Hello,

Conflict has broken out in the Middle East, introducing a new layer of uncertainty for the economy and markets. The situation remains fluid, but I outline below some of the potential implications of recent geopolitical developments for Canada, the U.S., and the broader global economy.

The Fog of Geopolitics

On February 28, the U.S. launched a large-scale military offensive against Iran following weeks of military buildup in the region. The escalation materially increased geopolitical risk and injected renewed volatility into financial markets. Equity markets retreated and bond yields edged higher in response to a sharp rise in energy prices amid worries of supply disruptions tied to a potential prolonged closure of the Strait of Hormuz—one of the world’s most critical energy transit routes.

In moments like these, I believe considering history provides valuable perspective. While geopolitical shocks often generate short-term market turbulence, occasionally severe, they have historically had limited influence on longer-term market direction. Across roughly two dozen significant military conflicts since 1950, the S&P 500 delivered positive returns twelve months later nearly three-quarters of the time. Markets typically adapt as uncertainty gradually gives way to clearer policy direction and improved economic visibility, making these episodes more transitional than structural in nature.

Nevertheless, military conflicts are inherently unpredictable. As such, the balance of risks surrounding the economic outlook has likely worsened at the margin. In my view, oil prices remain the key transmission channel to monitor. The $100-per-barrel level represents an important psychological and economic threshold, as sustained increases could adversely influence consumer spending and inflation. I expect financial markets will remain sensitive to energy prices in the near term, and a durable decline in oil would help build confidence that tensions are receding and market volatility could begin to normalize.

Despite heightened uncertainty, macro conditions remain reasonably constructive. The world economy was on a sturdy foundation prior to the conflict, underscored by broadening growth momentum and strong corporate earnings trends. This suggests to me that businesses and markets entered this period of geopolitical tension from a position of relative resilience.

Global and U.S. Implications

Energy markets have been exceptionally volatile, with oil prices moving within a wide range as investors attempt to gauge the likely duration and intensity of the conflict. Ultimately, how high oil prices rise—and how long they remain elevated—will be a key determinant of the broader economic impact. The impact is likely to vary significantly across regions, particularly between energy-importing and energy-exporting economies. Europe and much of Asia remain heavily reliant on imported energy, leaving them more vulnerable to higher inflation and weaker growth if oil prices stay high.

The U.S. appears somewhat better positioned to absorb an energy shock. The amount of oil required to produce one unit of GDP is about 70% lower than in the 1980s, and the country’s position as a net energy exporter reduces its direct exposure to supply disruptions. Reflecting these dynamics, U.S. equities—while lower since hostilities began—have generally held up better than many international peers, while the U.S. dollar has strengthened against most major currencies. That said, a prolonged period of elevated oil prices would still represent a headwind for the American economy by placing pressure on discretionary consumer spending and raising input costs for businesses. Meanwhile, the combination of potential inflationary pressures and slower growth could complicate the Federal Reserve’s policy outlook, with markets recently paring back expectations for near-term rate cuts.

Implications for Canada

Canadian equities have also declined since the conflict began, though the S&P/TSX Composite Index remains in positive territory year to date. The Canadian market’s significant weighting in the Energy sector has provided support, helping to offset weakness in other sectors. Energy accounts for roughly 15% of Canada’s goods exports and approximately 6% of GDP, suggesting that the country could see some modest economic benefit from higher oil prices.

However, Canada’s ability to fully capitalize on rising prices is constrained by limited pipeline capacity, which restrains how quickly exports can increase. As elsewhere, higher oil prices have mixed economic effects: stronger revenues for energy producers and governments, but higher fuel costs for households and businesses. For interest rates, the potential for renewed inflationary pressure tied to the conflict has added uncertainty to the outlook for the Bank of Canada’s benchmark rate, with futures markets now pricing in some probability of monetary policy tightening in the second half of the year.

Takeaway

Markets dislike uncertainty. Renewed Middle East conflict has produced the expected reaction: uncomfortable volatility alongside sharply higher energy prices. The key unknown, which markets are struggling most to assess, is the length of the conflict. Inconsistent messaging from the U.S. administration has added to the uncertainty, limiting visibility for investors.

The economic outlook understandably feels less certain than it did two weeks ago, and I am closely monitoring for signs that financial or economic stress may be emerging. With a wider range of possible outcomes now in play, maintaining discipline becomes especially important.

While markets may remain unsettled in the short term, longer-term outcomes ultimately reflect fundamentals such as economic growth and corporate earnings trajectory. In my view, recent events continue to highlight the value of diversification and remaining aligned with long-term investment goals as a prudent approach to navigating inevitable periods of uncertainty.

Highlights

In search of a nail

The Federal Reserve wields a powerful hammer with its ability to move interest rates. Despite its strength, though, we think the central bank is poorly suited to address key concerns arising from high oil prices and the rollout of AI.

Regional developments: Canada better positioned than global peers to weather higher crude prices; U.S. Treasury yields advance to multi-month highs amid Middle East tensions; Energy price shock reshapes Europe-UK interest rate expectations; Investors assess Asia's energy vulnerability

Please take some time to review the Global Insight Weekly.

New deals to unlock projects worth $12.1 billion in Canada’s critical minerals sector

Energy and Natural Resources Minister Tim Hodgson announced government support for several projects at the Prospectors & Developers Association of Canada mining conference in Toronto. The investments are part of the G7’s Critical Minerals Production Alliance, a Canada-led initiative, and include a rare earth elements recycling centre in Ontario and a $7-million contribution to a Toronto-company operating a mine in Greenland that produces tungsten and molybdenum, critical minerals used for defense.

All income groups in Canada have improved their net wealth since 2019

Despite economic headwinds, appreciation in home prices—up 25% nationally since 2019, despite recent pullback—and growth in non-pension financial assets (such as equity market profits) drove wealth gains, according to a new report by RBC Economics. Surprisingly, these gains have favoured lower-income groups, leading to a sizeable narrowing of the wealth gap, with the ratio comparing the wealth of the top quintile to the bottom two compressed from 3.2 times in 2019 to 2.1 times in 2024.

Rising Canada-China trade boosted cargo flows at the Vancouver Port

The country’s largest port handled a record 170.4 million tonnes last year of imported and exported cargo. Exports of crude oil, grain and potash hit record levels. China—Canada’s biggest trading partner at the West Coast—accounted for 52.6 million tonnes of exported and imported cargo last year, rising 15% from 2024. Canada-U.S. trade also jumped 12% to 11.6 million. The Port of Vancouver handles more cargo annually than the next five largest ports in Canada combined.

RBC Economics raised its inflation forecast for Canada and the U.S.

Following an upgrade to its oil price assumptions, the consumer price index is now projected to be 2.4% for Canada and 2.9% for the U.S. on average for 2026—0.2 percentage points higher for both compared to a previous forecast. U.S. inflation was steady at 2.4% in February but that was before the U.S.-Israel attack on Iran sent energy prices soaring. RBC expects the Bank of Canada and the U.S. Federal Reserve to look through near-term volatility rather than rush to a response.

The U.S. lost 92,000 jobs in February in a surprising downturn

That was far short from expected gains of 50,000 jobs, sending the unemployment rate higher to 4.4% from 4.3%. A public healthcare workers’ strike in California drove losses, but private sector jobs were also down 86,000. Trade-exposed sectors (manufacturing, transportation and warehousing) shed a combined 23,000 jobs, according to U.S. Labor Department data. December jobs gains were also revised from gains of 48,000 to a loss of 17,000 jobs—the economy has now shed jobs in five of the past nine months.

U.S. Opens Section 301 Probe to Rebuild Tariff Strategy

The Trump administration has launched a trade investigation into foreign manufacturing practices, aiming to restore tariff authority over certain countries after the U.S. Supreme Court struck down earlier tariffs imposed under emergency powers. The investigation will be conducted under Section 301 of the Trade Act of 1974, which allows the U.S. government to examine foreign policies or practices that may disadvantage American companies and potentially respond with tariffs. The probe will assess issues such as excess industrial capacity, government subsidies and labour conditions that may give foreign manufacturers an advantage over U.S. firms. Countries included in the investigation span major trading partners and export-oriented economies, including China, the European Union, Japan, India, South Korea, Mexico and several Southeast Asian producers. The administration currently relies on a temporary 10% global tariff under a different trade provision, which expires in a little over four months. Officials aim to complete investigations quickly to make new policy options available before that deadline. For Canada, which was left out of the investigation, focus remains on the upcoming Canada-United States-Mexico Agreement (USMCA) review scheduled for July 2026.

