This is the second report of a four-part series on the 2024 U.S. general election. Part I is available for review.

Updates and recent developments

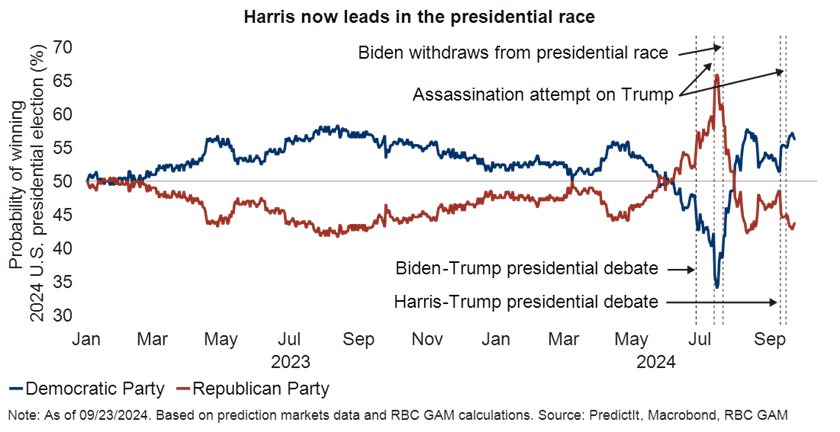

With the U.S. elections over a month away, we thought it would be a good time to provide an update on recent developments. Mercifully, since we published our first piece in early August, there has not been anywhere close to the level of uncertainty that was present through the earlier part of the summer. Though to be fair, the second assassination attempt on GOP presidential candidate Donald Trump in early September beggars belief, and one cannot help but wonder about the polarized state of U.S. politics today. While we suspect this latest attempt on Trump’s life has only served to galvanize support across his staunchly loyal base, it has done little to meaningfully increase the odds of a Trump presidency in betting markets, nor did it seem to faze the investments markets.

On the other side of the electoral divide, momentum in the Harris campaign has been remarkably solid. Shortly after accepting the Democratic nomination as the party’s presidential candidate, Vice President Kamala Harris experienced a swell in support, endorsements and fundraising. In August alone, Harris raised just over $360 million, outpacing the Trump campaign nearly threefold. In the 24 hours after the presidential debate on September 10, the Harris campaign raised a whopping $47 million – the largest 24-hour fund-raising period since Harris’ initial burst of donations when she first entered the race in July (and raised $81 million!). Note that the Trump campaign has yet to release a similar fundraising figure after the debate.

