However, medium-term challenges still persist as the industry navigates significant capital costs and construction difficulties. We highlight some opportunities for exposure in this space.

Change is afoot in the nuclear energy sector. After decades of underinvestment going back to the 1980s, nuclear energy is garnering increased attention from investors and the public alike. Sustainability-focused investment funds are starting to allocate capital towards nuclear. While public perception has historically been influenced by past accidents like Chernobyl and Fukushima, there is a gradual thawing in attitudes as the industry addresses safety concerns and emphasizes sustainable development.

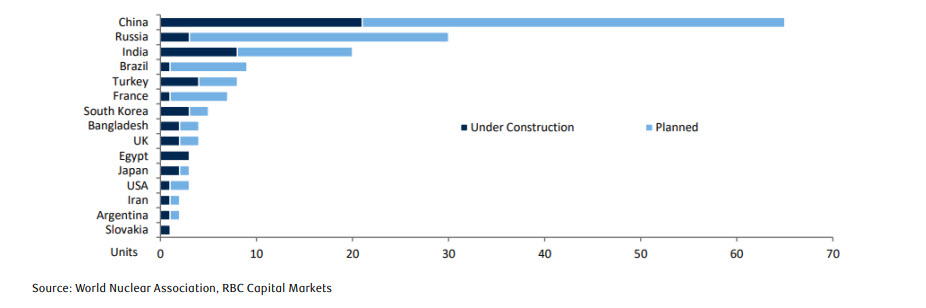

Nuclear power is the use of sustained nuclear fission to generate heat and electricity and is well-positioned to grow, supported by clean energy demands. Around the world, 60 new reactors are being built with 100 more planned. As countries navigate a challenging energy transition and rising geopolitical tensions, nuclear stands out as a source of reliable, low-carbon baseload power. The technology has been advancing, significantly improving safety and minimizing waste. All this is leading to positive change and a potential rebirth of the sector.

Nuclear power plants under construction or planned as of September 2023 – more than half are in China and Russia

The need to decarbonize

Nuclear energy—like solar, wind, geothermal and hydro—generates low direct carbon emissions. With the urgent need to achieve global net zero targets, policymakers are embracing nuclear as a complement to renewables and abated natural gas-fired power plants. The International Energy Agency (IEA) suggests that nuclear power output would need to double by 2050 to achieve net zero goals.1 Renewables alone may not get us there in a timely and cost-efficient manner, despite their lofty growth expectations over the coming decades.

From a lifecycle emissions perspective, i.e., taking into account indirect emissions associated with plant construction and disposal, nuclear compares well with other sources. This is because nuclear requires less construction material, has a longer operational lifespan (lasting 40–100 years while solar panels and wind farms are replaced every 20–30 years), and occupies less land (solar plants and wind farms require 75x and 360x more land to produce the same amount of electricity, respectively).2

Delivering to net zero goals will be harder and more expensive without nuclear. The IEA notes that without nuclear, there will be a need for $500B more investment and customer electricity bills will rise by $20B/year to 2050.3 Clearly, a balanced mix of low-emission energies that includes nuclear power will be needed to achieve climate targets.

Nuclear among lowest emissions energy available

Low-cost alternative

Nuclear’s reliability as a baseload power makes it a useful energy source. Nuclear plants generate power 93% of the time, whereas intermittent renewable resources like wind and solar generate power 35% and 25% of the time, respectively.4 Not only is extra capacity needed for renewables, they also need a backup source or batteries to store energy. This raises the cost and emissions profiles of these sources.

While industry research suggests nuclear can be cost-competitive when considering total system costs, this differs from practice in many cases. Nuclear power projects have frequently experienced substantial cost overruns and delays during construction, causing actual costs of nuclear electricity to greatly exceed initial estimates. However, there are arguments that nuclear projects may be better positioned for success moving forward. New plant designs using modular construction techniques have the potential to lower complexity and risks, while technological know-how and experience will bring efficiencies. Additionally, governments can help reduce costs by providing long-term commitments, financing and regulatory clarity in the licensing and construction processes. One of the most straightforward and inexpensive ways to increase nuclear capacity is through the extension of existing nuclear plants. The IEA noted that reactors designed for 40-year lifespans can be extended by 20–40 years. This offers countries the opportunity to retain the economic benefits of carbon-free baseload power at low marginal costs and with lower construction costs/risks.5 This also makes nuclear energy extensions competitive with solar and wind in many regions.

Government and regulatory momentum

In the wake of the Russia/Ukraine War and ensuing surge in energy prices, there has been a shift in policy for nuclear to meet energy security and independence. Governments are rethinking the value of having a diverse mix of energy sources and suppliers, and having a portfolio that can provide short term flexibility and adequate capacity during high demand periods.5

Recent initiatives by governments worldwide highlight both their willingness to de-risk nuclear projects, and the strategic importance of the technology to their net zero goals.5 For example, in the U.S., the Inflation Reduction Act included a tax credit for nuclear while the CHIPS Act supports the development of advanced reactors.6 Canada recently committed to tripling nuclear energy production capacity by 2050.7

Nuclear energy decisions extend beyond economics to matters such as national resource strategy, non-proliferation, and geopolitical relationships. Among Western nations, collaboration on nuclear has supported cooperation among governments for technology transfers and economic integration which can help broader political alignment. Russia and China have been more active in exporting nuclear tech; their dominance in the sector has also brought integration and political cooperation.5

Public and investor acceptance

Perceptions of nuclear has been tainted by past nuclear plant accidents, such as Three Mile Island (U.S., 1979), Chernobyl (Ukraine, 1986) and Fukushima (Japan, 2011), as well as the use of the technology to create nuclear weapons. However, there has been evidence of increasing acceptance amongst the public and politicians on both sides of the aisle.

RBC Capital Markets believes the industry and governments have done a decent job of informing (and perhaps convincing) the public of the benefits of nuclear technology. Still, a well-informed public need to be convinced that the benefits outweigh the risks, centered around operational safety, management of spent nuclear fuel, and the prevention of weapons proliferation. Public opinion should continue to inflect positively as the industry builds a record of safety, reliability, and environmental sustainability.5

The reality is that major reactor accidents are rare, and nuclear has a relatively safe record versus many electricity production technologies. Living next to a nuclear power plant for a year gives less radiation than a dentist’s X-ray. And all the spent fuel waste produced by the U.S. over the last 60 years could fit on a football field at a depth of 10 meters, to say nothing of additional recycling opportunities.5 As the public better understands the facts, interest in this space should continue to rise.

Headwinds still remain

One of the biggest impediments to nuclear development has been construction difficulty—many global projects have been overbudget and delayed. Such pitfalls add to the overall cost of nuclear energy, hindering adoption and investor perception. Nuclear projects can take close to a decade to complete which adds to complexity and risk. Comparatively, wind and solar projects have much better track records and are thus less risky for investors.

That said, there are reasons to believe the cost issue can be overcome. Smaller and more modular designs allow for easier transportation and lower startup costs. There is room for larger reactor designs to reduce complexity and implement automation. Some projects completed in China took as little as five years, pushing the envelope on construction.5 Extensions, as discussed earlier, are another way to reduce costs. These factors should motivate more development to move forward.

Another deterrent is regulation. Given the safety risks involved with nuclear energy, it makes sense that regulatory rules are strict. However, the rules are also constantly changing, including during the licensing and construction period which also happens to be long. It will be incumbent upon governments to enact a robust and stable framework, all the while prioritizing safety.5

As attractive as nuclear appears to us today, there are many energy industry participants that see any increase in nuclear energy as a threat to their business. Particularly if their slice of the energy transition pie becomes smaller. Amid affordability concerns, capital scarcity, and rising costs of capital, investors and governments may simply direct incremental investment dollars to the path of least resistance (wind, solar, gas) and forego the longer term merits of nuclear.5

As investors, we must weigh both pros and cons when accessing the viability for nuclear.

Opportunity for exposure

In North America, the primary ways to gain investment exposure to nuclear is through the Utilities, Industrials, and Materials sectors.

Utilities and independent power producers have an appetite to invest in nuclear power plants, from pre-construction to operational, as long as the risk profiles of the projects are sufficiently attractive. That includes construction costs, revenue certainty, fuel supply, government policy and regulatory frameworks, and decommissioning/waste management.

Industrials companies are involved across the entire value chain to provide the necessary service/support to existing power stations. That said, the underinvestment from past decades have resulted in challenges in attracting new talent to the industry. Expect stronger project management, additional recruitment, and training of specialized labour to feature prominently going forward.

Uranium mining will be critically important in the future growth of the nuclear industry as the key fuel component for reactors, along with the processing required to turn uranium into nuclear fuel (conversion, enrichment, and fuel fabrication). RBC Capital Markets sees the uranium market in a moderate deficit through the 2020s before entering a potentially significant deficit by the 2030s. Growth will be driven by utilities moving away from relying on Russia, and the buildout of Western enrichment capacity. Uranium resources are not scarce, just undeveloped—expect utility customers to help fund production through long-term contracts.

Reach out to your RBC advisor to learn more about specific nuclear investment opportunities in your region.

- IEA, Nuclear Power report, July 2023.

- BofA Global Research, The RIC Report, The nuclear necessity, May 2023.

- IEA, Nuclear Power report, July 2023.

- BofA Global Research, The RIC Report, The nuclear necessity, May 2023.

- RBC Equity Research, RBC Imagine, Climate of change for nuclear energy, November 2023.

- https://www.rbcinsight.com/wm/Share/ResearchViewer/?SSS_C3D663894D10AA5677300C2DFAEBDE0E

- https://natural-resources.canada.ca/energy/resources/international-energy-cooperation/cop28-declaration-triple-nuclear-energy-2023/25591

Due diligence processes do not assure a profit or protect against loss. Like any type of investing, environmental, social and governance (ESG) and responsible investing involves risks, including possible loss of principal. Past performance is no guarantee of future results. This material has been prepared without regard to the individual financial circumstances, investment objectives, and ESG criteria or other personal preferences of persons who receive it. It is not possible to invest directly in an index. Nothing in this communication constitutes legal, accounting or tax advice or individually tailored investment advice. All decisions regarding the tax or legal implications of your investments should be made in connection with your independent tax or legal advisor.

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that action is taken on the latest available information. The information contained herein has been obtained from sources believed to be reliable at the time obtained. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. To the full extent permitted by law, neither RBC DS nor any of its affiliates, nor any other person, accepts any liability whatsoever for any direct, indirect or consequential loss arising from, any use of this report or the information contained herein. No matter contained in this document may be reproduced or copied by any means without the prior written consent of RBC DS in each instance. RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / TM Trademark(s) of Royal Bank of Canada. Used under licence. © 2024 RBC Dominion Securities Inc. All rights reserved. 24_90083_2224