Les sujets abordés |

Les marchés boursiers mondiaux se sont orientés en hausse au cours des dernières semaines, les performances des pays autres que les États-Unis ayant été particulièrement bonnes. L'accent a été mis sur la situation de l'emploi et sur les récents commentaires de la Banque du Canada et de la Réserve fédérale américaine. Les deux institutions ont réitéré la nécessité de faire preuve de patience dans l'attente de nouvelles preuves que les pressions inflationnistes sont contenues. La possibilité d'un atterrissage en douceur est devenue de plus en plus probable et la probabilité d'une récession américaine à court terme a diminué.

L'économie américaine est toujours résiliente

- Le S&P 500 a atteint un sommet historique mercredi le 20 mars,

- Les données économiques américaines se sont améliorées, montrant des signes d'une légère accélération au cours des derniers mois. De plus, plusieurs signaux de récession sont en train de s'inverser, tels que la hausse de l'activité manufacturière, l'augmentation des commandes de biens durables et la baisse des niveaux de stocks par rapport aux ventes.

- Des réductions de taux sont toujours attendues au cours du second trimestre 2024, ce qui pourrait contribuer à la croissance économique.

- Si un atterrissage en douceur se produit, l'une des principales conséquences pourrait être son effet sur l'inflation. Certes, un atterrissage en douceur contribuerait à soutenir un marché du travail solide, des dépenses de consommation stables et un pouvoir de fixation des prix élevé de la part des entreprises.

Bien que les prévisions concernant une récession aux États-Unis soient récemment devenues de plus en plus optimistes, l'incertitude peut encore régner au cours de l'année à venir. Le risque d'inflation, les élections américaines et les risques géopolitiques sont autant d'exemples de catalyseurs potentiels qui peuvent soudainement changer la donne.

En outre, il reste encore plusieurs mois avant que les citoyens américains ne se rendent aux urnes en novembre, et beaucoup de choses peuvent se produire d'ici là. Les procès de Trump, l'âge du Président Biden et la clarté des politiques sont autant de variables qui feront l'objet de vifs débats dans les mois à venir. Si Joe Biden était réélu, nous assisterions théoriquement à moins de changements. Donald Trump, quant à lui, pourrait apporter plus de volatilité aux marchés. Quel que soit le vainqueur, le résultat de l'élection américaine ne devrait pas avoir d'incidence significative sur les portefeuilles à long terme. Comme on peut le voir ci-dessous, les leaders républicains et démocrates ont tous les deux connus des rendements attrayants au cours de différentes périodes.

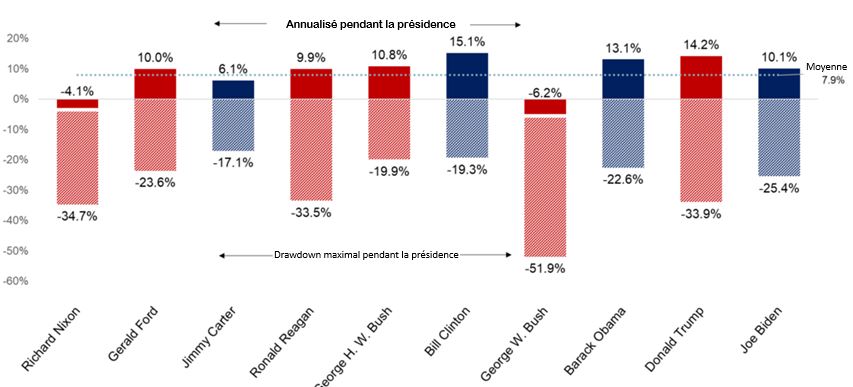

Rendement annuel moyen et baisse maximale selon l’administration élue

Source: RBC GAM, Morningstar: RBC GAM, Morningstar. Période allant du 20 janvier 1969 au 4 mars 2024. Performance du S&P 500.

À retenir

- Les mandats des démocrates ont rapporté en moyenne 11,1 %, contre 5,8 % pour les mandats des républicains.

- Plus particulièrement, les mandats présidentiels ont affiché une baisse moyenne de 28,2 % tout en offrant un rendement annualisé moyen de 7,9 % depuis 1969. Cela met en évidence la volatilité intermittente que peuvent afficher les marchés à court terme, mais aussi les rendements positifs constants que peuvent afficher les marchés à long terme, quel que soit le président.

Notre stratégie

Revenu fixe

Au début de l'année 2024, les rendements mondiaux ont été volatils. Les indicateurs de l'inflation mondiale ont continué à s'améliorer, mais les craintes d'une stagnation des progrès ont poussé les marchés à exclure les baisses de taux d'intérêt à court terme. Il en demeure que de modestes réductions de la part des principales banques centrales soient encore attendues plus tard dans l'année. Bien que les rendements proposés aient considérablement baissé par rapport aux sommets atteints fin 2023, ils restent bien supérieurs aux moyennes des 20 dernières années. Nous restons donc attentifs à toute hausse des rendements afin d'étoffer notre portefeuille obligataire, comme nous l'avons fait à l'automne dernier.

Actions

Nous continuons de croire qu’un portefeuille bien diversifié doit être exposé aux actions mais nous sommes tout de même vigilants. Des corrections ne peuvent être exclues, et certains signaux précurseurs importants des marchés baissiers ne sont pas encore visibles. De plus, si la probabilité d'une récession aux États-Unis a diminué, elle ne peut être exclue. Cette situation continue de se refléter dans notre sélection des titres puisque nous recherchons toujours des titres de participation de grande qualité, qui augmentent les dividendes qu’ils versent aux actionnaires.

Cela dit, il est important de garder une perspective à long terme et de ne pas mettre l’emphase sur des bruits intermittents. Nous continuons de nous concentrer sur la recherche d'investissements de haute qualité à des prix abordables. Le prix que nous choisissons de payer est le facteur le plus déterminant de la réussite de nos investissements et nous veillons toujours à conserver suffisamment de liquidités dans nos portefeuilles pour profiter des opportunités qui s’offrent à nous.

« Quelqu’un est assis à l’ombre aujourd’hui parce que quelqu’un a planté un arbre il y a longtemps. »

- Warren Buffett, investisseur légendaire

Comme toujours, nous sommes à votre disposition pour répondre à vos questions.

Cordialement,

Benoit Legros, B.A.A., CIM, FCSI

Gestionnaire de portefeuille et conseiller principal en gestion de patrimoine