An excerpt from Global Inisight Aug 2020 - authored by Kelly Bogdanova and Jim Allworth

Despite strong sentiments across the political spectrum, we argue that the American system includes robust

guardrails that limit the ability of any individual, or political party, to impose sweeping change.

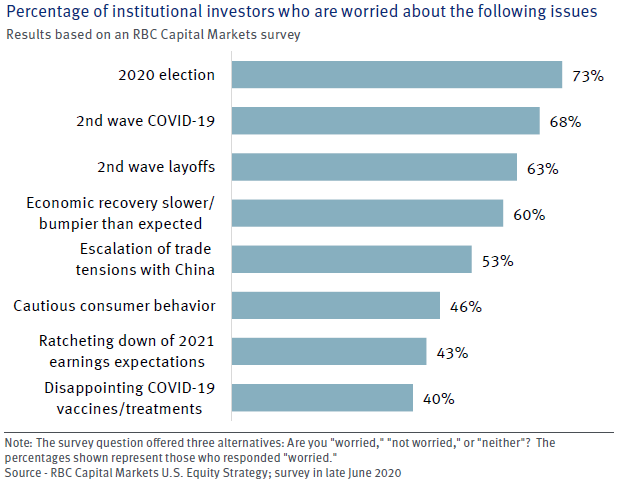

• Institutional investors are more concerned about the 2020 elections than any other issue, according to an RBC Capital Markets' survey.

• Recessions have been unkind to incumbent political parties. Party control of the White House changed in five of the last seven presidential contests that overlapped a recession.

• We think there are three plausible election outcomes for investors to focus on: The status quo with Trump and a divided Congress; Biden and a divided Congress; and a “blue wave” with the Democrats controlling the presidency and both chambers of Congress. These scenarios could impact the economy, markets, industries, and tax structure somewhat differently.

• A blue wave scenario that also includes the removal of the filibuster rule could be the most challenging for the equity market.

• But would it mean gloom and doom? While it could usher in some volatility or even a selloff, we doubt it would be long lasting because the American system’s formal and informal checks and balances act as guardrails, mitigating sweeping policy outcomes.

• An overlooked guardrail is the business lobby. We would not underestimate its power and creativity. We think business interests (which overlap many investor interests) would still have a prominent seat at the table, regardless of the election outcome.

Election angst, and then some

It is safe to say opinions and emotions about the U.S. elections are running hot.

The angst seems to be spilling over into the investment sphere, with people across the political spectrum concerned that various election outcomes could be

detrimental to financial markets—or worse.

U.S. presidential elections have polarized the public for many decades, especially when there are major differences in the candidates’ policy proposals on taxes and other hot-button issues, as in this election cycle. This is nothing new—elections have consequences.

What is new are the stark differences in opinions among investors regarding potential election outcomes, and the greater possibility that emotions could influence or even drive portfolio decisions. Strong sentiments also surrounded the 2016 election, but they seem more pervasive to us this time around.

This article is the second in a series titled, “U.S. election & market matters.” In this edition, we begin to analyze the key policy issues pertinent to financial markets in light of the three most plausible election outcomes. We also address the American system’s important checks and balances as they relate to policies that could impact

the investment landscape.

How unique are the 2020 elections?

This presidential election has some unusual and not-so-unusual features. It comes alongside a recession and pandemic, which are shaping the candidates’ policy proposals.

Presidential contests that overlap recessions are more prevalent than one might think. In the 25 presidential elections in the past 100 years, a recession has reared its head on seven of those occasions, for at least part of the year.

American elections have often been referendums on the economy, and this may be why recessions have been unkind to incumbent political parties. Since 1920, the incumbent party lost the White House in five of the seven instances when a recession was ongoing during the election year, most recently amid the Great

Recession in 2008.

To understand the potential effects of the unusual COVID-19 pandemic, one historical precedent offers the best analogy: the so-called Spanish flu, a global

pandemic that began in early 1918 and lasted into the spring of 1920. It’s difficult to gauge that pandemic’s impact as there were other economic crosscurrents at the time and it overlapped World War I. But it’s worth noting that the U.S. succumbed to a recession toward the tail end of the flu pandemic in January 1920, and the recession lasted into the next year. The incumbent Democratic Party lost the White House in 1920.

None of these data points are enough to base current investment decisions on. They are too few in number to be statistically significant, and each episode had unique contours. But the recession track record is something to keep in mind.

Elections scenarios & key issues that are in play

We think there are three plausible election outcomes for investors to focus on, each of which could impact the economy, markets, industries, and tax structure somewhat differently.

Status quo – Trump and a divided Congress:

President Donald Trump is re-elected, and the balance of power in Congress stays the same with Democrats in control of the House of Representatives and Republicans leading the Senate by a slim margin.

