The Canadian economy is not yet out of the woods, but we think the Bank of Canada is near the end of its rate hike cycle and the pressure on household balance sheets should subside over time. We see opportunities in Energy, while long-term investors can find value in bank stocks. The fixed income market is the most attractive in 16 years, in our view, and this calls for shifting exposure from short-term bonds to those with longer durations.

Canadian equities

Consumer spending shows clear signs of softening.

The Canadian consumer should remain in focus in 2024 as restrictive monetary policy and its impact on consumers finances continue to work their way through the Canadian economy. The idiosyncratic risks of elevated household debt levels, coupled with the housing sector’s outsized impact on the economy, have translated into a weaker economic environment in Canada relative to its less-levered neighbour to the south. Household budgets are beginning to feel the pinch of higher interest rates with consumer spending showing clear signs of softening. According to RBC Economics, Canadians are spending nearly 10% more on essential items than they were just one year ago. At the same time, the surge in discretionary spending has slowed with a downtrend in restaurant and travel spending. After a strong start to 2023, the Canadian housing market also appears to be stagnating, with the psychological impact of a lower net worth adding further pressure on Canadian households.

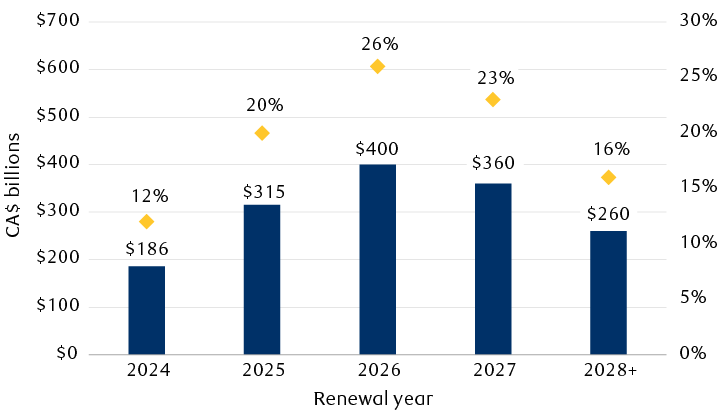

What is the silver lining? Evidence continues to build that inflation risks are easing as the economic backdrop softens. RBC Economics does not expect additional interest rate hikes from the Bank of Canada if that continues. This would bring a sigh of relief to Canadians with variable rate mortgages, as each rate hike has resulted in either higher payments or a lower proportion of principal paid. For those renewing their mortgages over the next few years, the eventual easing of monetary policy (i.e., lower interest rates) is of greater importance. RBC Capital Markets estimates that 20%, 26%, and 23% of Canadian-bank-originated residential mortgages will be up for renewal in 2025, 2026, and 2027, respectively.

Canadian mortgage renewals expected to rise substantially through 2026

Estimated residential mortgages up for renewal at Canadian chartered banks

The column chart shows the value (in Canadian dollars) of Canadian residential mortgages up for renewal, as well as the percentage of all mortgages up for renewal, each year from 2024 through 2027, and in 2028 and beyond. In 2024, $186 billion, or 12% of the total number of mortgages; in 2025, $315 billion, or 20% of the total; in 2026, $400 billion, or 26% of the total; in 2027, $360 billion, or 23% of the total; in 2028 and beyond, $260 billion, or 16% of the total.

Note: Distributions do not total 100% as renewals for the remainder of FY2023 are not shown.

Source - RBC Capital Markets, RBC Wealth Management, company reports; data as of 10/31/23

The trajectory of interest rates and the ultimate impact on the Canadian consumer will have clear implications for the Canadian banks, in our opinion. Several Canadian banks recently cited the risk of “higher for longer” rates when provisioning for future credit losses. Bank valuations continue to reflect the uncertain environment with the group trading at a steep discount relative to its long-term average and close to trough-like levels previously seen during the Global Financial Crisis and the early days of the pandemic. While it is hard to identify a catalyst for why valuations should improve at this stage of the credit cycle, we believe income-oriented investors with a long-term view can find opportunities in Canadian bank stocks.

We expect Energy sector performance will be largely influenced by commodity prices. We would highlight energy investors’ ability to reap meaningful cash returns via buybacks and dividends in a constructive economic environment. But, even if the challenging economic backdrop persists, Canadian energy companies are now better equipped to navigate this due to their fortified balance sheets and reasonable capex needs. We continue to suggest owning the best-of-breed Canadian energy producers in 2024, particularly for those investors with an income focus.

On balance, we believe the Canadian equity market should be supported in 2024 by its discounted valuation relative to history, while its exposure to the resource complex provides a hedge of sorts if inflation pressures persist.

