The snow is finally here! Happy New Year to everyone, we hope you enjoyed your time over the holidays with friends & family.

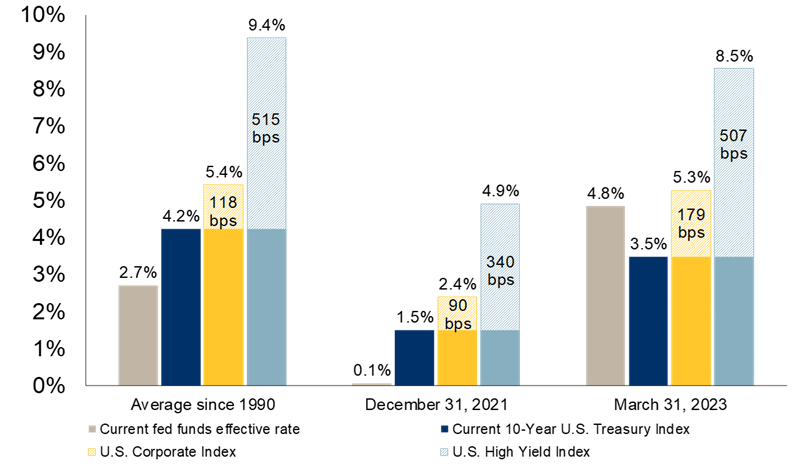

Investors enter 2024 faced with several continuing challenges but surging bonds yields are now a valuable complement to a balanced portfolio. Today, a combination of government and investment-grade corporate bonds is yielding north of five percent. We believe that makes bonds once again a valuable adjunct to equities in a balanced portfolio. Providing a combination of reduced volatility, more predictable returns, and the comfort of a maturity value as they have traditionally done.

What does higher bond yields mean for equities?

First, it reduces the need to buy equities for income to make a long-term financial plan work. At one point in the post-pandemic period, more than 60 percent of the stocks in the S&P 500 sported dividend yields in excess of the 10-year U.S. Treasury bond yield. Rather than make a multiyear commitment to a bond paying an artificially low rate, an investor was able to acquire the shares of a seasoned, probably well-known company with a higher-yielding dividend and offering the prospect that the dividend might be raised periodically. Consequently, fueled by the need to boost portfolio income, equity exposure in individual investors’ portfolios crept higher over that stretch when bond yields were deeply suppressed by extreme central bank policies. The same trend toward higher equity exposure could be seen in some balanced funds and pension funds. Today, no such obvious income pick-up advantage is widely available in our view. Companies possessing dividend yields competitive with or better than bond yields often have other issues attending them. If individual investors and pension funds find themselves able to achieve their long-term targeted returns and take less risk in the process, many may choose to do so. Lowering equity exposure by a few percentage points and redeploying the funds into fixed income is likely to be a feature of the coming months and quarters.

Second, the need for companies to refinance old loans and take on new ones in this higher-rate world means corporate interest costs are likely to rise, squeezing profit margins if those costs can’t be fully passed on to customers. Only the largest, most seasoned businesses were able to use the pandemic interlude of ultralow interest rates to issue long-term bonds. Many others had to accept shorter maturities. Some 20 percent of high-yield bonds (i.e., bonds of low-quality issuers) will mature in the next 18 to 36 months and will have to be refinanced at higher rates, which for some will likely be difficult. Even more companies are already being squeezed by the fast-rising cost of floating-rate debt. This latter category includes many small-cap companies, which we think goes some way to explaining their persistent underperformance in the stock market over the past year. And finally, sharply rising borrowing costs reduce the spendable income of customers—both individuals and businesses. U.S. consumers are contending with higher rates for mortgages, auto loans, and credit cards.

For now, we recommend remaining sufficiently committed to stocks to take advantage of the distinct possibility of some large-cap indexes led by the S&P 500 reaching new all-time highs in the coming few months. However, we believe investors should consider limiting individual stock selections to companies they would be content to own through a recession, which in our view, is the most probable economic outcome in the coming quarters. For us, that means high-quality businesses with resilient balance sheets, sustainable dividends, and business models that are not intensely sensitive to the economic cycle.

Perhaps the most compelling reason for focusing on resilient, high-quality businesses is that the economic headwinds which have been gathering will, in our view run their course and probably fully dissipate later in 2024. Equity markets typically have anticipated the start of a new economic expansion several months before it gets underway. In our opinion, portfolios that have held their value to a better-than-average degree will be best-equipped to take advantage of the opportunities that are bound to present themselves when a stronger pace of economic growth reasserts itself.

Debate still on

Meanwhile, the hard versus soft landing debate about the likely course of the U.S. economy carries on. It won’t be settled definitively until the Business Cycle Dating Committee at the Nation al Bureau of Economic Research decides on the official start date of any recession that arrives. That announcement usually comes about a year after the recession has begun— making the proclamation itself not very useful for investors. For our part, we are persuaded that the combination of high rates and restrictive bank lending standards in place today is a recipe for recession, just as it has been in the past. Soft landings, on the other hand, have historically featured rising interest rates but no overt tightening of lending standards.

al Bureau of Economic Research decides on the official start date of any recession that arrives. That announcement usually comes about a year after the recession has begun— making the proclamation itself not very useful for investors. For our part, we are persuaded that the combination of high rates and restrictive bank lending standards in place today is a recipe for recession, just as it has been in the past. Soft landings, on the other hand, have historically featured rising interest rates but no overt tightening of lending standards.

Changes

We decided to trim our very successful holding of RBC Global Technology fund (finished up over 53% in 2023) because of its exposure to 5 stocks that had significant gains in 2023. The 5 stocks (Microsoft, Apple, Google, NVIDIA and Meta) are a part of the widely discussed magnificent 7 which took the markets by storm largely because of the excitement around AI technology. While this technology is great it’ll take time to turn it into something profitable and we think share prices may slow and trend sideways until this technology can catch up to the hype.

We reinvested into an alternative strategy focused on maximizing income on a tax efficient basis for taxable accounts as this income is treated like capital gains. For taxable accounts these capital gains are only 50% taxable and the income received today is 11% so on an after-tax basis this is extremely attractive. Take for example a hypothetical investment of $100,000 into a GIC vs our alternative strategy (Dynamic Premium Yield Plus) for an investor with a 33% tax rate (income range of $55,000 to $100,000).

1 year GIC is paying 5.01% today would create $5,010 income minus 33% tax or $3,356.70 AFTER TAX

PYP paying 11% (only 5.5% taxable) minus 33% tax on 5.5% or $9,185 AFTER TAX

As you can see the income received from our alternative strategy will pay you $5,828.30 more after tax in this hypothetical investment example.

Cheers!