The election results surprised us. It wasn’t the fact that Trump won; the polls indicated the candidates were in a virtual tie prior to the vote so we believed either party had a shot. What surprised us was how fast the outcome was determined and the extent to which the Republicans were victorious. The market seemed surprised too. This explains why virtually all assets (stocks, bonds, currencies, etc.) moved significantly after the election as investors sped to factor in a Trump presidency. Thankfully, we had a plan of action in place for the most likely outcomes, including this one. With that said, our focus now is squarely on the implications of a Trump-led government and its impact on our portfolios.

The Trump Presidency Cheat Sheet

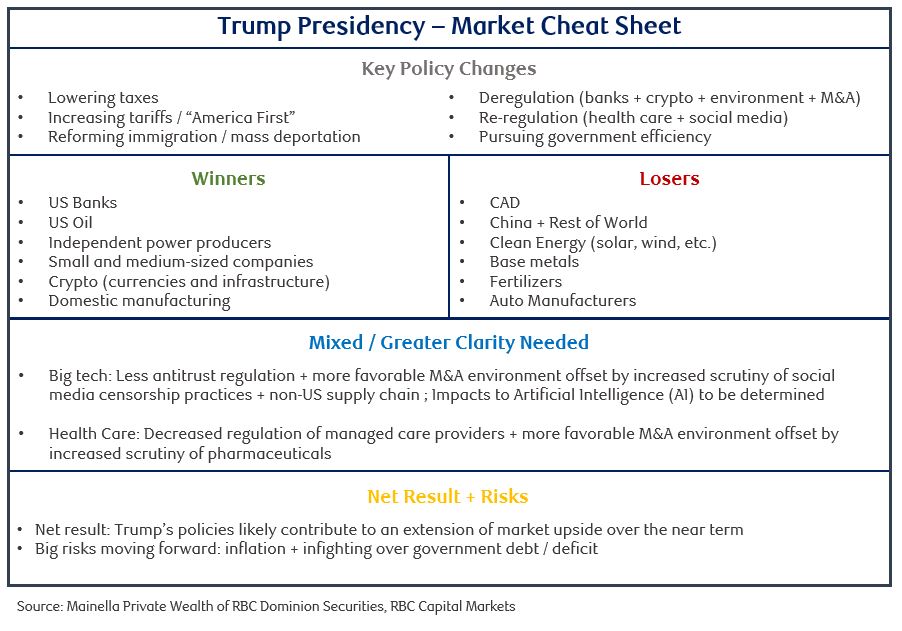

Providing a complete breakdown of the “Trump 2.0” platform would make this newsletter too long for its intended scope. Instead, we thought it would be helpful to summarize the key policy changes he has proposed, their potential winners and losers, and the net results and risks we see moving forward. You can see this in our “Cheat Sheet” below.

At its essence, the Trump platform is good for the US economy and markets in the short term. The generally pro-business policies favor cyclical sectors (i.e. those that go up and down with the economic cycle). This is particularly good for banks, who are likely to see boosted mergers and acquisitions (M&A) revenue in the years ahead. It’s great for small and medium-sized companies as well, as they stand to benefit in an outsized way from the increased economic activity that comes with lower taxes. The “America first” mentality also suits domestic manufacturing well as we’re likely to see more of the onshoring trend that’s taken hold since COVID. All of this will increase the demand for energy, boding well for oil, gas, and electricity production.

In contrast, the likely losers of Trump 2.0 include pretty much everyone other than the US. China, Canada, Europe, Emerging Markets – all countries/blocks will have to find a way to cope with a more inward-focused US economy. Inside the US, green energy and electronic vehicle manufacturers will experience pain as their subsidies and favorable regulatory treatment come under scrutiny. The impact on other notable areas – specifically Big Tech and Big Pharma – is a bit more mixed, though we believe they will fare well regardless.

Not All Good

The above may seem like an unambiguously favorable platform for the US economy. This is not the case. The Trump 2.0 platform has costs that will take time to appreciate. Specifically, it presents two key risks. The first is inflation. The proposed tax cuts are coming at a time when the US economy arguably doesn’t need them. Stimulating demand in this environment is likely going to push prices up. Tariffs, too, are inflationary; if you could produce something more cheaply in the US, you would already be doing so. Slapping tariffs on imports makes things more expensive since you either pay more for what you import anyway or switch to a more expensive domestic producer. Mass deportation is also inflationary since it reduces a cheap source of labour – one that happens to be concentrated in construction, a crucial sector for building out domestic industrial capacity. If inflation does take hold, then any economic/market gains we’ll see in the short term are simply being borrowed from the future and will likely speed up the arrival of the next down cycle, when the Federal Reserve will be forced to step in and hike interest rates to stop prices from climbing. This assumes, of course, that the Fed is left independent (which we hope is the case but is not a given under the Trump administration). The other concern regards the deficit, which will likely rise unless major cost cutting initiatives are put in place. We’re skeptical about the appetite for the latter. We therefore expect the debt/deficit discussion will take center stage in the years ahead, bringing market volatility along with it. In short, we see a positive run for the economy and markets in the short term (6-24 months) but balance this with a sense of caution beyond then.

Making Moves

Considering the net results and risks, we have been active both before and after the election to ensure our clients’ portfolios are positioned for success in a Trump-led environment. Earlier this year, we built up our positioning in small caps, banks, and industrials which all received a boost from the Trump win. After the win, we deployed the bulk of our cash reserves into energy producers and domestic US manufacturers. We also increased our allocation to Canadian-domiciled stocks that do most of their business in the US (ex: Shopify). The results have so far been favorable for our clients, widening our lead over our respective benchmarks. Our clients can expect us to continue to stay vigilant as we work our way through the new policy environment on their behalf.