Israeli Officials Temper Expectations for Political Change in Iran

Israeli officials believe that Iran’s ruling system is unlikely to collapse in the near term. Despite almost two weeks of sustained military pressure from Israel and the U.S., Iranian political and military leadership remains operational, and security forces appear to maintain firm control over major cities. Israeli Prime Minister Benjamin Netanyahu said it is uncertain whether the Iranian public will ultimately overthrow the regime, though he argued the war could weaken it significantly. Yesterday, Israeli military officials framed their campaign’s objective as reducing Iran’s military threat—particularly its missile capabilities and broader security apparatus—rather than regime change. On the ground, Iranian authorities have reinforced domestic control, deploying units linked to the Islamic Revolutionary Guard Corps and Basij militia across urban areas. Residents report a heavy security presence and warnings that protests could be met with lethal force, discouraging potential demonstrations despite underlying dissatisfaction with the government. Israeli officials say broader political change could require a longer period of military and economic pressure.

Charts of the Day

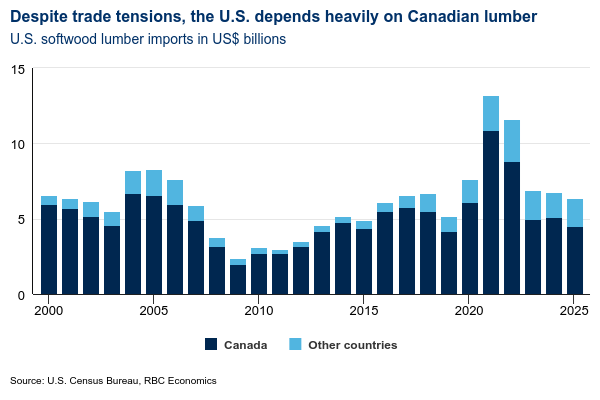

Decades of trade disputes reshape Canada's softwood lumber sector

Subsidies & Speed Bumps: The road ahead for Canada's auto strategy

Interesting tidbits

- Tea vs coffee: Which is the best drink for your gut, heart and brain? Two nutrition experts compared Britain’s favourite hot beverages to find out which is most beneficial for overall health. This interesting article highlights their key findings.

- British Columbia is has clocked out from daylight saving time. The province shifted clocks forward an hour for the last time on March 8, and has now abandoned the twice-yearly practice of changing clocks to capture daylight. The move will push B.C. an hour ahead of its continental West Coast neighbours California, Oregon and Washington from November to March. Alberta Premier Danielle Smith said the province should also consider abandoning the practice of changing clocks twice a year. Saskatchewan and Yukon are currently the only two jurisdictions that don’t participate in DST in Canada.

- Young Canadians are reluctant to buy cars. Vehicle ownership among Canadians aged 25-34 declined 9%, according to a study by car rental platform Turo, even as it stayed flat for the average population. Around 36% of Gen Z don’t own a car compared to 15% of the general population, the survey shows. S&P Global data also showed new vehicle registrations by the 18-34 age group fell below 10% in the second half of 2025, from 12% four years ago. Rising insurance and vehicle prices and affordability issues are cited as key factors.

- Nearly two-thirds of the electronics that Canadians throw out still work. The University of Waterloo study, featuring 800 homes across nine provinces, looked at the lifespan of everything from cellphones to washing machines. A broken key on a laptop was considered repairable—and therefore functional. Between 2025 and 2030, the authors predict e-waste in Canada could top 2.3 million metric tonnes, which they equate to filling 18 CN Towers full of garbage. Previous research by one of the authors found that e-waste had tripled over the past 20 years.

Today's Funny

REMINDER: Most of my new clients come to me via word of mouth as I don’t advertise or engage in marketing programs. Please keep my team in mind if you hear of anyone with over $1 million in investable assets who is in need of wealth management services.

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that any action is taken based upon the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein.