A word from Mike

Hello,

Despite resilient equity markets, headline-driven uncertainty persisted through February, with tariffs and technology in focus. I discuss these themes, alongside North American corporate earnings trends and the implications for Canadian trade, in more detail below.

Solid Corporate Earnings

As the Q4 2025 earnings season for the S&P 500 draws to a close, the index has achieved its fifth consecutive quarter of double-digit earnings growth. However, the “beat rate”—the share of companies exceeding profit expectations—moderated. In an environment where valuations remain elevated, a narrower gap between reported results and forecasts could leave markets somewhat more sensitive to disappointments or adverse macro shocks.

Earnings results from some Big Tech firms were closely watched as a test of whether heightened AI-linked expectations can be maintained. Investors are increasingly looking for clear evidence that substantial AI investments are translating into tangible returns, amid questions around profit growth visibility and the potential for AI-driven disruption in certain industries. This skepticism was evident when a major AI infrastructure firm recently delivered a “beat and raise”—exceeding revenue forecasts and lifting forward guidance— and was met with a subdued market response. Nevertheless, the Big Tech group, broadly speaking, remains supported by durable business models and reliable cash flow generation.

North of the border, Canadian firms are also wrapping up their 2025 reporting season, while major banks reported Q1 2026 results. Bank earnings have been positive, with record profits driven by solid performance across key divisions alongside improved return on equity (ROE). Despite trade and geopolitical uncertainty, consensus estimates for the S&P/TSX Composite Index continue to point toward double-digit earnings growth this year, underpinning a constructive outlook for Canadian equities.

More Tariff Developments

Last week, the U.S. Supreme Court struck down some tariffs imposed by the Trump administration under the International Emergency Economic Powers Act (IEEPA). The market reaction was largely muted as investors had anticipated both the ruling and efforts by the administration to reinstate tariffs through alternative legislations.

Accordingly, a 10% global tariff on U.S. imports came into effect earlier this week, with the White House indicating that could increase to 15% "where appropriate". Implemented under Section 122, these levies can remain in place for 150 days without Congressional approval. However, Section 122, designed to address balance-of-payments emergencies, is also likely to face legal challenges. Given the current composition of Congress, a vote to extend the tariffs appears unlikely, but the temporary measure provides time for the administration to restructure its tariff policy.

Other legislative pathways, such as Sections 232 and 301, require formal investigations into national security risks or unfair trade practices but tend to offer more durable legal grounding. Still, the Supreme Court’s ruling reaffirmed that presidential authority over tariffs is not unlimited, reinforcing constitutional checks and balances and underscoring that more permanent trade measures require a more rigorous procedural path.

For Canada, the immediate economic impact remains limited. Roughly 90% of Canadian exports to the U.S. continue to flow tariff-free under exemptions within the U.S.-Mexico-Canada Agreement (USMCA). Meanwhile, sectoral tariffs on metals, autos, and other targeted parts of the Canadian economy imposed under Section 232 remain in effect and continue to weigh heavily on certain industries. As such, the scheduled USMCA review in July remains more consequential for Canada’s economic outlook, alongside ongoing efforts to diversify trade and invest in domestic capacity.

The base case remains that the core agreement framework stays intact, given deeply integrated North American supply chains and the shared economic costs of disruption. That said, I expect negotiations to involve political signaling and sector-specific pressure points that could stoke near-term uncertainty. I am monitoring developments on this front closely.

Takeaway

While markets remain susceptible to shifts in sentiment given elevated valuations and policy uncertainty, strong corporate earnings momentum provides grounds for measured optimism. Trade uncertainty continues to influence business and consumer confidence, but equity markets are primarily driven by earnings over time. Against a backdrop of steady economic fundamentals, I believe maintaining a cautiously constructive stance in portfolios remains sensible.

Highlights

A mature but still intact equity bull market

The 2022–2026 bull market is mature but intact after a 100 percent rebound by the S&P 500 and 150 percent rally by the Nasdaq 100 from the Q4 2022 lows. While valuations remain a headwind, U.S. equity markets remain above key technical support levels with potential for another round of sector rotation developing heading into Q2.

Regional developments: The Government of Canada lays out a plan for its Defense Industrial Strategy; Tariffs and AI continue to impact U.S. markets; EU suspends U.S. trade deal ratification; China recorded strong tourism growth during New Year holiday.

Please take some time to review the Global Insight Weekly.

Mark Carney is expected to strike a flurry of deals in India

The Prime Minister’s visit will cement a diplomatic reset after strained ties with New Delhi in recent years. The new chapter aims to focus on unlocking new trade and investment opportunities in nuclear power, oil and critical minerals. The Asian nation is also keen to buy Canadian heavy crude and other energy products, and is reportedly exploring potential investments in pipelines, terminals and other infrastructure. Peas, power aircraft and potash are Canada’s top three exports to India.

