-

Canadian investors need to be particularly careful in preventing emotions from dictating actions.

-

Successful thinking about tariffs, like every other issue, needs to be systematic and focused on real economic impact.

-

Our proactive approach pays off in times like these. Remaining on the lookout for risks and opportunities will be key in the months ahead.

Mindset is Everything

It’s been 44 days since US President Donald Trump began his second term. It’s admittedly felt a lot longer. Still, one of the themes of this term so far is unpredictability. This is particularly true when it comes to tariffs. Nearly all their “who, what, where, when, and how” elements have been unclear from the beginning, with the situation being fluid, to put it politely. This is partly because the tariffs being discussed are constantly changing. In fact, it’s possible they have changed again by the time this article is published. In any case, their impact is currently being felt in markets, with the S&P 500 and growth-heavy Nasdaq down off their highs by about 6% and 10% respectively.

If you are a Canadian investor, this is probably one of the more concerning bouts of volatility in recent memory. A bit of discomfort can set in any time the market is down. But this time is different. For many, this feels like an unprovoked fight that threatens our way of living. And it’s coming from our greatest ally, no less. This has added a certain amount of anger and shock to the cocktail of emotions in this market downturn, making it feel different from others. We therefore think it’s worth spending a little time talking about investor mindset.

With this in mind, our message to investors is to be extra careful in preventing our emotions from dictating our actions. In times like these, there is a tendency to emphasize the short term; we become hyper-aware of the news and shift our attention to weekly, daily, or even hourly portfolio activity. But this type of focus has little-to-no relationship with our long-term financial goals. Instead, it can cause us to lose sight of the big picture and make hasty changes to our investment plan, all in an effort to re-exert a feeling of control. These changes almost always end up doing more harm than good.

The best antidote to emotional thinking is to force oneself to think longer term. How will the companies (investments) you own be doing in three-to-five years? Are they in industries that are growing? Are they led by people who know what they’re doing and that have demonstrated good judgment in the past? Do they provide something others don’t? Are they in a financial position to ride out a storm and potentially even benefit from it?

It’s telling that five years ago today we would have been right in the middle the COVID market crash that took about 30% off markets. If you had done the above exercise then and stuck with your plan, your portfolio would have easily recouped its losses and provided a fantastic return in the years ahead (the S&P 500 is up ~80% since Jan 2020). Then, as now, the world was a challenging place. But good companies are able to thrive regardless. If you’re one of our clients, you know we spend a lot of time obsessing about the quality of the companies we own and won’t hesitate to act if something doesn’t look right. In short, we are on the lookout on your behalf. Hopefully this gives you enough peace of mind to focus on the big picture.

