A Word from Mike

Hello,

Markets have entered the new year digesting a steady stream of headlines, underscoring the importance of staying focused on fundamentals. I discuss geopolitics, corporate earnings, and monetary policy in more detail below.

Geopolitical flashpoints

The year has begun with heightened geopolitical activity, led by U.S. actions in Venezuela alongside renewed tensions involving Iran and Greenland. In Venezuela, the removal of President Nicolás Maduro and the possibility of U.S. involvement in rebuilding the country’s oil sector have revived expectations that production—currently near 1 million barrels per day—could rise over time. However, decades of underinvestment, infrastructure decay, corruption, and political instability suggest that any supply recovery would be slow, costly, and complex.

For Canada, the longer-term risk is competition from Venezuelan crude for U.S. refiners, which rely heavily on Canadian supply. That said, Canada benefits from an entrenched pipeline network into the U.S. and improved export optionality following the Trans Mountain Pipeline expansion to the west coast, both of which should help preserve market share. Canadian energy equities initially reacted negatively to developments in Venezuela, reflecting concerns that U.S. refiners could substitute Venezuelan barrels for Canadian crude, potentially widening the WCS-WTI differential—the price spread between Canadian heavy oil and the benchmark—which would create a headwind for Canadian producers. This market response may be underappreciating the significant time and capital required to materially lift Venezuelan production, as well as Canada’s improved export infrastructure.

Elsewhere, the U.S. administration has warned Iran about civilian harm in the regime’s suppression of widespread domestic protests and reasserted its desire to “acquire” Greenland. While these events underscore persistent geopolitical uncertainty that may bring episodes of market volatility, the broader lesson from recent years has been the importance of maintaining perspective—avoiding overreaction to headlines and focusing instead on economic fundamentals and corporate earnings trends.

Corporate earnings

Corporate fundamentals remain constructive. Forward earnings expectations across major markets continue to trend upwards, and the U.S. Q4 2025 earnings season began this week, with analysts expecting high-single-digit earnings growth for the S&P 500 Index. More broadly, after approximately 12% global earnings growth in 2025, consensus expectations point to a further 14% increase in 2026.

While a good deal of economic and earnings optimism may already be reflected in valuations—which remain above long-term averages and can thus leave markets more sensitive to negative surprises—consistent earnings delivery can help support elevated multiples. In this context, profit trends remain a key foundation for equity markets to extend their advance.

Central banks

In Canada, recent labour market data, notably the stabilization seen in trade-exposed sectors, could allow the Bank of Canada (BoC) to remain patient. RBC Economics expects the labour market recovery to be uneven, and with inflation near target, the BoC has flexibility to assess macro developments. As a result, both RBC Economics and futures markets expect the BoC’s benchmark rate to remain unchanged over the coming quarters.

In the U.S., markets are currently anticipating roughly 50 basis points of rate cuts over the next 12 months. However, uncertainty surrounding the legal status of certain tariffs continues to cloud the economic outlook and post a challenge for Federal Reserve (Fed) policymakers.

Separately, recent headlines regarding subpoenas served by the U.S. Justice Department related to Fed building renovations have renewed debate around central bank independence. Nevertheless, the near-term risks of a politicized Fed seem relatively contained, given the strength of U.S. institutional checks and balances. Notably, several prominent Republican senators have committed to defending the Fed through their authority to advance Fed nominations, and Fed Chair Powell’s vigorous response has likely increased the likelihood that he remains on the Fed’s board beyond the end of his term as chair in May. Importantly, market reactions typically associated with threats to central bank independence—such as higher inflation expectations—have remained muted, suggesting continued investor confidence in U.S. institutional safeguards.

Takeaway

While geopolitical developments and policy uncertainty may drive intermittent volatility, corporate earnings and underlying economic fundamentals remain the primary drivers of equity markets. These factors continue to look supportive in the quarters ahead. In my view, maintaining an “invested, but watchful” approach remains prudent.

________________________________________

Highlights

Global Insight Monthly

January 2026

I am pleased to share the latest investment strategy report from RBC Wealth Management—Global Insight, which provides our current thoughts on asset classes, the economy, and timely issues that impact investment strategy.

Full report: Global Insight

This month’s highlights:

Building on a narrow base

Long-term economic trends have left the U.S. economy increasingly reliant on spending by upper-income households. We unpack the potential implications for economic stability and Federal Reserve policymaking.

Global equity: Navigating 2026 growth, AI momentum, and election-year dynamics

Equity markets appear poised for moderate gains, driven by easing inflation, rate cuts, and steady earnings. AI promises more near-term capital spending and future productivity boosts, while election-year dynamics usually spark volatility in both directions.