Inflation rate in Canada cooled to 2.3% in January

A decline in gas prices on a yearly basis pulled the overall inflation index down from 2.4% in December. Pockets of price growth are still high, with food purchased from stores rising 4.8% year-over-year in January, albeit slower than the 5% increase in December. Since early 2024, growth in shelter costs has slowed year over year. In January, prices continued to decelerate, rising 1.7%—the first time in nearly five years that year-over-year shelter price growth has fallen below 2%.

Canada's job growth stalled in 2025 amid trade and demographic headwinds

Canada's labour market lost momentum in 2025 as trade tensions and demographics shifts weighed on hiring. Payroll employment fell by 28,300 positions - with Ontario bearing the brunt of the job cuts - while roughly 37,000 manufacturing jobs were shed as U.S. tariffs curbed production in autos, warehousing and related industries, according to data released by Statistics Canada. At the same time, tighter immigration policies and a decline in temporary residents slowed population growth, dampening both labour supply and demand. Despite a broadly steady unemployment rate, labour demand softened, with job vacancies slipping to 514,600 in December and the vacancy rate falling to 2.9%, near pre-pandemic levels. Employers remain cautious amid ongoing trade uncertainty, and policymakers are increasingly watching early signs that AI may reduce entry-level jobs. While service industries have supported employment in recent years, economists warn that they could begin to soften. Food and accommodation vacancies may also rise as fewer temporary workers and international students remain in Canada over the near term. A key takeaway is that Canada's labour market appears to be entering a softer, more structurally constrained phase, where trade uncertainty, slower population growth, and potential AI-related disruptions collectively point to more modest job gains and a subdued growth backdrop in the quarters ahead.

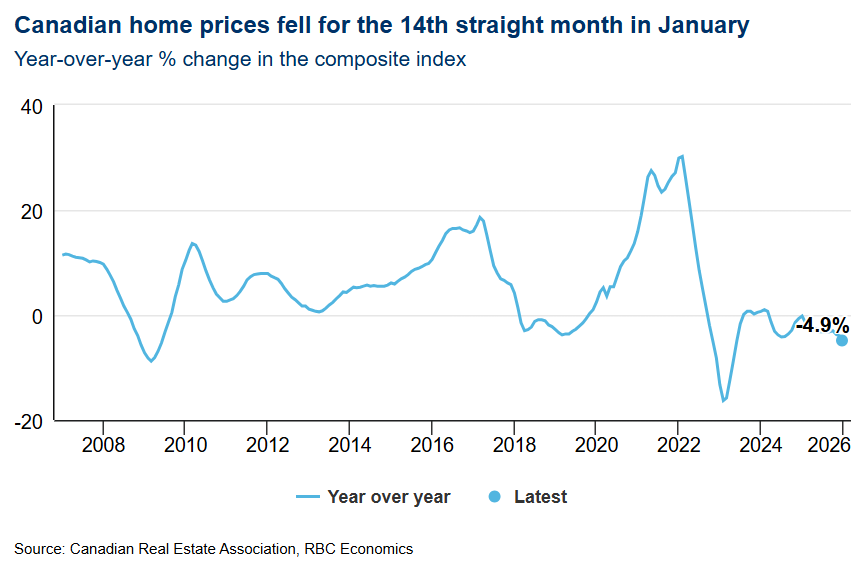

Canadian housing market had a chilly start to the year

Sales of existing homes fell 5.8% month-on-month in January as winter storms and frigid weather played a role in lower sales activity. Benchmark prices fell 0.9% in January to $665,200—the lowest level in almost five years—and are now down 4.9% on a year-on-year basis, according to the Canadian Real Estate Association. There was also a burst of new supply in Montreal, Quebec City, Calgary, Greater Vancouver and Victoria—although areas in Central and Southwestern Ontario posted declines.

New U.S. tariffs set at 10%, lower than the 15% previously expected

The United States has implemented a new 10% tariff on most non-exempt imports, a lower rate than the 15% previously signaled by President Trump, following a Supreme Court ruling that invalidated earlier tariffs imposed under the International Emergency Economic Powers Act (IEEPA). The new levy, authorized under Section 122 of the Trade Act, applies broadly but allows for exemptions and can last up to 150 days without congressional approval. While the reduced rate is viewed as less severe than expected, the lack of clarity on whether it would later rise to 15% has contributed to continued policy uncertainty and mixed market reactions. The court decision also halted the collection of earlier tariffs - some as high as 50% - raising questions about potential refunds for affected companies. Trading partners have responded cautiously, with some urging adherence to existing agreements and others, including China, calling for renewed dialogue while keeping potential countermeasures under review. Altogether, the narrative around tariffs remains fluid and underscores ongoing tensions and legal constraints shaping U.S. trade policy.

