In Part I of our serial, we looked at the history of disruptive new technologies from the Industrial Revolution to the Internet Age.

In Part II we looked at how for the first time, a new technology (AI) is coming for cognitive, white-collar work as opposed to past technologies, which tended to target repetitive tasks. We then looked at the J-curve and the tendency for new technologies to have negative near-term economic benefits before generating a long-term productivity surge.

In Part III, we will explore how AI is likely to widen the income gap (section V), historic government responses to disruption and the current lack of any response (section VI) and the very real impact on the software sector over the past half-year (section VII).

Section V: I dream of Gini Coefficient

Productivity gains, even large ones, do not automatically translate into broadly shared prosperity. The Internet productivity boom of 1995–2004 coincided with a dramatic widening of income inequality: the top 1%'s income share rose from roughly 10% to nearly 22% between 1979 and 2007, a period bookended by the two great technology waves of the era. Capital owners and highly-skilled workers captured a disproportionate share of the gains.

Let’s take a look at a chart and then comment:

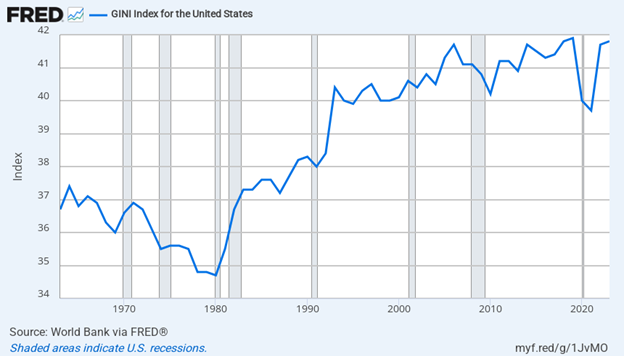

The Gini Coefficient (GC) measures the extent to which the distribution of income or consumption expenditures among individuals or households within an economy deviates from a perfectly equal distribution. A GC of zero would mean everyone has an exactly equal share of income whereas a GC of one would mean that one person (we will call him “Elon”) controls all of the income. As you can see from the chart above, the Gini Coefficient had been mostly trending higher over the past 4+ decades (with a brief pause during Covid) and now sits at 0.47 vs. less than 0.35 in 1980. In other words, income equality has deteriorated by roughly a third over the past four decades, meaning wealth is in fewer and fewer hands.

AI's productivity is likely to lead to similar challenges. In fact, these challenges could potentially be even more acute largely because if AI primarily benefits firms and the workers skilled enough to use it, while displacing workers in moderate-skilled white-collar roles, the net productivity gain could be substantial, while the income is distributed unequally. This is the central policy problem AI presents – significant growth in the economy that is felt by the few and not by the many.

Section VI: historic responses vs. the current non-response

History has taught us a pretty simple lesson about technological disruption and policy responses – those that adopted policies that invested in workers broadly succeeded, and those that tried to manage the transition without investing in workers broadly failed. Let’s explore a few historical examples:

Some attempts were more effective than others

- Mass public education expansion (1850s–1950s): As the industrial revolution took hold, the U.S. responded to the dislocation by dramatically expanding access to education — first compulsory primary and secondary school, then post-secondary access via the Morrill Act land-grant to universities in 1862.

- The GI Bill (1944 – 1956): sent 7.8 million veterans to college or vocational training between 1944 and 1956. Education and retraining combined with automation to drive productivity up 33% from 1940 to 1950 — the most compressed productivity surge in American history — even amid the enormous labor market dislocation of demobilization post WWII. The estimated return on GI Bill investment was $5–7 for every $1 spent in increased tax revenues and reduced social costs.

- Union-negotiated industrial retraining (1970s–80s): When automation began threatening automotive and steel jobs in the late 1970s, Ford Motor Company and General Motors negotiated agreements with the United Auto Workers (UAW) requiring employer contributions of $0.05 per worker per hour to joint training centers — roughly $10M/year for Ford and $40M/year for GM. The UAW-Ford National Development and Training Center became a model for employer-funded retraining. Data from plant closures that used these programs showed only 17.6% of displaced workers remained unemployed two years after closure — compared to far higher rates in plants without such programs.

The U.S. adopts an anti-anti-AI strategy

There does not appear to be any momentum at present for any sort of U.S. Federal government response to AI-disruption. In fact, while more than half of U.S. states have either adopted AI-policies or are exploring the implementation of AI-policies, the Federal government has threatened these states with retaliation, preferring an “AI-dominance” approach. The AI Litigation Task Force, a specialized unit formed in January of 2026 within the Department of Justice (DOJ), has the sole purpose of challenging state-level regulations on artificial intelligence. In other words, the Federal government seems bent on preventing most if not all AI regulation, which, given the speed in which AI is evolving, could have profound long-term consequences.