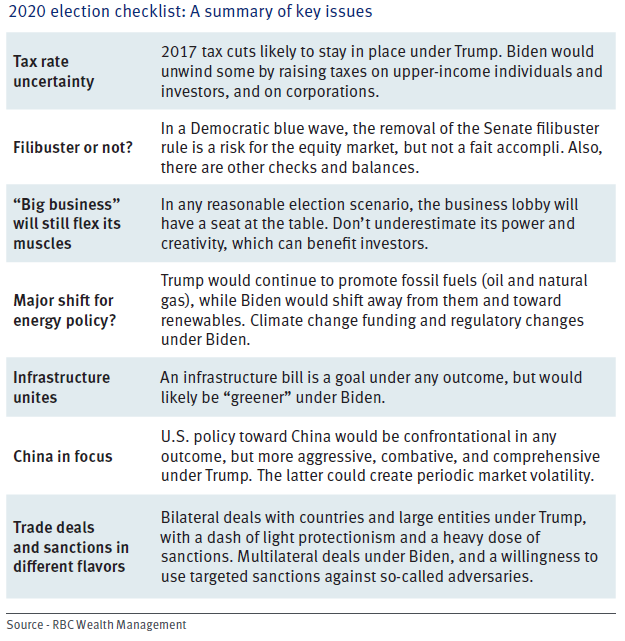

• Key initiatives: Thus far, Trump’s re-election pitch is similar to the one he ran on in 2016 and the policies he has governed on since. He would focus on growing the economy and creating jobs; further deregulating the business landscape; restraining immigration and continuing border wall construction; seeking to pass an infrastructure bill; inking more bilateral rather than multilateral trade deals within an overarching light-protectionist trade policy framework; limiting companies based in rival countries from interacting in key global ndustries through economic sanctions; and challenging China.

• More heat on China: Trump has been more aggressive with China following the bilateral trade deal in late 2019 and since the onset of the COVID-19 pandemic. While some observers see this merely as a convenient election-year tactic, aggressive stances have also been taken recently by the secretary of state, national security advisor, Pentagon eaders, attorney general, FBI director, and some Republican senators. In our view, their collective speeches, policy papers,

and actions go well beyond election year rhetoric. They seem to be laying the foundation for Republican Party policy—at the very least.

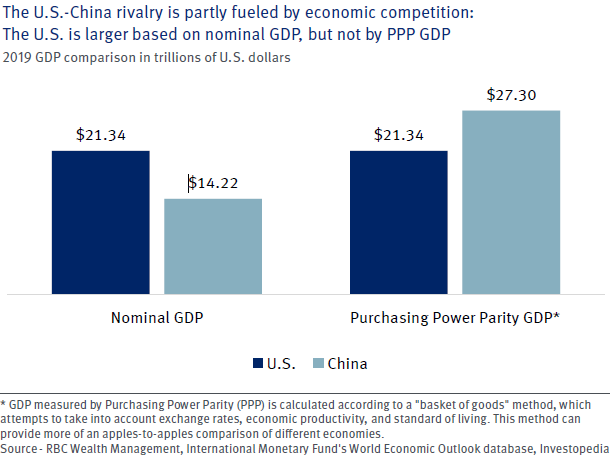

We think a second Trump administration would once again attempt to exert pressure on China through its economic policies and sanctions, as well as by seeking to influence Chinese domestic issues via geopolitical and strategic initiatives. We see no evidence to suggest China would bend to U.S. pressure; in fact, the country’s leadership is already pushing back methodically and calmly. In late July the CEO of the Atlantic Council, a NATO think tank, told CNBC regarding the rivalry, “Well, I think this is going to be decided in decades and not in presidential terms.”

If the U.S.-China confrontations intensify, the conflict could create volatility for equity markets at times. If the showdown between these two economic powerhouses threatens to constrain global commerce on an ongoing basis, a “Cold War 2.0” risk premium may ultimately get factored into equity valuations.

• Tax cuts likely to stay, but … Trump continues to tout the sweeping corporate and individual tax cuts passed in 2017, strongly implying he would not seek to unwind them in a second term. Most of the tax cuts on individuals are scheduled to stay in place through at least 2025, when they begin to sunset by law (new legislation would need to be passed to renew them); the corporate tax cuts are “permanent” unless they are reversed by new legislation. We think keeping tax rates low, especially surrounding the deep COVID-19 recession, would help support U.S. economic growth as well as the equity and corporate bond markets.

On the flip side, however, sky-high annual deficits and rising federal debt as a percentage of GDP likely would be negative over the longer term—even if the economy were to grow somewhat faster with the assistance of lower tax rates than without.

