This past weekend, the US and Israel began a full-scale military operation aimed at neutralizing Iran’s nuclear capabilities and, potentially, installing a more Western-aligned regime. As always, our primary lens is how developments like this impact markets and, most importantly, what they mean for our clients’ portfolios.

Below we break down the core market risk we are watching, why history suggests perspective is warranted, and the deliberate steps we took earlier this year to position portfolios defensively.

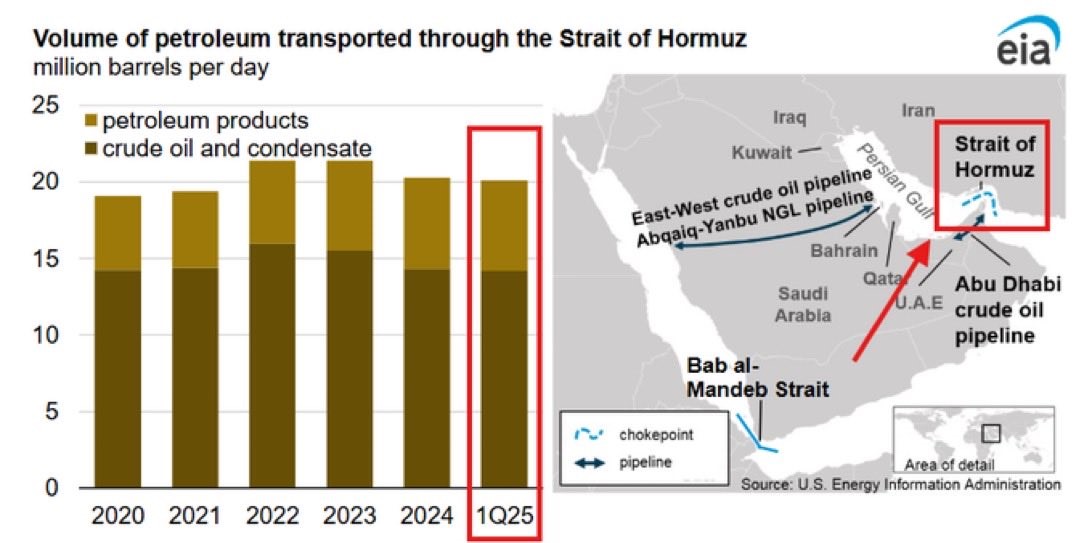

Oil Remains the Primary Market Risk

Over the last forty years, Iran has become increasingly isolated from the global economy. Its trade with the West is minimal, and outside of China and a handful of regional partners, its economic footprint is small. From a purely macro perspective, that limits the direct contagion.

Oil is different. Iran accounts for roughly 4–5% of global oil supply, which is meaningful but not, on its own, systemically destabilizing. The real issue is the Strait of Hormuz. As the graphic below from the US EIA shows, approximately 20 million barrels of oil (~20% of global output) flows through that chokepoint. Any sustained disruption—whether through mining, tanker seizures, or insurance market withdrawal—would have an outsized impact on energy prices.

Because oil is a globally priced, systemically important commodity, large price swings feed directly into:

- Inflation expectations

- Consumer spending

- Central bank policy paths

- Equity multiples

For this reason, the oil price trajectory is the single most important variable we are tracking to assess the wider global market impact of any prolonged Iranian conflict.

Reminder: Stick to the plan

Periods like this test discipline. War introduces uncertainty, and uncertainty creates volatility. We should expect emotional market reactions in the days and weeks ahead.

History provides valuable context here. Major geopolitical and crisis events have repeatedly produced an initial negative market reaction—often sharp—followed by meaningful recovery over the intermediate to longer term. The table below from Carson Research breaks this down nicely.

The central lesson: these episodes, while unsettling, rarely derail well-constructed long-term plans. Avoiding headlines and staying anchored to our disciplined strategy is what has served our clients well through past cycles.

Defensive Moves We Made Early in the Year

Being long-term investors does not mean being passive. As we regularly communicate, the strongest defense against unexpected global events is proactive portfolio positioning, sometimes well before any specific catalyst emerges. That prudence can mean forgoing a portion of short-term upside in exchange for greater resilience.

Despite our generally constructive economic outlook entering 2026, we flagged elevated turbulence risk in our year-ahead commentary (feel free to reach out to view a copy of our presentation). Combined with the very strong performance investors enjoyed over the last few years, we viewed it as an appropriate window to reduce certain exposures and add defensive ballast.

On that note, key adjustments we implemented over the last few months include:

- Increased exposure to oil & energy names (e.g., CNQ, SU, XLE, CCO)

- Added to defense-related companies (e.g., RTX, BBD)

- Increased allocations to precious metals and basic materials (e.g., XGD, XBM)

- Reduced large-cap technology holdings (e.g., MSFT, NOW)

- Trimmed low-yield, high-duration fixed income

- Boosted cash levels and allocation to hedged / absolute return strategies

These changes leave us less reliant on chasing momentum and better equipped to evaluate emerging opportunities as they arise. We have liquidity, we have hedges, and we have exposure to the sectors that historically benefit from energy and defense shocks. That puts us in a position of optionality rather than urgency.

Our Focus Now

Moving forward, you can expect us to:

- Monitor oil markets and Hormuz shipping conditions

- Watch for second-order effects on inflation and rate expectations

- Deploy capital opportunistically when dislocations create value

As always, our job is to protect capital first and compound it over time, regardless of the headline environment. If this latest development has prompted questions about your own portfolio’s positioning—or if you would simply like a fresh review in light of current events—please feel free to reach out.