As investors continue to navigate the fluctuations and recent volatility of the stock markets around the globe. I wanted to highlight recent events this week, and give an update on the stimulus package the Canadian government has implemented to cushion the blow of the economic shocks from COVID-19 and the drop in oil prices.

A Weakened Canadian Dollar

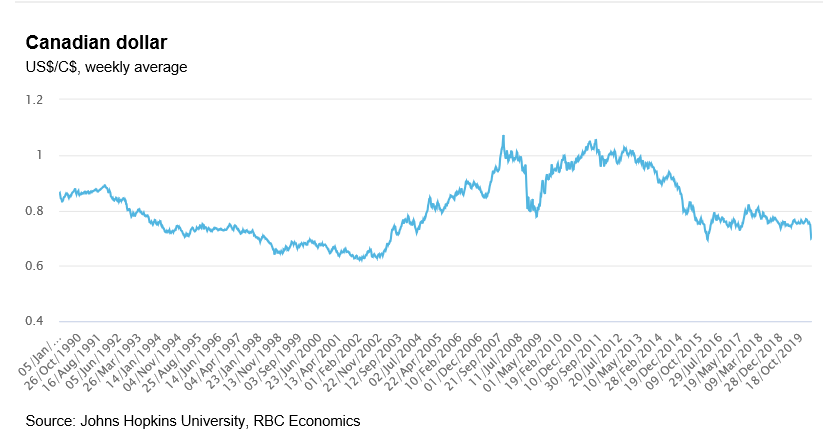

The Canadian dollar traded at below 70 cents this week. 2020 has been anything but stable for our Canadian currency, including a recent drop of 10% compared to our U.S. counterparts. The strengthening of the U.S. dollar has played a major factor for the recent spread and fluctuations and as market volatility creates a wave of panic, investor’s race to the security of the U.S. dollar. Factor in collapsing energy prices and the uncertainties surrounding the coronavirus, it seems obvious why the Canadian currency has been hit hard.

Among all the uncertainties, Canada has decided to join the likes of other commodity producing countries (Australia, Norway) and launching quantitative easing programs.

Easing the cost of borrowing

As of March 27, the Bank of Canada has decided to cut its benchmark interest target to 0.25%. This will be the second rate cut in two weeks in response to the damage evoked by COVID-19. The benchmark interest rate, or overnight lending rate, is what the bank charges for short-term loans between retail banks. The overnight lending rate in turn, impacts the rates Canadians receive from their banks (think savings accounts and variable rate loans, such as your line of credit). Cutting interest rates is a direct way to help stimulate the economy, a term known as “quantitative easing”.

The effects of “Quantitative easing”

Essentially, the Canadian government is using the similar program the U.S. Federal Reserve has done multiple times already over the last few weeks. The process of quantitative easing involves central banks printing more money, and using that money to purchase assets such as government and corporate bonds held by commercial banks and other financial institutions. By selling bonds to the government, financial institutions receive the cash necessary to lend more money and create economic activity.

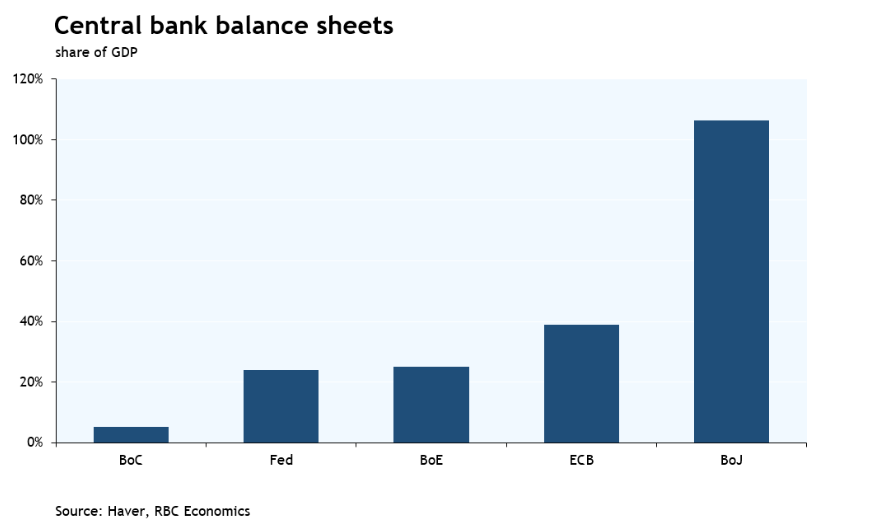

Today, central bank rates have hit historic lows (0.25% in Canada and 0 in the U.S.). The U.S. Federal Reserve and the Bank of England have also both implemented quantitative easing programs to help stimulate their economies and the Bank of Canada has now decided to follow suit.

In a stimulus package situation, no one really knows if the effects of quantitative easing will work. Only time will tell if the effects will help jump-start the Canadian economy, and intrigue the use of credit and borrowing.

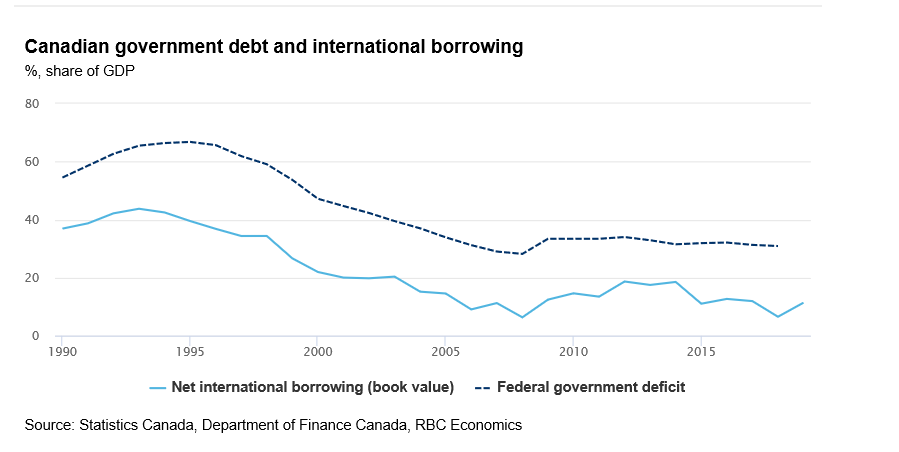

One thing to keep in mind is the use of such stimulus efforts come with risks. To purchase debt, the government needs to print money (or create it virtually) which could lead to higher inflation rates and devalue of currency. An aggressive approach could ensure that this doesn’t happen. However, Canada has also come a long way since the “Wild West” of the 1990’s where our Canadian government debt was roughly 60% of GDP. Today we stand in a much better position (our debt-to-GDP ratio now sits at 31% which has helped to improve our net international borrowing). The use of quantitative easing would certainly push us higher in debt, but to nothing we’ve ever seen before. In fact, other countries may be envious of our current stance in these uncertain economic times.

What is the Canadian Government doing?

As of Friday, the new program will involve the Bank of Canada purchasing $5 billion dollars of Government of Canada securities per week in order to relieve pressures on our financial system. The second program also includes the purchasing of commercial paper purchases, in addition to recent purchases of Canadian mortgage bonds, money market securities, and other liquid providing assets. Everything we are doing seems to follow the example of what countries have done before in 2009. The question is, what will the Bank of Canada do next if more stimulus is needed to start the economy? In this case, it will likely mean buying more government securities and increasing our levels of quantitative easing in a more dramatic fashion. As I mentioned previously, our balance sheet sits well to the effects and efforts of the Bank of Canada. We haven’t hit levels ever seen or even “stimulated” our economy as drastically as other countries.