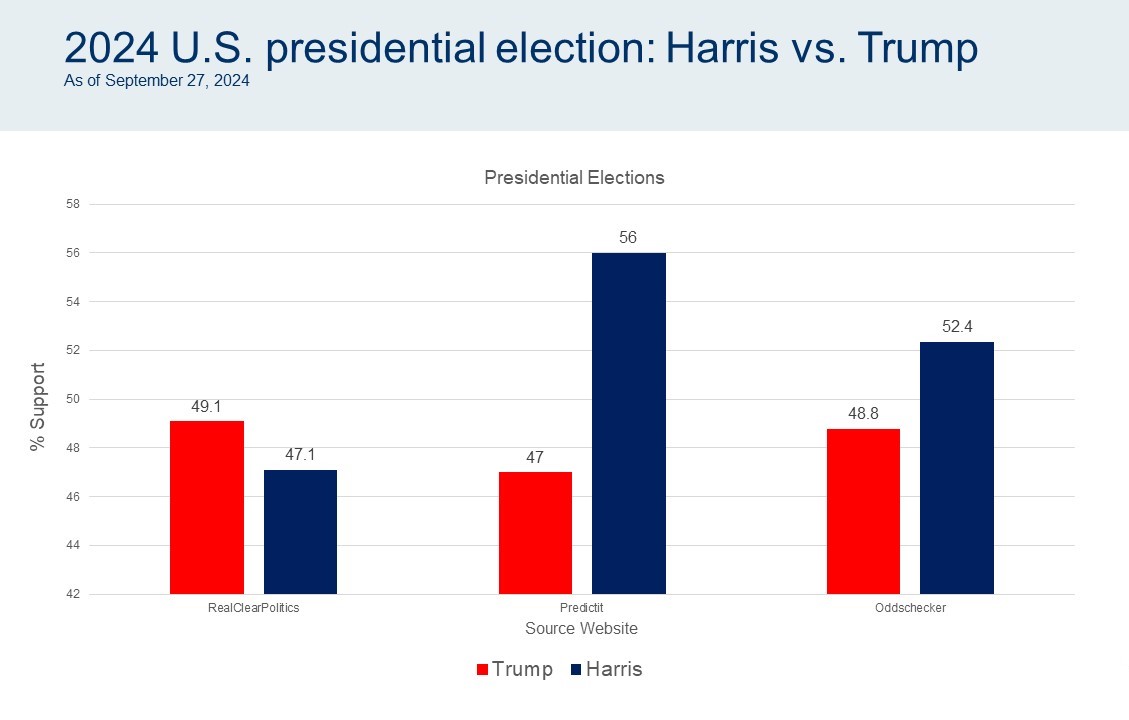

As of the time of writing, and following the recent debate, several respected election betting sites such as PredictIt, RealClearPolitics, and Betting Odds have shown betting odds on the rise for Harris.

Despite Harris’ (narrow) advantage, the race is tight. We would also caveat that the probabilities thrown out by the betting markets are not the same as polling numbers, which suggest a much closer race. There is plenty of time for shifts in momentum for either candidate as we approach election day on November 5.

In the discussion that follows, we hope to provide a broad overview of each candidate’s economic platform, and how this election could impact us in Canada. While it is reasonable to anticipate heightened market volatility in the lead-up to the elections, we would be remiss if we did not reiterate our view that in the medium-to-long term, elections matter far less to investment markets than the outlook for GDP and corporate earnings growth. In fact, specifically with respect to the current economic cycle, the Federal Reserve’s path for rate cuts for the balance of next year and into 2025 are far more consequential to economic growth and market performance than the election.

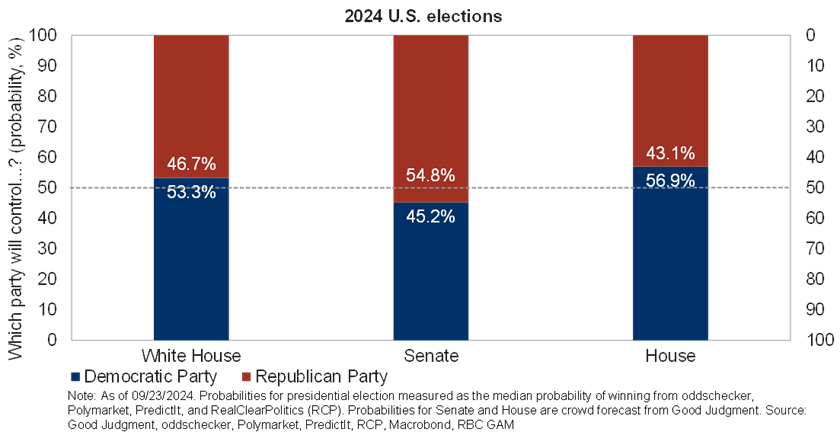

Lastly, the outcome of Congressional elections has far more bearing and influence than what a presidential candidate says they are going to do, given the limits to what a president can actually affect once in office. A scenario in which Congress remains in a state of gridlock – as it is today – or the opposing party is in control, is likely preferable to the markets, which inherently dislike uncertainty. At the time of writing, betting markets suggest a narrow majority in the White House, with the Republicans in control of the Senate and the Democrats in control of the House of Representatives.

Vice President Kamala Harris’ economic agenda: Something old, something new, something borrowed, something blue

During her bid for the 2020 Democratic presidential nomination, Harris’ campaign struck quite a progressive note, particularly versus other would-be candidates, including then presidential hopeful, Joe Biden. Her platform at the time included a large corporate tax hike (to 35%), universal basic income, Medicare for all, banning fracking, and implementing the Green New Deal.