Canadian fixed income

Interest rate risks are becoming more two-sided.

The sharp increase in bond yields seen throughout most of 2023 is beginning to abate as the Bank of Canada (BoC) appears more firmly positioned on the sidelines, opting to put further policy rate increases on hold while it assesses the cumulative economic impact of the string of rate hikes it has already delivered. Despite inflation remaining much higher than the BoC would prefer, economic momentum is softening, as evidenced by decelerating month-over-month GDP growth numbers; this relieves some of the pressure on the central bank to continue hiking at the same aggressive pace. That being said, the BoC remains on guard against upside inflation data surprises, leaving the door open for additional hikes if necessary. With the BoC likely approaching the end of its policy-tightening regime, and monetary policy strongly dependent on month-over-month economic data, we view the risks of interest rates moving in only the upwards direction as diminishing. In other words, we see the interest rate outlook as becoming more two-sided, strengthening the case for extending duration within our fixed-income portfolios.

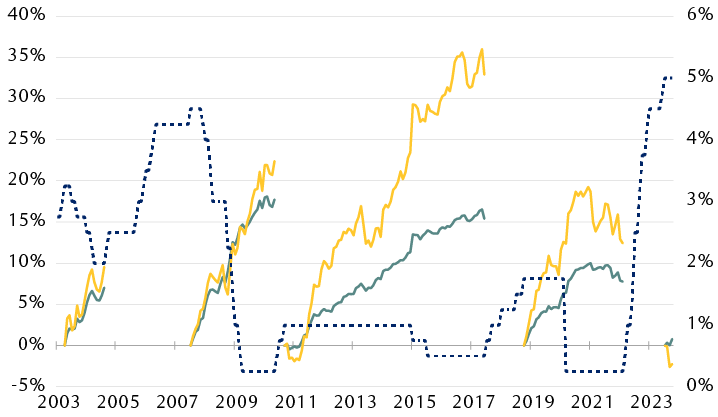

Looking back at the history of recent monetary policy cycles reveals that adding duration to portfolios following the last BoC rate hike has led to higher total returns relative to short-duration strategies. For example, as the chart shows, the Bloomberg Canada Aggregate 5–10 Year Index has consistently outperformed the shorter-duration 1–5 Year Index following the final BoC rate hike in a cycle.

Longer-duration bonds tend to outperform following policy rate peaks

Total returns after the Bank of Canada’s final interest rate increase in hiking cycles

The line chart shows how different bond maturities have performed following the end of previous cycles of interest rate increases by the Bank of Canada. From April 2003 to August 2004, from August 2007 to May 2010, from September 2010 to June 2017, from November 2018 to March 2022, and from August 2023 through October 2023. In most cases, longer-dated bonds (those with maturities of five to 10 years) have outperformed short-dated bonds (maturities of one to five years).

Source - RBC Dominion Securities, Bloomberg; data through 10/31/23

After spending three years sheltering in short-duration securities while the BoC rolled out nearly 500 basis points worth of interest rate increases, it is now reasonable, in our view, to consider lengthening duration in portfolios. However, despite the more attractive risk-reward profile of duration at this time, we think it is prudent for investors to lean in cautiously and calibrate their exposure to their rate volatility tolerances. This view on duration can be expressed in portfolios while still maintaining a degree of duration diversification by extending maturities through laddering, exposing the portfolio to a higher degree of rate sensitivity while minimizing return volatility, which should lead to a smoother path of returns.

In today’s rising-rate environment, companies are being forced to pay up to issue new debt and refinance old debt, in many cases at costs that are three times higher than 2020 levels. Yet despite tighter conditions for corporations and a more difficult operating environment, the extra yield compensation demanded by investors for the risk of default on corporate bonds remains range-bound, and in our view is far from levels that would suggest economic trouble ahead.

On the other hand, we continue to expect some level of corporate pain, as well as some degree of negative credit repricing over the near term. We have therefore reduced our preference for corporate credit, while maintaining a bias towards higher quality (i.e., an investment-grade rating) within our corporate bond allocations. Nonetheless, we see bond yields as broadly attractive from a historical perspective, with higher starting yields providing some cushion against further rate increases and/or credit spread widening.

Regardless of one’s approach to bond investing—buying and holding to maturity, or trading in and out opportunistically—higher base rates make bond investing more attractive today than during any other period over the last sixteen years, in our view. We believe the past three years of surging yields, though painful for existing bond holdings, have increased the likelihood of achieving equity-like returns via credit instruments going forward.

View the full Global Insight 2024 Outlook here