal Reserve to reduce interest rates, providing relief to consumers and the economy. Add to this a strong U.S. economy that is likely to get a lift from further tax cuts and deregulation and the overall backdrop is favorable, despite some valuation concerns in the U.S. Our biggest concerns are those that are unlikely to impact the investment landscape and something that we will leave for a future missive.