Suffice to say that her 2024 policy agenda has toned down her “progressiveness,” as she tries to “hug the middle” and draw undecided centrist voters to the Democratic blue zone. For example, she is now calling for a corporate tax hike to 28% (up from 21% and in line with Biden’s proposal), has retracted her intention to ban fracking (which in effect raises questions about her support for the Green New Deal), and is no longer a “Medicare for all” champion.

In keeping with Biden’s agenda, Harris has also proposed increasing the top marginal tax rate for individuals regardless of income type, maintaining the Inflation Reduction Act and environmental priorities, preserving Obamacare, and tightening the southern border to illegal immigration.

This year’s campaign focuses on a host of issues across both economic and foreign policy. Going through all these issues exhaustively is beyond the scope of our discussion, but in the following, we highlight a few points that we believe are important and topical:

What Harris wants

-

The enhanced Child Tax Credit is one of Harris’ signature policy issues: While this policy is technically new, it builds on the ambitions of outgoing President Biden’s administration which endeavored to pour billions of taxpayers’ dollars into making childcare and home care for the elderly and adults with disabilities more affordable. The Vice President is proposing an expansion of the Child Tax Credit to $3,600 from $2,000 – matching the temporary increase implemented by the Biden administration in 2021 as a COVID-19 pandemic relief measure (though it was only in effect for one year). In addition, she is calling for a $6,000 credit for newborns in their first year of life.

Former President Trump’s campaign is proposing a $5,000 per child yearly tax credit. Whereas Trump would have the credit go to all families regardless of income, Harris would restrict the credit to pay low and middle-income families only. She would also make the credit “refundable” (i.e., parents who do not pay taxes due to low incomes would get the credit in cash).

-

Ban on “price gouging” at grocery stores and food suppliers: This proposal, introduced under the Harris platform, forms part of a broader agenda aimed at lowering the cost of housing, medicine, and food. Given that grocery prices shot up by more than 20% under the Biden-Harris administration, this ban seeks to tackle one of the Harris’ campaigns vulnerabilities head-on: Americans’ disillusionment and frustration with inflation. Such a ban, in theory, would prevent food and grocery companies from hiking prices by an egregious amount over a certain period, according to our understanding (and given the vagaries of the proposal at this stage). The idea that this proposal may replicate similar bans currently implemented in over 30 states has been floated, those bans specifically prohibit companies from exploiting a sudden imbalance between supply and demand (e.g., a natural disaster or health crisis) by significantly hiking prices. Still, details of the policy remain limited, and it is not clear whether such a measure would control the rise of food prices, how it would be enforced, or even if such intervention is desirable. Trump for his part has lambasted this proposal and referred to it as a “Communist” era price control.

-

Enhanced home buyer affordability: The Harris campaign has said it will provide first-time homebuyers with up to $25,000 to help with their downpayments, with more generous support for first-generation homebuyers. Other details include alleviating the housing supply shortage with the construction of three million new housing units, while preventing Wall Street investors from buying homes in bulk. Officials said she will propose a new $40 billion innovation fund – doubling the $20 billion proposed for the Biden-Harris innovation fund – that would be used for local governments to fund local solutions to build housing and support construction financing.

The Trump campaign has released some details on how it intends to address home affordability, including reduced regulations on open swaths of federal land for large-scale housing construction. While it is not clear what types of regulations Trump would like to target, it is not out of step with President Biden’s call on federal agencies in July of this year to “assess surplus federal land that can be repurposed to build more affordable housing across the country.”

Trump has also linked housing costs to one of his key platform issues – immigration – and has said he would ban mortgages for undocumented immigrants, thereby lower housing costs which he claims have been driven higher by the unsustainable influx of migrants across the border. It is not clear how significant or even real an issue this is, as it is generally difficult, if not impossible, for immigrants to qualify for a mortgage given valid documentation is required for the application process.