Charts of the day

Canadian homebuyers get cold feet, sellers out in force in January

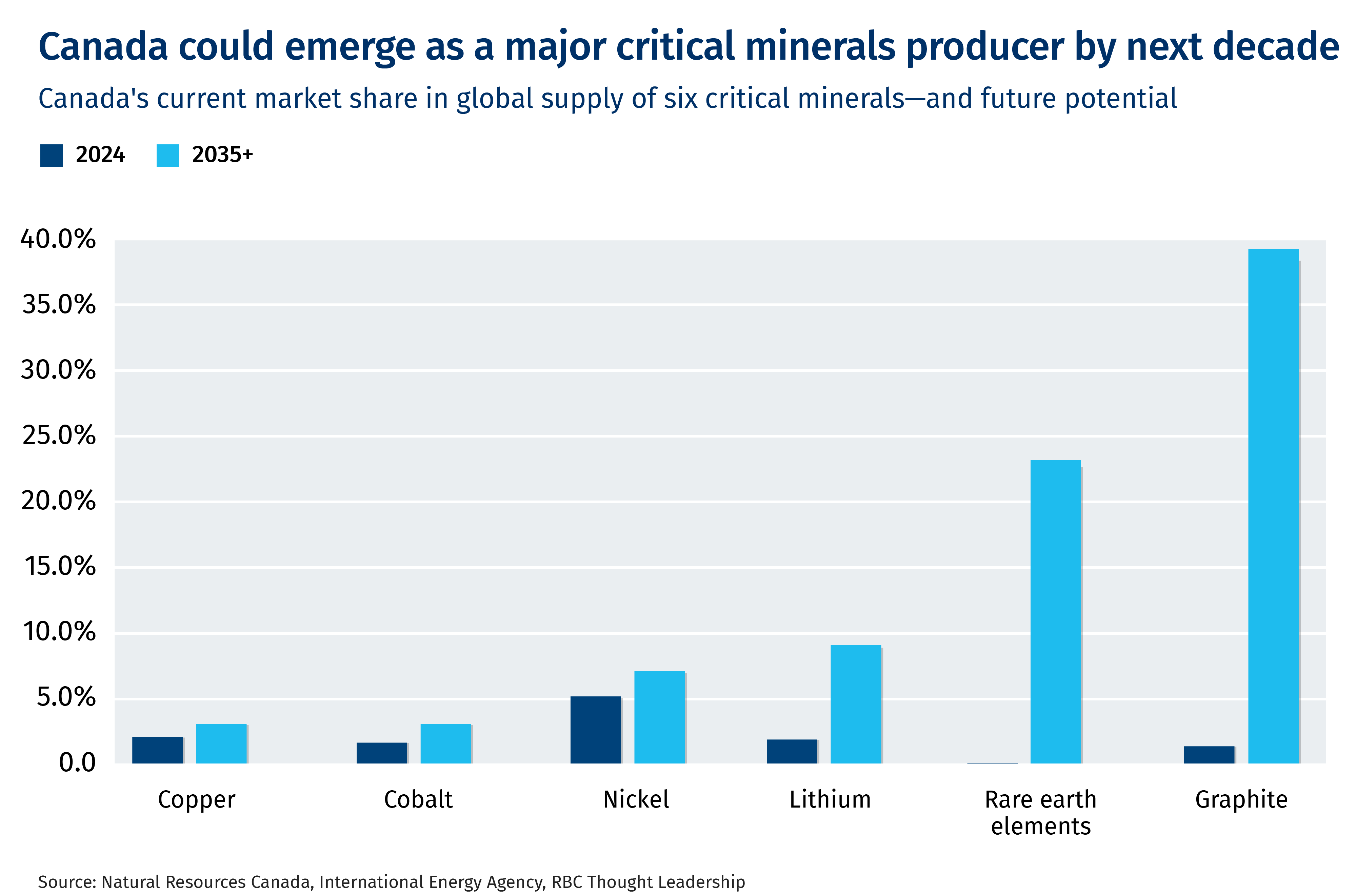

Mine & Refine: Bridging Canada's Critical Minerals Capital Gap

Interesting tidbits

-

$30.5 billion. The dollars Canadian residents splurged on domestic tourism, up 11.1% year-on-year in the third quarter, as Canada Strong Pass provided an incentive to spend at parks and museums. Canadian spending abroad fell 8.6% to $11 billion during the period.

-

Some Canadian airlines are cutting back flights to the U.S. WestJet said the airline had seen a notable decline in transborder travel demand and is suspending 16 Canada-U.S. routes as it expects the trend to persist in the “foreseeable future.” Air Transat is halting flights to two popular Florida destinations, Fort Lauderdale and Orlando, by June. However, Porter Airlines said it is adding flights to Austin and expanding operations at Chicago. Canadian-resident trips to the U.S. had fallen 23.6% year-on-year in November, latest Statistics Canada data shows.

-

Uber Air is ready to take off. The transport and delivery company is teaming up with Joby Aviation to start all-electric air taxis in Dubai, UAE, later this year. Long-term plans include touch downs in major U.S. cities, once American regulators complete the certification process. The aim is to serve passengers in time for the Los Angeles Olympic Games in 2028. California-based Joby has completed 50,000 miles of flights tests across its fleet. The two partners plan to expand the market globally, including the United Kingdom and Japan.

Today’s funny

REMINDER: Most of my new clients come to me via word of mouth as I don’t advertise or engage in marketing programs. Please keep my team in mind if you hear of anyone with over $1 million in investable assets who is in need of wealth management services.

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that any action is taken based upon the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein.