I'm sure the subject has come up in your house. Or maybe out for dinner with friends, or family. Life has become increasingly expensive over the last few years. Inflation headlines, increases to interest rates, staring at that grocery bill wondering why the 4 is now a 5.....or the 5 is now a 6. Remember back before 2020 when prices seemed reasonable? If it were not for that whole "pandemic thing", where would things really be.

There is one pandemic "hangover" issue that still has yet to hit, and that is MORTGAGE RENEWALS. Remember back during COVID when buying a cottage seemed impossible, because the prices were so high? What about that brand new Mastercraft wakeboard boat (or used for that matter), that you wanted to get but couldn't because all the inventory was sold. I even know people that had to wait 8-12 months for a hot tub! How was all of that paid for?

Most of it was on credit....cheap credit borne from the equity that homeowners had built up. Borrowing at 1-2% didn't really seem like a massive hurdle, when faced with unending boredom of being cooped up at home, only to head out to some long single file line, outside of the grocery store. So the Jones's took out that 5 year, fixed-closed mortgage to buy (insert big ticket item here) because it would only cost them a small amount per month, of extra mortgage payment. Seemed worth it at the time.

Fast forward to today......

Something to think about

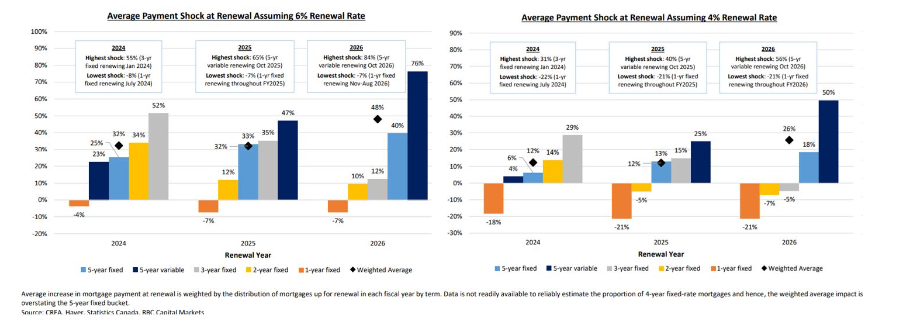

There is a renewal cycle coming in 2025/2026 that could present a real problem for borrowers, and the housing market at large. The state of interest rates in the coming year or two will go a long way in determining whether this renewal cycle is a hurricane we need to be on the look out for, or just some passing showers. See below:

- at a 6% renewal rate, the average payment shock for borrowers renewing will be +33% and +48% respectively for 2025 and 2026. Hurricane level burden

- at a 5% renewal rate, the average payment shock for borrowers will be +23% and +37% respectively for 2025 and 2026. Better, but not by much

- at a 4% renewal rate, the average payment shock for borrowers will be +13% and +26% respectively for 2025 and 2026. Far more palatable against the potential out come illustrated in point 1. Relatively speaking.... a passing shower.