-

Taxation of unrealized gains is a proposal that Harris carried over from the Biden administration. Currently no such tax exists. Under the current system, the federal government only taxes profits from stock investments (capital gains) once a stock is sold (i.e., a realized capital gain). Under the new proposal, Harris would impose a tax on stock holdings as their value increases – irrespective of whether they are cashed. That said, this tax would only apply to a narrow cross section of the U.S. population and is targeted at the ultra-wealthy with net assets of at least $100 million – which is some 11,000 individuals in the US (out of a population of roughly 330 million) according to an estimate by Henley & Partners.

There are undisclosed details around the complexity of such a proposal. For example, the glaring asymmetry of the proposal to the extent that taxes are levied on unrealized capital gains, but investors are not refunded for capital losses. The fluctuation and accurate determination of the value of unrealized capital gains contributes to such complexity, and details are few on how such a tax would be enforced.

Not surprisingly, there has been plenty of opposition to this proposal both from within the GOP and from without. Note that Biden could not get the proposal passed even when he presided over a slim majority in the House and Senate in the first part of his term. The Trump campaign has panned this proposal calling it “the craziest idea” as it could discourage investment and drain capital. We suspect the lack of popularity of such a proposal would ultimately suggest that turning it into law would face considerable hurdles.

Some other issues of note

-

A little more on taxes: The Tax Cuts and Jobs Act (TCJA) was enacted into law by former President Trump in 2017, and included lower tax brackets, a higher standard deduction, and a boost to the Child Tax Credit, among other changes. Several provisions of the TCJA are scheduled to expire at the end of 2025. This looming deadline comes at a time when the middle class are still struggling with inflation-driven cost of living increases.

Trump has indicated his commitment to extending the TCJA if he is elected to a second term. Harris has not explicitly said she will preserve the Act, but we believe there is a possibility she may simply change some or several of the provisions and repackage the Act, rather than doing away with it completely. She has also said she plans to reduce taxes for the average middle-class American in her own ways. For example, through the expanded Child Tax Credit, and restoration of the Earned Income Tax Credit (EITC), which was around $1,500 for workers without dependent children.

Harris has broadly aligned with President Biden’s proposals around bringing the corporate tax rate back up to 28% from 21%. Further, Harris supports raising the capital gains tax rate to 28% from the TCJA’s 20% on people earning $1 million or more a year.

The Trump campaign has previously advocated for a lowering of the corporate rate to 20% or less. He recently called for a reduction to 15% for companies that make their products exclusively in the U.S. and has proposed tax credits and accounting incentives for such companies. On capital gains, Trump intends to extend the TCJA rules, which suggest long-term capital gains rates of 0%, 15%, and 20%, depending on income level.

-

Trade:

With China: The general expectation is that a re-elected Trump and his administration will take a harder stance on foreign policy generally, especially as it pertains to China. This is completely in step with the foreign policy during his first term. Earlier this year, the former President spoke openly about plans to escalate the U.S.-China trade war should he be re-elected. Trump proposed a tariff of 60% or higher on Chinese goods in his potential second term – which is roughly four times the average levy of his original policies.

The Biden-Harris administration never did away with Trump’s China tariffs despite campaigning to remove them during the 2020 election. In the years since his election, Biden has in fact added to the tariffs. This year, Biden issued new tariffs on $18-billion worth of Chinese imports narrowly focused on a few strategic industries. The Biden administration has touted this as a “smart approach” by targeting goods such as electric vehicles, solar cells, steel, aluminum, and certain medical equipment, ostensibly to fend off the growing technological threat that China presents. In a more recent escalation, the U.S. Commerce Department proposed prohibiting critical Chinese software and hardware in connected vehicles on American roads due to national security concerns. Such a move would be an effective ban on nearly all Chinese cars from entering the U.S. market.

The Harris Democratic platform promises a “tough but smart” approach toward China. It makes no apology in refuting what it believes are unfair trade practices that harm American workers, but caveats that it does not seek conflict in addressing those practices through tariffs. While Harris herself has not voiced support for significantly raising tariffs on Chinese imports, she has neither suggested lowering or eliminating them. Experts have said she is likely to continue Biden’s tariff policies.