Global fixed income: A slow start out of the gates

Last year saw most central banks ease policy rates. 2026 will likely see different courses of action.

________________________________________

Canada’s Free Trade And Labour Mobility Act is now in effect

The law to break down interprovincial trade barriers is among a slew of rules rolled out on January 1. The year 2026 will also be the first full year the federal income-tax rate will fall to 14% from 15%, while RRSP contributions are rising to $33,810 from $32,490 in 2025. In Ontario, employers will be required to disclose the expected compensation or salary range for any public job posting, and whether artificial intelligence is used during the hiring process.

Canada and China Sign Agreements

During a visit to Beijing on Thursday, Canadian Prime Minister Mark Carney announced a series of agreements with China aimed at expanding trade, strengthening investment, and increasing collaboration. The nations unveiled a general plan for a warmer trade partnership after relations have been strained for a number of years, including a signed document that states Canada "welcomes Chinese investments in Canada in areas such as energy, agriculture, consumer products and other sectors." Canada will import 49,000 Chinese electric vehicles at a tariff rate of ~6%, down from the current 100% duty. In exchange, Carney stated he expects China to cut tariffs on Canadian rapeseed and that China would offer visa-free travel to Canadians. Canada anticipates canola tariffs to fall from 85% to ~15% by March 1st along with a suspension of anti-discrimination duties on other farm products.

Canada’s U.S. export share hit a record low

In a sign of trade diversification, the share of Canadian exports destined for the U.S. dropped to 67.3% in October—the lowest level since 1997, outside the pandemic. Overall, the country’s merchandise trade balance swung into a deficit of $583 million in October, according to Statistics Canada. It was driven by imports rising 3.4% year-over-year, led by record shipments of computers and computer parts. Gold shipments, largely to the U.K., resulted in a 2.1% increase in exports.

U.S. and Taiwan Sign Trade Deal

The U.S. and Taiwan have signed a trade agreement by which tariffs on Taiwan would fall from 20% to 15%, on par with rates faced by Japan and South Korea. In exchange, Taiwan's tech industry will commit to increase financing for American operations by $500 billion. This includes $250 billion in direct investments to expand advanced semiconductor, energy, and AI operations in America along with another $250 billion in credit guarantees for additional investment in U.S. semiconductor supply chains. The U.S. is also set to increase investments in critical Taiwanese sectors including semiconductors, AI, defense, and biotechnology. The deal also imposes limits on sector-specific U.S. tariffs on auto parts, timber, lumber and wood derivative products at 15%. While some details, including how the looming Supreme Court decision on tariffs will dictate the administration’s scope to unilaterally set tariffs on foreign trading partners, are unclear, the deal removes a key overhang for the Taiwanese economy.

China Trade Surplus Grew in 2025

Increased exports to non-U.S. markets in the face of trade war volatility throughout 2025 led China to report a record trade surplus of almost $1.2 trillion. Exports from the world's second-largest economy grew 6.6% y/y in value terms while imports grew 5.7% y/y, both exceeding Reuters forecasts for 3.0% and 0.9% growth, respectively. Exports to the U.S. fell 20% and imports from the U.S. fell 14.6% in dollar terms throughout 2025, but outbound shipments to Africa, the Association of Southeast Asian Nations (ASEAN), and the European Union all increased. Following the data release, a Chinese customs administration minister stated that "with more diversified trading partners, (China's) ability to withstand risks has been significantly enhanced." While trade resilience has helped insulate the export-reliant economy, a persistent property downturn, deflationary pressures, and sluggish domestic demand pose continue to pose challenges in the year ahead.

