Key points

- Fossil fuels were given a new lease on life as European and Asian governments scrambled to ensure energy supplies through the 2022–23 winter heating season.

- Yet as governments worldwide moved to combine their environmental agendas with energy security policies, the green transition gained new impetus.

- While most governments have upped their targets for renewable energy, serious challenges remain, such as access to critical minerals, antiquated grids, and higher borrowing costs.

- The increased focus on energy security will see some companies emerge in advantageous positions, but given the challenges ahead, investors should be discerning.

Is the global energy transition powering down? Dwelling on just the headlines, it’s easy to jump to the conclusion that looming deglobalization is imperiling the clean energy drive. After all, since Russia invaded Ukraine—a symptom of deglobalization—fossil fuel production has spiked.

Yet we believe this masks a more significant underlying trend. Although fossil fuel use has been reinvigorated, most nations are also turbocharging the rollout of clean energy as governments are merging environmental agendas with energy security policies.

We delve into the extent of the renewed enthusiasm for green technologies and assess the challenges that threaten their deployment and the achievement of net-zero emissions by 2050. We suggest how investors should position portfolios to tap into industries that we see as likely to benefit from the emphasis on clean energy.

A boost to fossil fuels

Russia’s invasion of Ukraine marked the onset of an era of renewed popularity for fossil fuels, with oil and coal in particular enjoying a new lease on life. With Russian energy supplies at risk, and European and Asian governments scrambling to ensure energy supplies through the 2022–23 winter heating season, oil drilling increased in the U.S., the UK, the Persian Gulf, and, in particular, Latin America. Global production rose by some 1.7 million barrels per day, according to the International Energy Agency (IEA). This intergovernmental organization expects global production to expand by close to six million barrels per day over the next five years.

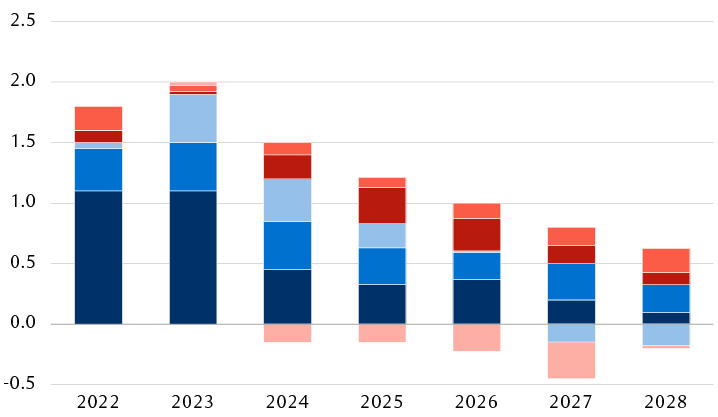

Oil supply increases to peak in 2023 and rise at a slower pace thereafter

Global oil supply forecast, 2022–2028 year-over-year change (million barrels/day)

Bar chart showing the increase in global oil supplies on a million-barrels-per-day basis for the period of 2022 through 2028 and breaks down the various regional sources for the increase in supply. Globally, 2023 marks the peak of the increase in production—at two million barrels per day. From 2024 and forward the increase in daily production diminishes annually to 0.6 million barrels per day in 2028. The United States was the source of the largest daily increases in 2022 and 2023. For 2024, the chart shows that non-OPEC countries, in particular Latin America, will be the key contributors. OPEC+ is expected to contribute less than a quarter of the overall increase in supply until 2028, when it is anticipated to contribute more than half of the additional supply.

Note: Assumes Iran and Russia remain under Western sanctions. OPEC comprises 13 oil-exporting countries: Algeria, Angola, Congo, Equatorial Guinea, Gabon, Iran, Iraq, Kuwait, Libya, Nigeria, Saudi Arabia, United Arab Emirates, and Venezuela. OPEC+ comprises 23 countries including the OPEC members as well as Russia and other major producers such as Azerbaijan, Kazakhstan, Mexico, and Oman. The U.S. is not a member of OPEC.

Source - International Energy Agency, "Oil 2023"

Coal has also experienced a revival. Coal-fired power plants in Europe reopened or were granted life extensions in response to Russia shutting off its gas supplies to the continent. This new appetite was a sharp reversal for coal, which had been in decline since 2014. In fact, the IEA estimates that world coal output reached an all-time high in 2022, surpassing eight billion tonnes for the first time.

This apparent new love affair with fossil fuels didn’t stop at production. Many governments in Europe went as far as subsidizing the consumption of dirty fuels to shield their populations from crippling increases in energy costs, an ironic twist to existing policies that encourage the use of green energy.

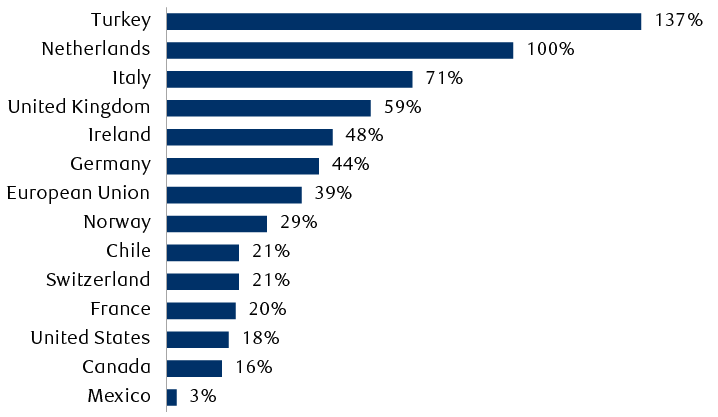

The extent of energy price inflation has varied by country, depending on several factors such as the fuel mix, taxation, and energy bill support strategies. Turkey and Europe have suffered the worst pain as a quarter of households lived in energy poverty (i.e., unable to afford essential energy services) at the peak of the energy crisis, according to the IEA. North America, meanwhile, has not been entirely spared from energy price inflation.

Energy price inflation was highest in Europe and Turkey, but North America was not spared

2022 year-over-year change in energy prices for select countries

Bar chart showing the year-over-year increase in energy prices for select countries. Most affected was Turkey, where energy prices spiked 137%. Energy prices jumped 59% in the UK and 39% in the EU. The increases were more muted in North America, though prices were still up an uncomfortable 18% and 16% in the U.S. and Canada, respectively. The following countries were also shown in the chart: Netherlands, 100%; Italy, 71%; Ireland, 48%; Germany, 44%; Norway, 29%; Chile and Switzerland, 21%; France, 20% and Mexico, 3%.

Source - International Energy Agency, "Energy Efficiency 2022"; data as of October 2022

The real big story: Green energy transition

Yet higher fossil fuel production and consumption mask a much bigger story: the new impetus for the renewable energy transition as governments combine their environmental agendas with energy security policies that have taken on fresh urgency. As such, renewable power can augment energy self-reliance as these energy sources are mostly generated domestically.

Conveniently for governments fostering the green transition, the economics of renewables have improved. New solar plants and wind farms are now more cost-effective to build than fossil fuel-fired plants, even when factoring in the rising raw material and borrowing costs brought on by the Russia-Ukraine war.

Governments are also attracted to the job creation potential of renewable energy projects. In March 2022, a World Economic Forum study projected that the green transition will create 10.3 million net new jobs globally by 2030, with the largest gains in electrical efficiency, power generation, and the automotive sector.

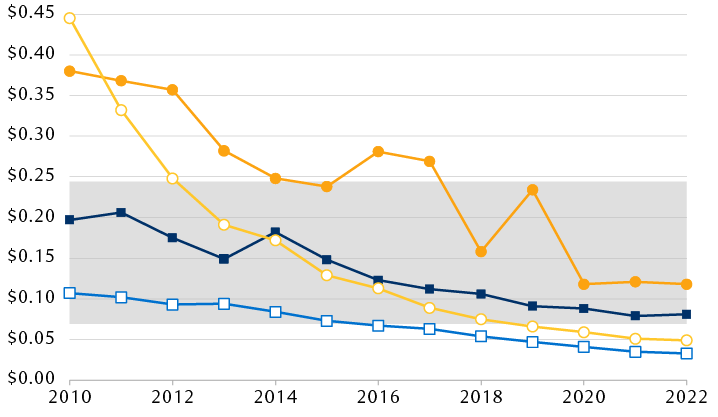

Solar photovoltaic and onshore wind are more cost-effective than fossil fuel

Global weighted average levelized cost of electricity (LCOE) by production technology (2022 dollars/kilowatt-hour)

