When I started writing this, I did not think it would be as wordy. I apologize in advance, but this is valuable information, that is better explained with some degree of detail.

As interest rates rose rapidly over the past 18 months, the appeal of investments such as GICs, money market, and high interest savings grew in popularity. The real after tax return on those investments however, may not be as high as one might think....but it depends. Remember three terms as we go through today's post.

- yield

- after tax yield

- taxable equivalent yield

Let me start by stating 2 clear assumptions for today's exercise

- the following does not apply to tax exempt accounts like RRSPs and TFSAs. Tax is an inconsequential element in those accounts.

- we are assuming that the investor's tax rate is at the highest marginal rate in Ontario

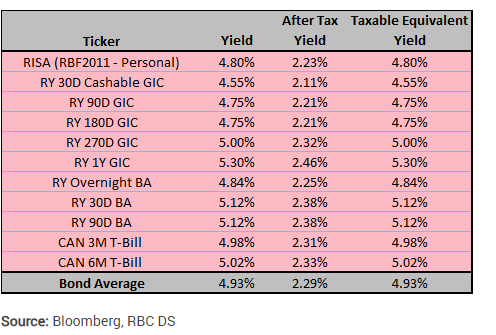

When we examine the following 2 exhibits, what we see is that tax treatment of interest income, can erode the after tax return to the investor. Remember that interest income is taxed at the highest marginal rate. When you invest securities that pay exclusively interest income, you are exposing yourself to the highest level of taxation. There are ways to soften the blow, while getting relatively equivalent quality securities.

In the following examples we look at money market instruments, vs Government of Canada bonds purchased at discount to par. What that means, is that you buy the bond at a discount (due to it's low interest coupon --- it's an older bond that was issued when rates were much lower). When it matures, it will due so at its full par value, and the gain you receive from that is treated all as capital gain. Capital gains tax treatment is more favorable than that of interest income. A simplified example of this would be:

- buy the bond at a discount price of $95

- the bond will mature at full $100 (par)

- $5 capital gain

Isolating an example below:

- purchase a 1 year GIC paying 5.30%. At maturity, you collect 5.30% on your money, but once the tax-man is done with it, your total yield is 2.46%

- purchase a GoC bond that matures in October 2024 (a slightly shorter term) at a discount, and once the tax-man is done with it, your total yield is 3.35%. This means that you would have to find a GIC that paid interest at 7.20% to get the equivalent after tax yield.

Credit to the Portfolio advisor group, Bloomberg, and RBC DS for source work on this.