Also, the high deficit and debt remind us of a similar, but less acute episode. After former President Ronald Reagan and Congress cut taxes aggressively in 1981—a modern analog of the Trump tax cuts—major battles ensued on the budget due to surging deficits (to which high spending on defense and social services also contributed). In 1986, in a new tax “reform” bill, Reagan and Congress cut tax rates on individuals and expanded tax credits and exemptions, while at the same time hitting investors with higher capital gains and alternative minimum taxes and eliminating a number of important tax deductions and shelters. The Trump administration has floated the idea of a second round of tax cuts, but so far does not seem to be contemplating a 1986-style about-face that would raise investor taxes to offset the new cuts. We can’t completely rule this out, however, with the deficit and debt so high and the federal government’s mounting obligations (Social Security, Medicare, and Medicaid).

Biden and a divided Congress:

Joe Biden wins the presidency, Democrats maintain control of the House, and the Republicans retain their slim majority in the Senate.

• Key initiatives: Biden would seek to unwind some of the Trump corporate tax cuts by raising the top rate and by putting in place provisions that would require the most profitable companies that pay very little or no tax to pay a minimum tax rate. For individuals, the policy proposal is to increase taxes on upperincome earners and investors, including to limit itemized deductions such as mortgage interest and state and local taxes. Other initiatives are to expand health care coverage and lower costs; address climate change by reducing the use of fossil fuels and increasing the use of clean, renewable energy sources; pass an infrastructure bill with a focus on “sustainable” transportation infrastructure; implement a more active regulatory approach; and expand immigration and reverse some related Trump administration policies. Trade policy would shift back to multilateral rather than bilateral deals; economic sanctions would likely be imposed in response to perceived national security threats; and we expect China would be confronted in a targeted way, including in the technology sphere.

• A shift in direction, with constraints: In this scenario, Biden’s agenda would be constrained by Republican control of the Senate floor and its committees—a powerful tool for the opposition party. Due to the filibuster rule, which effectively requires a supermajority of 60 out of 100 votes to pass legislation, at least some compromise would be needed to pass important bills. In this case, we think Biden would make progress on key aspects of his agenda, but not a lot. There could be some tinkering with the tax code, although we would not expect big changes initially.

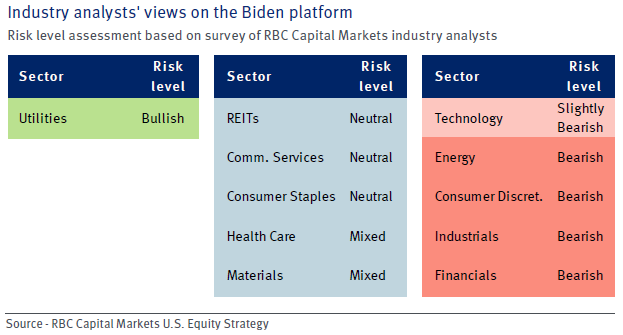

In our view, a Biden presidency combined with a divided Congress would be largely neutral for financial markets. We believe some industries would benefit (renewable energy, utilities, and pockets of health care, for example), while others could face challenges (fossil fuels, financials, aerospace and defense, and other areas of health care). Fiscal stimulus should offset sector headwinds.

Blue wave - Democratic sweep:

Biden wins the presidency, Democrats retain the House, and the Senate flips from Republican to Democratic.

• Controlling the Senate: With the upper house of Congress in Democratic hands, there would be fewer barriers to pass legislation and set the country on a different course. Control of the Senate floor and committees entails great legislative advantages. If the Democratic majority were to retain the long-standing filibuster rule, 60 votes would continue to be required to pass a bill—thus, it would still be necessary to find common ground with at least a small group of Republicans.

• Out with the filibuster? In a blue wave scenario, the elimination of the Senate supermajority filibuster rule becomes a possibility for all votes, or at least for key pieces of legislation. (The filibuster is not necessarily an all or nothing rule—it can be used consistently across all legislation or just on certain bills.) If the filibuster were abolished, only 50 votes (plus the vice president’s tie breaker) would be required to pass legislation.

Senate Democrats would need to make a proactive decision to eliminate the filibuster rule in the face of opposition from even the most moderate Republican senators. To remove it would be a big step given it has been used since 1837 in the upper chamber (much more so in recent decades), and has historically been viewed as a guarantee that major shifts in public policy have at least a modicum of bipartisanship. Such a change could sow discord in the Senate for years to come, and invite retaliation should Republicans regain control of the chamber in the future. For these reasons, eliminating the filibuster is not a fait accompli. But both parties are already using it as a weapon in their campaign rhetoric, and the push for its removal gained traction recently when former President Barack Obama endorsed ending the practice.