Line chart showing the progression of the levelized cost of energy for various renewable technologies and the price range for fossil fuels from 2010 to 2021. Since 2010, the levelized costs for offshore and onshore wind power as well as solar and concentrated solar power have declined markedly. As of 2020, all are below the high end of the price range for fossil fuels. The levelized costs of solar photovoltaic and onshore wind are also below the lower end of the fossil fuel price range.

Note: The levelized cost of energy estimates the overall cost of an energy system against the amount of energy it will provide to end up with a cost per unit of energy produced.

Source - International Renewable Energy Agency, "Renewable Power Generation Costs in 2022"

Bankrolling the clean energy rollout

In the wake of the Russia-Ukraine war, most governments have raised their targets for renewable energy generation and announced substantial fiscal support to achieve them.

All in all, the IEA’s current estimate of global renewable energy capacity is 30 percent higher than prior to the war. It expects this capacity to rise almost 75 percent, or by 2,400 gigawatts (GW), between 2022 and 2027—an amount equivalent to China’s current installed capacity.

In the U.S., the Inflation Reduction Act (IRA), signed into law by President Joe Biden in August 2022, provides over $350 billion of subsidies for green technology, which should result in a tripling of U.S. clean energy production, according to S&P Global Commodity Insights. By 2030, 40 percent of the country’s energy could come from renewable sources, or close to double today’s level.

Meanwhile, the European Commission has earmarked €250 billion for clean tech companies via its RePowerEU plan. It now targets doubling the bloc’s installed solar capacity by 2025, five years ahead of the previous deadline.

In 2021, in its 14th Five-Year Plan, China announced for the first time an ambitious goal of generating one-third of its power from renewables by 2025.

The UK, the second-largest offshore wind market worldwide, upped the pace of deployment of this technology, aiming for installed capacity to reach 50 GW by 2030 versus the previous commitment of 40 GW, among other measures encouraging renewables.

Indications of the vitality of the clean energy transition were clearly visible in 2022, including:

- Global Investments in wind and solar assets grew to $490 billion over the year, exceeding outlays for new and existing oil and gas wells for the first time, according to Rystad Energy, an international energy consultancy based in Norway.

- According to IEA estimates, energy efficiency-related investments globally exceeded $550 billion in 2022, up 16 percent over the prior year, with electric vehicles (EVs), building insulation, and heat pumps the key priorities, as consumers faced the worst energy crisis since the 1970s.

- Global EV sales were just shy of 11 million in 2022, up more than 45 percent year over year. Thanks to subsidies and phase-out targets, RBC Capital Markets, LLC’s Senior Global Autos and Auto Parts Analyst Tom Narayan expects global EV sales of some 14 million units in 2023, or close to 20 percent of all cars sold worldwide—a stark step up from a mere 2.7 percent in 2019.

Bottlenecks and higher costs

Despite these renewed commitments, the green energy transition still faces serious challenges which threaten the ambition of achieving net zero by 2050.

One of the most pressing issues is squeezed supply chains. As demand for green products accelerates, so does demand for critical minerals. Increased expenditures on military hardware, particularly from the U.S., EU, and China, exacerbate these issues as these raw materials are crucial to manufacturing and maintaining weapons systems and equipment. Today, for the first time in decades, those three regions, which together represent close to half of global GDP, are all vying for the same limited supplies of resources.

Suppliers of critical minerals and components are struggling to keep up. Investment has been insufficient to meet this surge in demand, while scaling up mining and processing is an expensive and time-consuming process as it takes 10 years on average for a mine to come on stream.

