Preferred Share Guide

- Preferred shares are a nondilutive (to common equity holders) source of funding for companies that rank between common equity and bonds. In case of a company liquidation, preferred shareholders rank behind bondholders in order of payment, but senior to common equity holders. The seniority over common shares also applies to the payment of dividends, as a common equity dividend cannot be paid if a preferred dividend is outstanding. On top of this, for non-financial issuers (not banks or insurance companies), preferred dividends are cumulative. This means if a preferred dividend is missed then it is added to the next dividend payment.

- Preferred shares are considered to be 50% equity and 50% debt by ratings agencies. They offer a less secure payment stream than a bond and their dividends (more tax friendly than bond coupons) are not legal obligations. Historically, preferreds shares have been less/more volatile than equities/bonds, respectively.

Market Characteristics:

- The preferred share market is less than 5% of the bond market in Canada. Its small size results in lower trading volume. Less liquidity can make entering and exiting positions challenging, particularly during times of stress.

- Institutional investors are often too large to own individual preferred share issues, so the primary participants are retail investors.

- Banking, insurance, and energy companies are generally the largest issuers and account for two thirds of outstanding preferreds.

- The market has evolved over the last decade, and rate resets now make up around 80% of outstanding issues. That means that most of the preferred share universe is positively correlated to interest rates.

Types of Preferreds:

Floating Rate Preferreds

- Dividend adjusts on a monthly basis and the adjustment is directly linked to the Canadian bank prime rate.

- When prime rate is increased, the dividend increases. Positive correlation to interest rates.

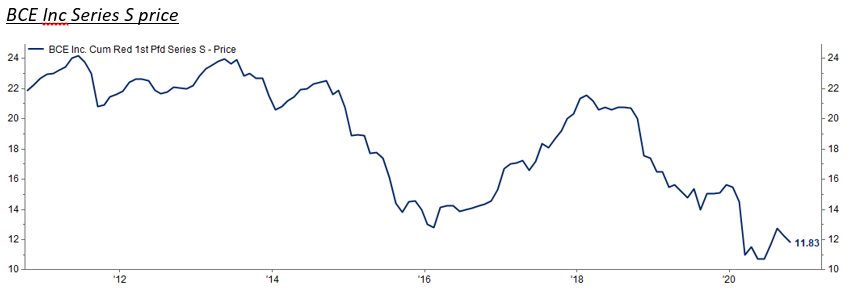

- Example floating rate: BCE INC Series S

- Trades at 100% of prime and adjusts on a monthly basis

- Dividend calculation: Prime rate * Issue price = 2.45% * $25 = $0.6125

- Current yield = dividend / current price, $0.6125 / $11.83 = 5.18%

Rate Reset Preferreds

- Dividend adjusts every 5 years and is directly linked to the Government of Canada 5 year-bond yield. The adjustment formula is = GoC 5 year yield + X, where X is a fixed reset spread determined when the preferred share is issued.

- Not all issues in this part of the market are equal. The fixed reset spread is key, higher spreads will pay higher future dividends and offer a greater margin of safety if interest rates go down.

- Positively correlated with interest rates.

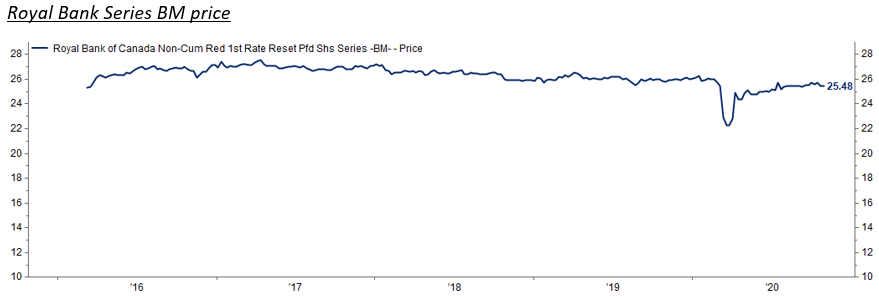

- Example rate reset: Royal Bank Series BM

- Reset spread is +4.80%

- Dividend will reset every 5 years at BoC 5-year bond yield + 4.80% (big reset spread, relatively high margin of safety)

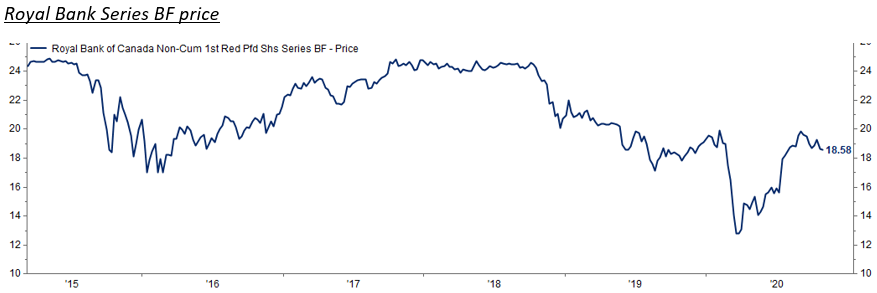

- Example rate reset: Royal Bank Series BF

- Reset spread is +2.62%, so the dividend will reset every 5 years at the BoC 5-year bond yield + 2.62%.

- Lower reset spread has resulted in meaningful underperformance compared to the previous rate reset issue.

Perpetual Preferred Shares

- The dividend remains fixed into perpetuity

- Theoretically negatively correlated with interest rates (similar to bonds). If interest rates decrease and the yield on perpetual issues stays the same, the relative attractiveness of these issues will rise.

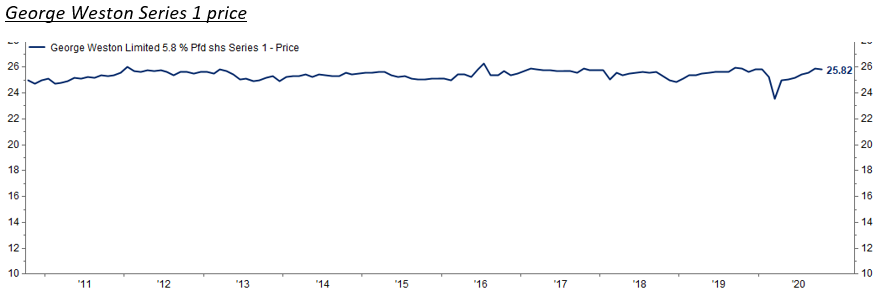

- Example perpetual issue: George Weston Series 1

- Pays a $1.45 dividend annually into perpetuity

- Current yield = dividend / current price, $1.45 / $25.82 = 5.62%

Takeaways:

- The preferred share universe is diverse as there are multiple types of issues with unique characteristics.

- Most issues in the preferred index are positively correlated to interest rates (floating rate and rate reset issues) so they have depreciated over the last decade as rates declined.

- Not all rate resets are created equal and their leverage to interest rates (reset spread) is a key factor to consider.

- Most preferreds yield over 5%, a particularly attractive dividend yield when compared to Canada 10-year bonds yielding 0.7%. They can play an important role in fixed income portfolios.

We would be happy to answer any questions you may have, please do not hesitate to reach out to our team.