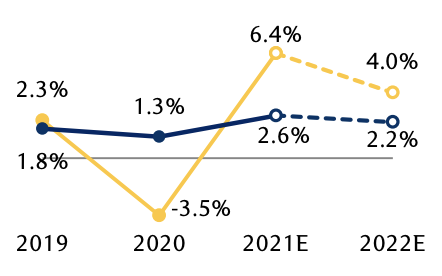

United States: Housing boom

United States: Housing boom

Economic data broadly positive amid vaccination rollout. ISM indexes firmly in expansion territory. New orders positive, inventories too low. Unemployment rate down to 6%, weekly unemployment claims falling. Strong payroll growth will result in all jobs replaced by early 2022. Home prices at 15-year high on record low supply. Core inflation barely below the Fed’s 2% target at 1.8% y/y. Near-term surge underway, but Fed policy unlikely to change.

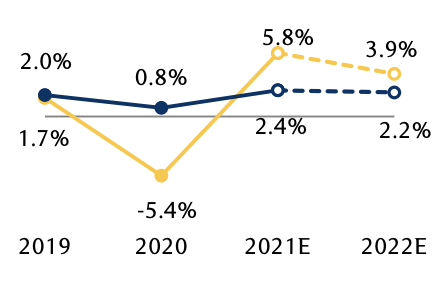

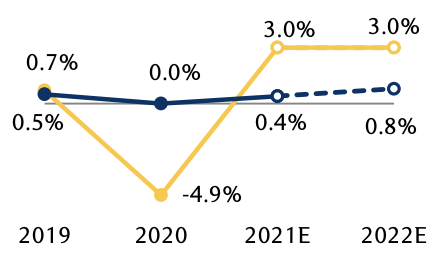

Canada: BoC sees brightening economic outlook

Canada: BoC sees brightening economic outlook

The BoC advanced the timeline to full economic recovery from the effects of the pandemic. Growth expectations up more than 2% to 6.5% for 2021, and inflation projected to reach 2% target by late 2022. The committee tapered asset purchases from CA$4 billion to CA$3 billion per week. Housing market worryingly strong as demand well ahead of supply. Unemployment rate at 7.5%. Third wave lockdowns temporarily dampening employment growth.

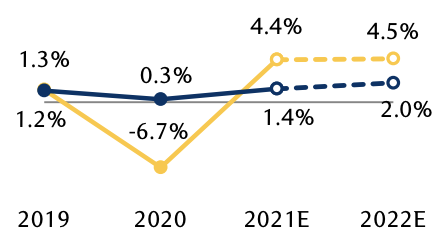

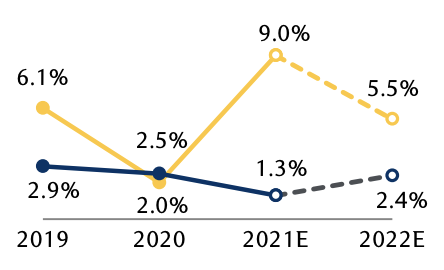

Eurozone: Manufacturing jumps to new record

Eurozone: Manufacturing jumps to new record

Double-dip recession arrived with Q1 negative GDP growth report. Largely a result of big hit to important services sector from widespread shutdown in response to third wave. Eurozone manufacturing hit a record high mostly due to continued strength in Germany’s output. European Central Bank kept its very stimulative monetary policy unchanged. After a slow start, vaccinations have picked up, which should lead to gradual reopenings throughout May. Tourism rebound expected in H2.

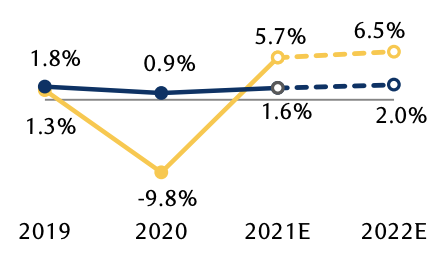

UK: Expecting faster growth

UK: Expecting faster growth

Bank of England (BoE) Deputy Governor Ben Broadbent recently said he expects to see “very rapid economic growth at least over the next couple of quarters.” Consumers expected to spend as much as 5% of savings banked during pandemic. Manufacturing and industrial output climbed with transport equipment as well as computer, electrical, and optical equipment leading the way. Pent-up demand drove stronger-than-expected retail sales.

China: Domestic slowdown

China: Domestic slowdown

China’s official and Caixin PMIs indicate domestic economy is slowing while external demand remains strong. Construction indicators show infrastructure investment has weakened in response to government efforts to rein in lending. The dynamic phase of the recovery from the pandemic appears to be over with slower growth projected going forward as the government deals with distortions in the debt market.

Japan: Consumer slump following shutdowns

Japan: Consumer slump following shutdowns

GDP has been recovering on the back of very strong exports and manufacturing. Consumer and business confidence on the rise. Despite these positives, Q1 GDP expected to retreat as COVID-19-related shutdowns hit consumer spending. Recovery expected to pick up speed late in Q2. Bank of Japan to maintain accommodative policy but now expects inflation won’t reach 2% target before 2024.

Chart source - RBC Investment Strategy Committee, RBC Capital Markets, Global Portfolio Advisory Committee, Bloomberg consensus estimates