Geopolitical tensions are also rippling across supply chains. China, which dominates the supply chains for most of the metals and minerals required for the energy transition, recently imposed an export ban on germanium and gallium. These two niche metals are used to manufacture electronics and green technologies, and the restrictions are a retaliation to the West’s embargoes on software and chipmaking equipment. Given the risk of further escalation, such tit-for-tat salvos are a wrinkle to keep an eye on.

In an attempt to build more resilient supply chains, the corporate sector is innovating. For instance, EV manufacturers are increasingly turning to joint development agreements. Tesla is now negotiating supply contracts directly with the mines, and General Motors plans to invest $650 million in mining company Lithium Americas to develop a mine in Nevada.

Such collaborations can provide automakers with more control over the supplies and costs of the EV value chain. Vertical integration is becoming increasingly important to car manufacturers as they look to lock in supplies of key battery raw materials at cheaper prices. We think this strategy will become more common in the coming years and may spread to other industries.

Another thorny problem for countries is that antiquated power grids are struggling to keep up with the growing appetite for clean energy. Grids all over the world need to be modernized and enlarged to accommodate renewable energy sources. Still, some renewable generation and storage projects face lengthy delays. For example, it could be a couple of years before projects in some U.S. states are able to connect to the grid, with delays in the UK of up to 15 years. BloombergNEF, a commodity research provider, calculates that 80 million kilometers of new grid is needed by 2050, an amount equal to today’s existing global grid.

Expanding and modernizing the grid has not been much of a priority for governments so far, but it’s dawning on them that the lack of grid investment could put renewable targets in jeopardy. Locating transmission lines alongside highways, railroads, or pipelines, where the granting of planning permission is more likely, could be a way to accelerate the process.

Finally, higher costs are another headwind to the green energy transition. The COVID-19 pandemic and other supply chain issues have made many raw materials, such as aluminum, copper, and steel, more expensive. Prices of many inputs have been dropping, but rising interest rates over the past 18 months have driven up the cost of financing projects, a particularly acute problem for solar and wind farms as they require more upfront capital than traditional power plants. Meanwhile, soaring staffing costs are an additional headache.

In extreme cases, spiraling costs are taking their toll and some projects are being abandoned. Recently, Swedish energy giant Vattenfall suspended work on a 1.4 GW offshore wind farm in the UK after a 40 percent increase in costs. The company won a UK government contract to build 140 turbines to provide energy to 1.5 million homes with low locked-in electricity prices. But following the sharp rise in costs, Vattenfall was unsuccessful in obtaining tax breaks from the government and subsequently halted the project; negotiations are ongoing.

Higher borrowing costs are also affecting consumer demand in the U.S. despite growing concerns over the reliability of the power grid, given struggles to cope with extreme heat waves. This slump in demand led many home solar and backup-power companies in the U.S. to recently cut their sales guidance for 2023.

Thinking outside the box

When considering how to invest in this theme, renewable energy equipment manufacturers come to mind. But given the headwinds they face, as well as fiercer competition that could arise from generous subsidies attracting new players, we believe investors would be better served by seeking a broader opportunity set, including:

- Renewable energy operators, such as large utilities

- Industrial companies that focus on improving energy efficiency in buildings or providing electrification of industrial processes

- Semiconductor companies and other parts suppliers for the EV industry

- Industrial gases companies that provide a range of low-carbon solutions to support the decarbonization of industrial assets and processes

- Select miners of critical minerals and mining equipment providers

Timing and stock selection are key, however, in our view. The stock prices of companies in most of these sectors are highly cyclical and could be subject to volatility should U.S. recession concerns heighten.

Illuminating the renewable energy transition opportunity

As nations’ energy security policies converge with their environmental agendas, the energy transition has been given a new impetus. Policymakers are setting more ambitious targets for green technologies and injecting ample financial support.

Yet the green transition still faces serious challenges. The supply of critical minerals, particularly copper, may well prove to be the barometer of how rapidly the energy transition occurs. Antiquated grids and higher borrowing costs amplify the challenges. The deadline for achieving net-zero emissions by 2050 may wind up being pushed somewhat further out, giving fossil fuels some additional respite.

Nonetheless, the increased focus on energy security and the clean energy transition will see some companies emerge in advantageous positions, but given the challenges ahead, we think investors will need to be selective.