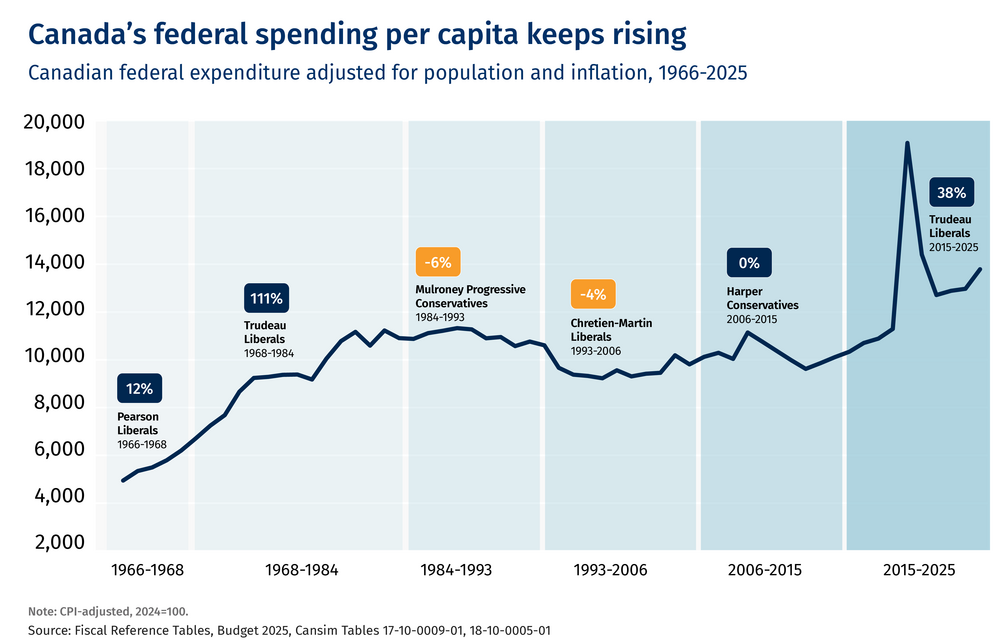

Charts of the day

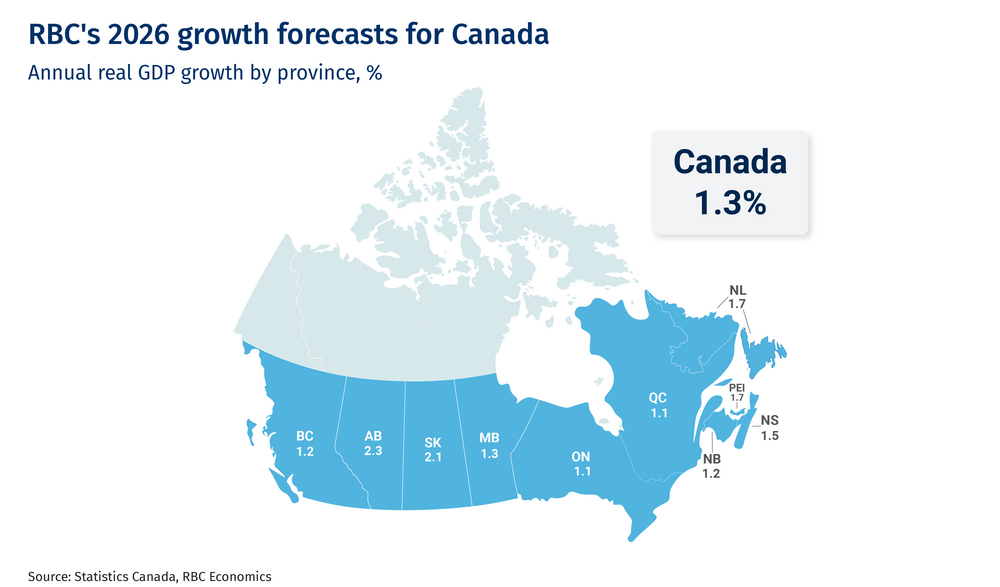

Beyond the forecast: Six themes for Canada’s economy in 2026

Interesting tidbits

- Most top-performing adults were not standouts in their youth. A new study of world-class performers, including Olympians and Nobel laureates, showed little connection between early success and elite performance later in life. Just 10% of high-performing children remained elite at their peak performance age as adults, which was defined as between 20 and 30 for sports and between 40 and 50 for music and science. The findings, based on data from more than 20 previously published studies, challenges the theory that success comes from specialized early training.

- $63,264. The average cost of a new car in Canada, according to latest data available from Autotraders. It’s a dramatic jump from $36,100 on average for a brand new car in 2018.

- Canadians took 28% fewer trips to the U.S. last year. The country’s residents visited their southern neighbour 22.9 million times in 2025, nine million fewer than the prior year as President Donald Trump’s trade war and suggestions of making Canada its 51st state hit a nerve. The U.S.’s immigration crackdown and extra scrutiny at the border also discouraged many. An Angus Reid Institute poll in October noted that seven in 10 Canadians were uncomfortable travelling to the U.S. this season. Fewer Americans also travelled to Canada, with visits falling 5% to 17.8 million.

- 9.35 years. The increase in longevity with 42-103 minutes of exercise and 7-8 hour sleep a day, a 60,000-patient study found. Additional 5 minutes of sleep, ½ cup of vegetables and two minutes of vigorous physical activity could add a year.

Today’s funny

REMINDER: Most of my new clients come to me via word of mouth as I don’t advertise or engage in marketing programs. Please keep my team in mind if you hear of anyone with over $1 million in investable assets who is in need of wealth management services.

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. will ensure that your own circumstances have been considered properly and that any action is taken based upon the latest available information. The strategies and advice in this report are provided for general guidance. Readers should consult their own Investment Advisor when planning to implement a strategy. Interest rates, market conditions, special offers, tax rulings, and other investment factors are subject to change. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein.