...the Wealth Effect, whereby rising markets cause investors to feel richer and more confident, leading them to spend more and stimulate further economic growth.

Another example – and an important one at the moment – is capital raising. A rising market by definition indicates a willingness from investors to buy assets, while also providing companies with increasingly compelling prices at which to sell shares or issue bonds. The proceeds from issuing new debt or equity is then (ideally) spent by businesses on growth initiatives, providing a positive impulse for the economy through more jobs and higher business spending.

Right now, the capital raising window for companies is wide open. This has been most evident in the US bond market, where the year-to-date flow of new investment-grade bonds exceeds that of 2019 by almost 50% even while the yield on offer has dropped below 2%. But as the recovery continues, the ability access to fresh money is becoming increasingly evident in riskier assets too. In equity markets, for example, a string of large and high-profile IPOs are expected to be priced in the coming weeks including Rocket Co’s, Ant Group and Palantir. The US high-yield debt market has also come back to life, with issuance now above 2019’s levels.

In short, the ability for large companies to fund growth initiatives is remarkably good right now. Of course, this is exactly what central banks have aimed to engineer, and it has the potential – along with the Wealth Effect – to add a self-reinforcing tailwind to the economic recovery that we’ve been witnessing since May. As a side note, cheap and abundant financing also implies a coming increase in corporate takeovers, with opportunistic management teams opting to buy growth rather than build it in a recovering economy.

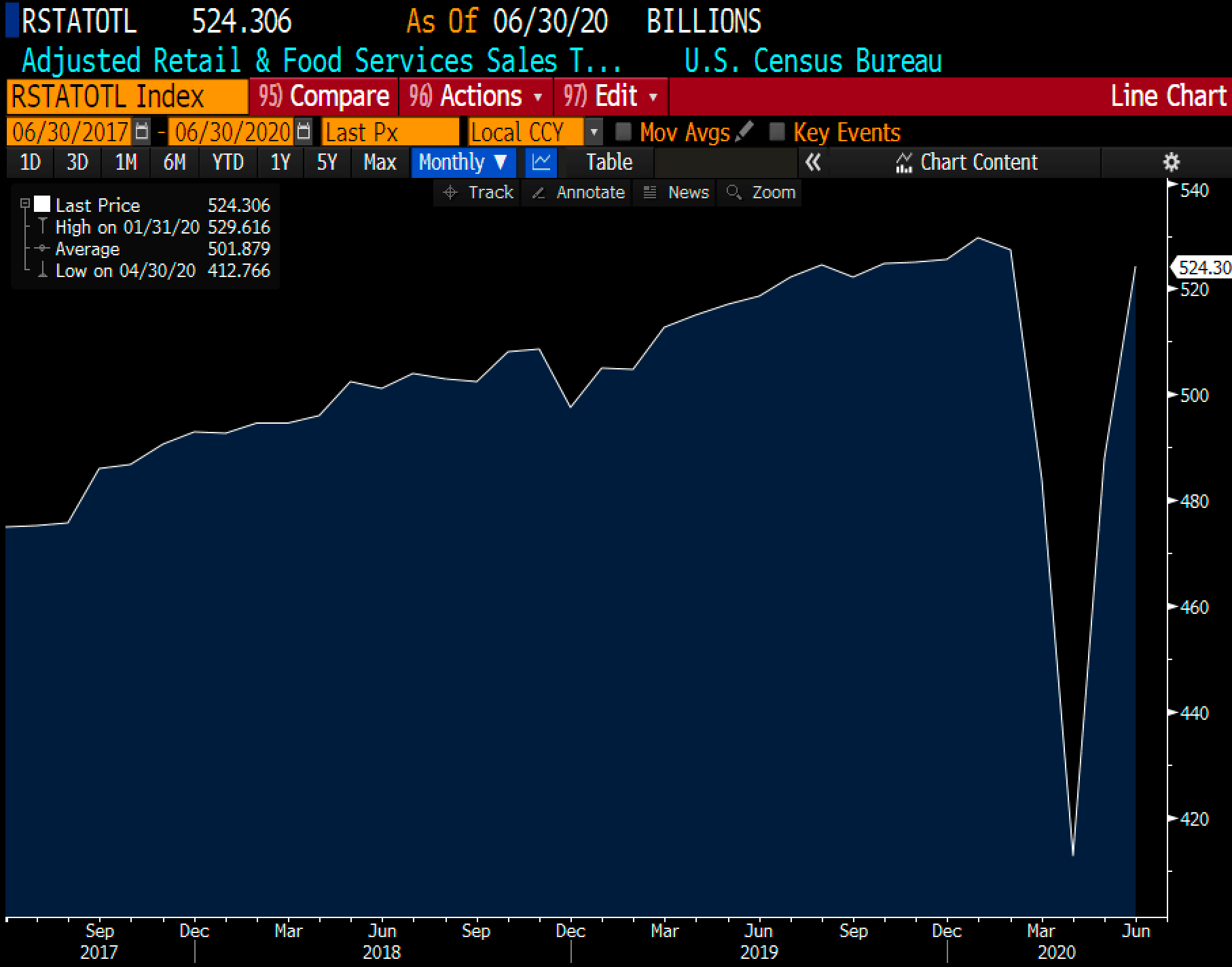

As these indirect tailwinds have built steam, direct data on the global economy has evidenced a stunningly strong rebound in the demand for goods. For example, look at the value of US retail sales below; would you have guessed that as of June, retail sales are tracking at only 1% below January’s pre-COVID high?

US Retail Sales (SA, billions): 3-years to June 2020

Source: Bloomberg, US Census Bureau

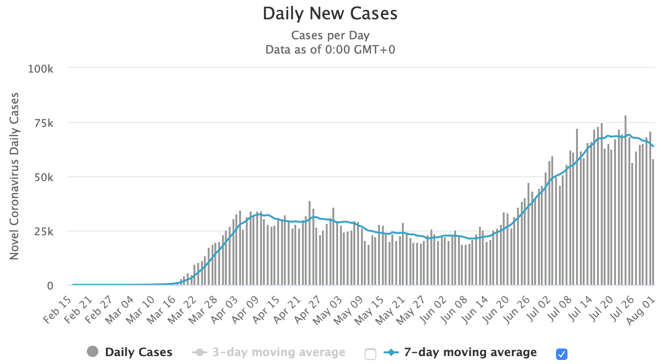

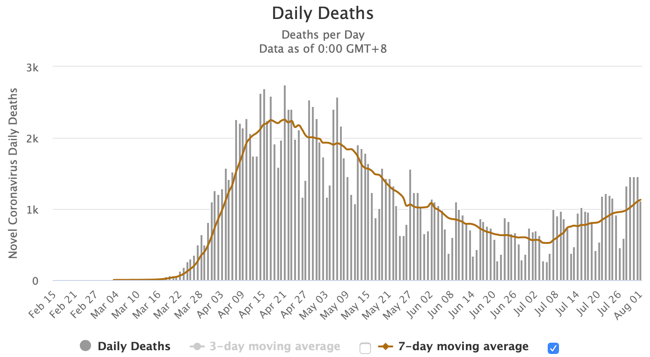

One could question whether the July spike in US infections will cause this figure to resume falling. However, high frequency data like credit card spending and cell phone traffic at malls suggest that even the hardest hit counties in Texas and Florida are experiencing – at worst – only a pause in gains rather than a renewed decline in consumer activity. Arguably, this suggests that economic reopening strategy is actually working as planned…after all, while daily new cases started hitting record highs in the US exactly a month ago, daily deaths today remain at only about half of April’s peak. With the caveat that I am not a medical professional, given the ample time for the lag on deaths to have caught up, this presumably reflects better protection of high-risk groups as well as progress in medical knowledge on how to treat severe cases. Both are encouraging observations in a period where the economy is getting closer to normal.

USA: daily new COVID-19 cases and deaths – Feb 15 to-date

Source: Worldometer

The surge in consumer demand is now set to pass through to manufacturing, where last quarter’s inventory destocking exceeded that witnessed during the Financial Crisis (and anecdotally, we have heard first-hand about inventory shortages from a number of you who run active businesses). While this goods-focused momentum continues, the remaining and very important puzzle piece for a complete economic recovery will be a rebound in the service sector. This includes travel, tourism and entertainment, much of which will be vaccine dependent. Even with this gap though, the economic rebound to-date has been strong enough to result in a far better than expected, second-quarter earnings season. Reporting for Q2 is wrapping up now, with roughly 80% of companies exceeding Wall St earnings estimates by an unprecedented average of +15%.

Putting it all together, the case is compelling case for equities to continue drifting higher as the rate of economic improvement slows but stays positive, and self-reinforcing mechanisms start to kick in. From an equity investor’s perspective, this scenario has a few interesting implications.

First, if you have rising confidence that the economy is going to grow its way out of the pandemic, then cyclicals stocks start looking much more attractive…why bother paying a high valuation for the safety of secular grow stocks (i.e. the Tech sector) when you can pick up a cyclical on the cheap that likely has more torque to a recovery anyway? To this end, returns on Industrials as well as some Consumer and Financials stocks could reasonably start to improve.

Second, the US dollar could continue to weaken moderately. After two years of trading in a very tight range, the USD has fallen notably against other major currencies over the past 45 days. A continuation of this trend seems limited without oil prices increasing amongst other things, but it will still provide a welcome tailwind to the earnings of US-based multinationals as well as a talking point for the financial media.

US Dollar Index (“DXY”): 2-years to July 31, 2020

Source: Bloomberg, ICE

Source: Bloomberg, ICE

Finally, a continued upward drift in financial markets buys the economy more time for a vaccine. Fancy data analysis aside, the unanswerable question remains what will happen on the public health front this winter. There seems to be general acceptance that infections will rise, so the question not so much whether there will be a second-wave, but rather whether it will be manageable. While it is easy to skew negative when pondering the market impact of this, if we are being fair then the probabilities actually work both ways: what if a second wave indeed proves manageable; or what if a vaccine is declared effective; or what if simply medical progress is being made while government support programs continue to be announced and extended? Such outcomes can’t simply be dismissed on account of sounding pleasant. While we wait for the future to unfold though, the fact that financial markets are “showing the money” to companies for now plays an important role in buying the economy more time for a positive resolution.