Thinking Systematically About Tariffs

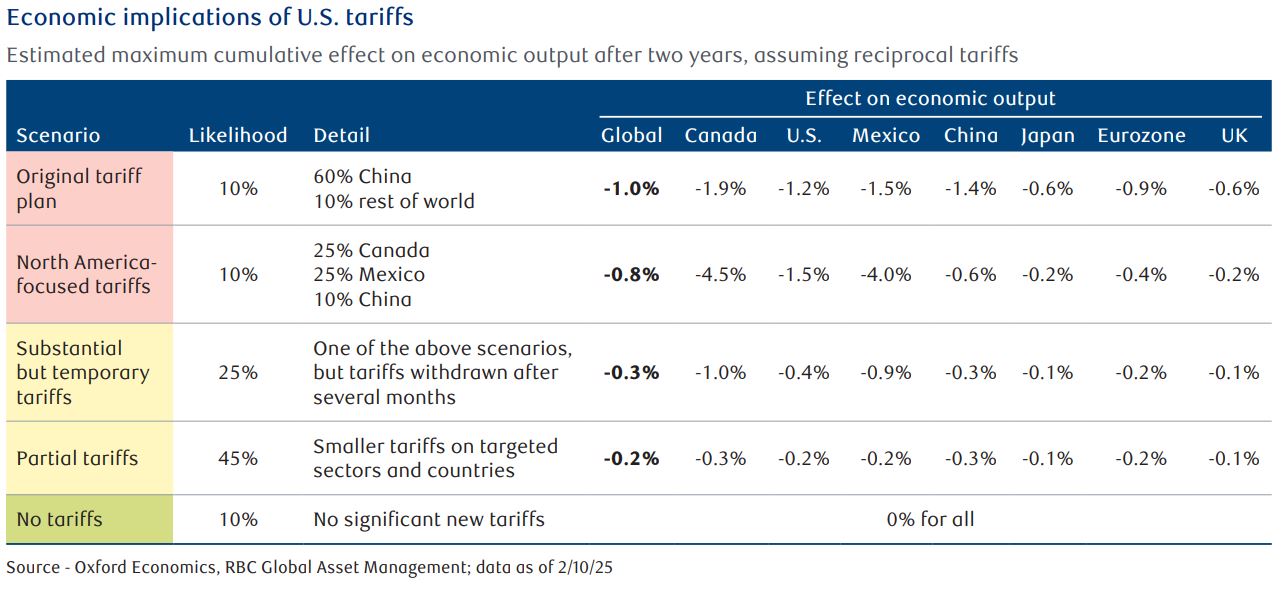

The above notwithstanding, we would be remiss if we didn’t summarize our views on tariffs as they stand today. Our current thinking is based on our assessment of their economic impact. The chart below, put together by our partners at RBC Global Asset Management, presents the best and most clear analysis we have seen. We particularly like it because it builds in uncertainty. The truth is that no one knows what the eventual structure of tariffs will be or how long they will last. The best we can do is think systematically about the outcomes, assign each a probability based on our knowledge today, and derive a sense of what the picture could look like in different scenarios.

Our conclusions can be summarized as follows:

-

Our base case is that the blanket tariffs enacted on March 4th will eventually give way to targeted tariffs on certain sectors. Our reasoning is based on what is best for the US economically, since the former hurt growth more and lead to higher inflation. Fortunately, this will hurt but not disable impacted countries.

-

The longer the uncertainty around tariffs last, the more short-term pain it will cause all those involved, particularly those with smaller economies. Companies are already delaying investment decisions because of a lack of clarity.

-

Most importantly, in all cases we do not see tariffs resulting in a US recession. Therefore, any downturn in this market is likely not the start of a bear market and should be treated as a buying opportunity.

-

A recession is likely in Canada if substantial tariffs stay on for a significant amount of time. A defensive approach here is warranted.

What have we done so far and what’s our plan moving forward?

Despite the fact that the situation is fluid, the above has implications for portfolios that require investors’ attention. Our regular readers know that we emphasize a proactive (rather than reactive) approach to managing risk. To this end, we rebalanced often last year, taking money off winners and stowing them in cash, fixed income, or stocks that had more room to run. This has and will continue to protect us from the worst of the downturn. It has also created a reserve we can tap into to take advantage of market opportunities. So we’re already ahead of the game.

Within stocks, Canada is in an obvious tough position. But this weakness didn’t start with tariffs; it has been in bad shape for a while now. We shifted our holdings to be less domestically oriented some time ago. Further, the Canadian businesses we do own are extremely high quality, pay a substantial dividend, and are well positioned to ride out the storm. By the latter we mean they have strong balance sheets, capable management teams, and are in industries that tend to do well in most economic environments (think Dollarama).

In the US and international markets, we are more interested in playing offense. We have a shopping list of companies that we are looking to buy at the right prices. We are particularly interested in those that are either (a) exposed to the long-term themes that will drive economic growth over the next five years and (b) those that will be able to take market share from weaker competitors if tariffs last longer than expected.

In any case, we remain on the lookout for risks and opportunities. This is imperative in a situation as fluid as this.