We size up the bounce in global equities, but we caution that this is no time to be complacent as plenty of uncertainties and risks could shake markets.

Most equity markets have rallied substantially since Mar. 23, the day many country and global indexes hit a low point. Since then, the S&P 500 has jumped 25.1 percent, while Canada’s S&P/TSX has climbed 23.8 percent and Europe’s main benchmark has bounced 15.9 percent—all in less than a month.

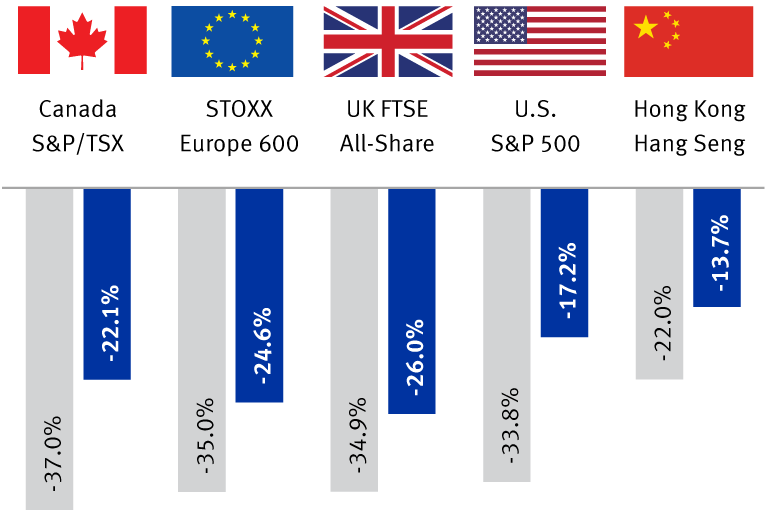

These moves have mitigated the damage that has occurred since global benchmark indexes reached all-time highs in mid- February. For example, instead of the S&P 500 being down 33.8 percent from the global peak to its low point, it is now down “only” 17.2 percent. Other markets have improved as well, as the chart illustrates.

Equities have bounced sharply for a number of legitimate reasons, and this is not an unusual phenomenon during major bear market periods of the past 20 years. In fact, the S&P 500’s move is roughly in line with recent history.

But this is no time to be complacent about market risks, of which there are many. We continue to believe it is appropriate to hold equities at the Underweight level in portfolios—this is below the long-term strategic recommended level. The strength in equity markets allows those who are not yet Underweight to reposition portfolios.

We outline the catalysts behind the recent rally, compare the moves to prior bear market periods, and discuss the lingering risks.

Equity indexes have recovered some of their lost ground

Index performance since the MSCI All-Country World Index peaked on Feb. 12, 2020

Peak to trough level (Feb. 12 to Mar. 23)

Peak to current level (Feb. 12 to Apr. 16)

Source - RBC Wealth Management, Bloomberg

Morale boosters

The avalanche of negative COVID-19 news—that sometimes piled onto equity markets by the hour—has receded, and some glimmers of light have started to shine through, boosting equity markets in the past few weeks:

- The spread of COVID-19 infections has eased in the U.S., Canada, and Western Europe. The daily number of deaths has declined in some of the hardest-hit areas, such as Italy, Spain, and New York.

- There are signs that some parts of major economies— whether it be in certain regions or a limited number of industries—could begin the process of opening up in weeks rather than months.

- The historic $2.3 trillion in lending and bond purchase facilities recently announced by the Federal Reserve to shore up and support the credit market, including high-yield debt, was well received by equity markets. It removed the risk of an imminent credit crunch. Furthermore, market participants realize the Fed still has more arrows in its quiver.

- The OPEC+ deal to significantly cut oil production by 9.7 million barrels per day removed a potential negative from the crude oil and equity markets. Of course, the oil market remains quite weak due to the collapse in demand caused by COVID-19 shutdowns, but at least major oil-producing countries can begin the process of whittling down supply.

Understanding what this rally is

While the catalysts that drive bear market rallies differ dramatically from one bear market to the next, it’s interesting that the magnitudes of the rallies are similar.

For example, during this COVID-19 crisis, the S&P 500 climbed 27.2 percent from Mar. 23 through Apr. 14, its recent high point.

During the bear market associated with the bursting of the tech bubble and 9/11 attacks, the S&P 500 rallied between 19.0 percent and 21.4 percent on three separate occasions, according to Bloomberg.

During the global financial crisis bear market, the S&P 500 staged two big rallies less than one month apart in late 2008. The first was an 18.5 percent move, followed by a separate 24.2 percent run.

Such moves provided opportunities to reposition portfolios until the full bear market cycles were flushed out of the system.

Potholes await

Despite the glimmers of hope and the slower pace of negative news lately, there are still a number of risks facing this COVID-19 bear market:

- The stream of negative economic data has only just begun. We believe market participants are bracing for record-breaking or near-record-breaking declines in a host of data in a number of countries, and for deep (and brief ) recessions in major economies. A lot of bad news is already factored into markets. But it’s not yet clear if market participants are underestimating (or overestimating) the magnitude and duration of the economic retrenchments. Perhaps even more importantly, it is not yet clear whether they are gauging the recovery trajectories properly.

- The process to open up major economies is not without complications and health risks. Increasingly, business groups and some elected officials are calling for mass “testing, testing, testing” as a key requirement to get things moving again, but COVID-19 and antibody testing are not yet widespread in the U.S. and many other countries.

- The start of Q1 earnings season so far has revealed what market participants know—there is a lot of uncertainty about what Q2 earnings and beyond will look like. The 2020 Refinitiv I/B/E/S consensus estimate for the S&P 500 of $142 per share has fallen meaningfully, and we think it will continue to push lower. RBC Capital Markets recently cut its 2020 estimate to $135 per share, but there are downside risks to this estimate if the presumed economic rebound in the second half of the year is muted or pushed back.

- There is anecdotal evidence that many institutional investors are looking past the earnings valley of 2020, and ahead to 2021. This makes sense given equities should be valued on a multiyear stream of profits, not just on earnings for a couple of quarters or one year. But the view of 2021 is cloudy at this stage given the lingering risks associated with the opening up of major economies and the spread of the virus. Will there be additional COVID-19 outbreaks in the months ahead or next year? RBC Capital Markets has penciled in $153 per share for the S&P 500 for 2021, and this estimate is dependent on any changes in the economic landscape.

Biding our time

We think the lingering uncertainties argue for keeping some powder dry, and holding equities at the Underweight level in portfolios.

In the near term, markets have to contend with weak economic data, a difficult Q1 earnings season, and uncertainties associated with unwinding mass quarantines. Over the longer term, we expect major economies and corporate profits to bounce back.

In Quebec, financial planning services are provided by RBC Wealth Management Financial Services Inc. which is licensed as a financial services firm in that province. In the rest of Canada, financial planning services are available through RBC Dominion Securities Inc.