All told, it seems that tensions between the two countries are unlikely to cool irrespective of who leads the next administration. Our overall view is that any escalation of tension by way of more punitive tariffs has the potential to add to inflationary pressures domestically. From a market perspective, an escalation of the trade war by the magnitude put forth by Trump would likely drive-up near-term volatility, at least in the short- to medium-term.

With Canada: The U.S. is Canada’s largest trading partner, with more than 75% of our exports (namely energy and vehicles) going to our southern neighbour. Donald Trump’s campaign has proposed a 10% tax on the $3 trillion in merchandise that the U.S. imports each year from all countries –

including Canada. More recently, Canada’s ambassador to the U.S. stated the U.S.-Mexico-Canada Agreement (USMCA) for free trade, negotiated during Trump’s first term and which replaced the two-decade-old North American Free Trade Agreement (NAFTA), should automatically exclude it from his 10% tariff proposal. It was Trump’s contention during his first term that NAFTA led to the loss of manufacturing jobs in the U.S. The USMCA comes up for review in 2026, and Trump’s economic advisors have suggested the 10% across-the-board tariff would unlikely apply before that. However, this still leaves the door open for additional tariffs for Canadian imports upon review.

Canadian officials have already begun talks with members of Trump’s economic team about avoiding new trade tariffs should he be elected in November, and they have also vowed to respond with reciprocal tariffs. An inflationary tariff war between Canada and its largest trading partner has the potential of compounding an already softening economic and labour market narrative at home, and it will likely weigh on market sentiment meaningfully in our view.

We suspect that the Harris administration will seek little change to the current state of trade between the US and Canada, even though the Democratic candidate has not commented on the review of the agreement in two years.

Keep calm and invest on

Elections often matter more in the short term than the long term. Investor nerves around election time are completely understandable, but knee-jerk reactions in portfolios due to such nerves are unwarranted in our view. As discussed, over the medium to long term, elections matter far less to investment markets than the outlook for corporate earnings and GDP growth. Our Investment Counsellors, many of whom have lived through several U.S. election cycles, have the experience and perspective to look beyond the noise that is so characteristic of the U.S. presidential campaign trail. This level-headedness is reflected in the well-diversified portfolios that they have constructed for our clients, which are based on robust investment frameworks and geared towards long-term horizons, all of which should help withstand transitory bouts of volatility. Against this backdrop, it is our view that staying the course is the best “vote” to cast in the coming months and beyond.

This document has been prepared for use by RBC Phillips, Hager & North Investment Counsel Inc. (RBC PH&N IC). The information in this document is based on data that we believe is accurate, but we do not represent that it is accurate or complete and it should not be relied upon as such. All opinions and estimates contained in this document constitute RBC PH&N IC judgment as of the date of this report, are subject to change without notice and are provided in good faith but without legal responsibility. This report is not an offer to sell or a solicitation of an offer to buy any securities. Persons, opinions or publications quoted do not necessarily represent the corporate opinion of RBC PH&N IC. This information is not investment advice and should only be used in conjunction with a discussion with your RBC PH&N IC Investment Counsellor. This will ensure that your own circumstances have been considered properly and that action is taken on the latest information available. Neither RBC PH&N IC, nor any of its affiliates, nor any other person accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or the information contained herein. This document is for information purposes only and should not be construed as offering tax or legal advice. Individuals should consult with qualified tax and legal advisors before taking any action based upon the information contained in this document. RBC PH&N IC, RBC Global Asset Management Inc. (RBC GAM), and Royal Bank of Canada are all separate corporate entities that are affiliated. RBC PH&N IC is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / ™ Trademark(s) of Royal Bank of Canada. RBC, RBC Wealth Management and RBC Dominion Securities Inc. are registered trademarks of Royal Bank of Canada. Used under license. © RBC Phillips, Hager & North Investment Counsel Inc. 2024. All rights reserved.