Without the filibuster, a blue wave could be more challenging for the equity market as we think it would generate greater concern about tax policy for upperincome earners and investors. It would also likely impact corporate earnings. Based on RBC Capital Markets' polling of its industry analysts and institutional investors, the blue wave/no filibuster scenario is the most bearish for the equity market and select industries.

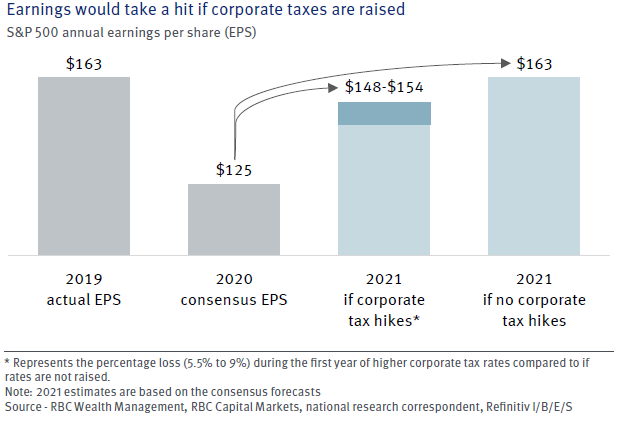

For example, if half of the Trump corporate tax cuts were reversed and the top rate raised—as Biden seeks to do—S&P 500 profits could be about 5.5 to 9.0 percent lower during the first year of implementation, according to estimates from our national research correspondent and RBC Capital Markets. Furthermore, the industries and sectors that would be most at risk of major regulatory and/or legislative changes in a blue wave scenario could face more pressure if the filibuster were removed. All of this could add to market volatility and downside risk.

Checks and balances

Would a blue wave with no filibuster necessarily mean gloom and doom for the U.S. economy and stock market? While it could usher in some volatility or even a selloff, we doubt it would be long lasting for reasons even beyond the fact that high fiscal spending could partly offset some of the potential economic pressure.

Under all three likely party control scenarios, the American system’s formal government checks and balances can act as guardrails. The separation of powers into three co-equal branches (executive, legislative, and judicial) restrains the ability of a particular president or Congress to take the country in a drastically different direction in one fell swoop—regardless of how candidates and political parties promise that they can in nearly every campaign season.

In the past, the checks and balances have worked to varying degrees, depending on the historical circumstances. We acknowledge they are not foolproof; if a Democratic blue wave were accompanied by the removal of the filibuster rule, then the legislative guardrails would be lower. In that case, however, other unofficial checks and balances would still remain that investors should take into account.

A powerful—and often overlooked—guardrail is the collective voice of business interests. We’ve yet to witness a legislative cycle where business groups didn’t achieve at least some of their lobbying objectives, often to the benefit of investors.

In the last few presidential cycles, for example, controversial initiatives such as Trump’s trade deal with China and Obama’s Affordable Care Act were greatly influenced by negotiations with the corporate sector. There were times when both agreements generated enough volatility to test the nerves of investors, but in the end compromises were struck to the satisfaction of multiple parties.

We would not underestimate the power and creativity of the business lobby. Should the Senate remove the filibuster, we think business interests (which overlap many investor interests) would still have a prominent seat at the table.

The Federal Reserve and the natural ebb and flow of the economic cycle are also “checks” on government power, and we think they actually influence financial markets more than the president or Congress. In a previous article, we explained why these forces are so relevant. The re-election or defeat of Donald Trump, and the continuation of the status quo in Congress or its realignment by a blue wave, are outcomes that will have comparatively little impact next to the outsized roles that the Fed and economic cycle play.

Bigger than the Oval Office

We have a hard time believing the slow-moving supertanker that is the U.S. federal government will suddenly start veering like a speedboat following the 2020 elections, regardless of the outcome. The checks and balances embedded in the American system—both formal and informal—mitigate far-reaching, sweeping policy outcomes.

These are among the practical reasons we think the most acute partisan fears about various election outcomes are unlikely to be realized. The U.S. economic system is

bigger than the presidency and those who control the levers of power on Capitol Hill.

There are certainly risks for financial markets associated with the 2020 elections. We think it prudent to remain at least moderately Underweight U.S. equities in portfolios, by positioning holdings somewhat below the long-term strategic allocation.

In this article we have touched on the broad electoral issues that could impact markets. In future editions of our “U.S. election & market matters” series, we will address some of these issues in depth, such as Biden’s tax proposal, both candidates’ trade policies, their economic policy differences, and the risks and opportunities for key sectors and industries.

Authored by Kelly Bogdanova and Jim Allworth