Section VII: The software sector “highlights” the potential impact of AI

Speaking of consequences – let’s take a look at the software sector, which has been in the “AI-crosshairs”.

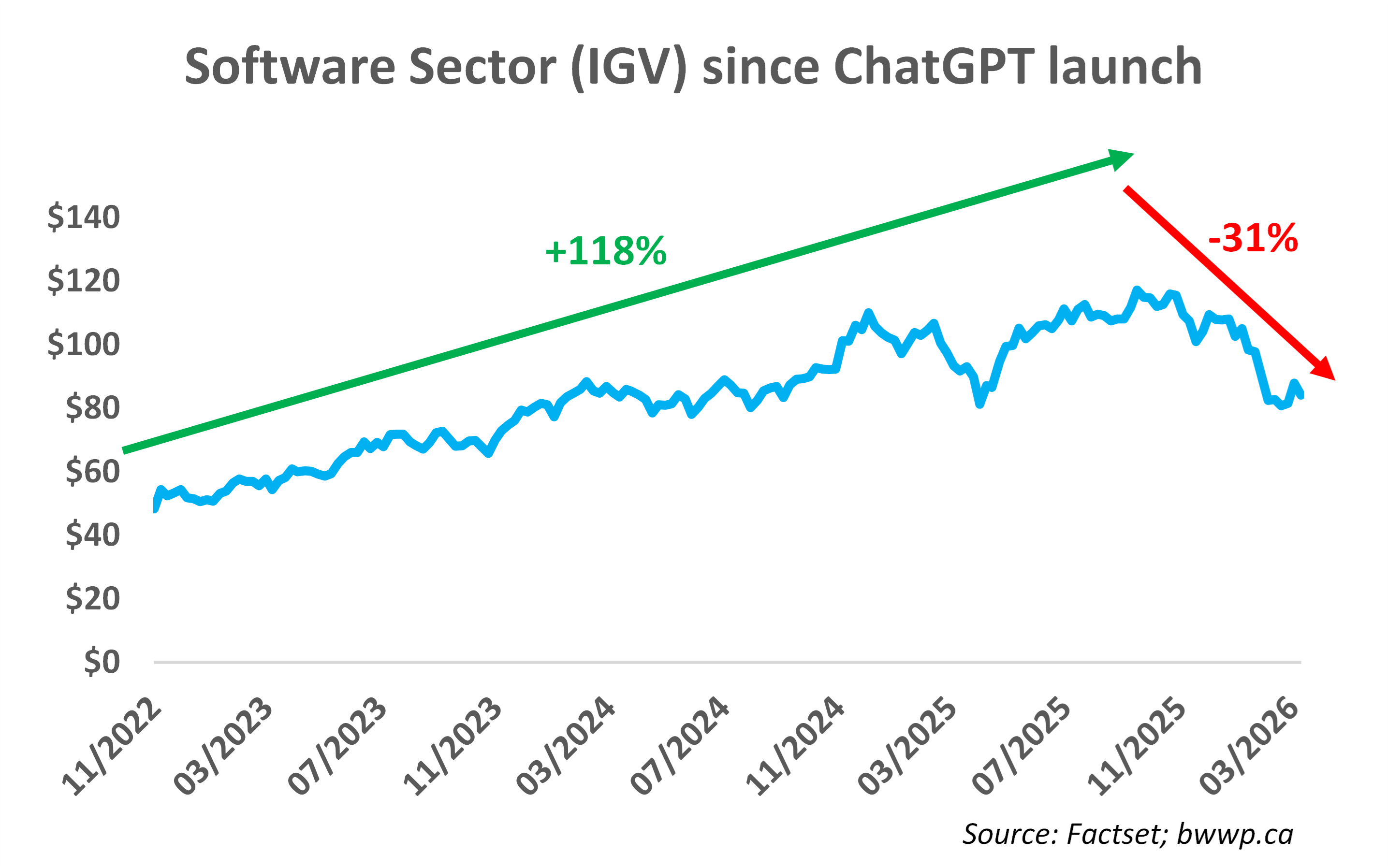

The main driver of revenue in the software sector is via seat licenses. The more people employed within various enterprises, the more demand there is for software on these new employee’s desktop computers. ChatGPT went live in late 2022. For the first 18-months or so after its launch, software was viewed as an AI-beneficiary on the thesis that AI would increase enterprise software spending via more employment and more seat licenses.

But as you can see from the chart, this thesis began to shift in the back half of 2025, culminating earlier this year with the launch of Anthropic's Claude Cowork tool - an agentic AI platform explicitly designed to automate workflows in sales, legal, and financial analysis.

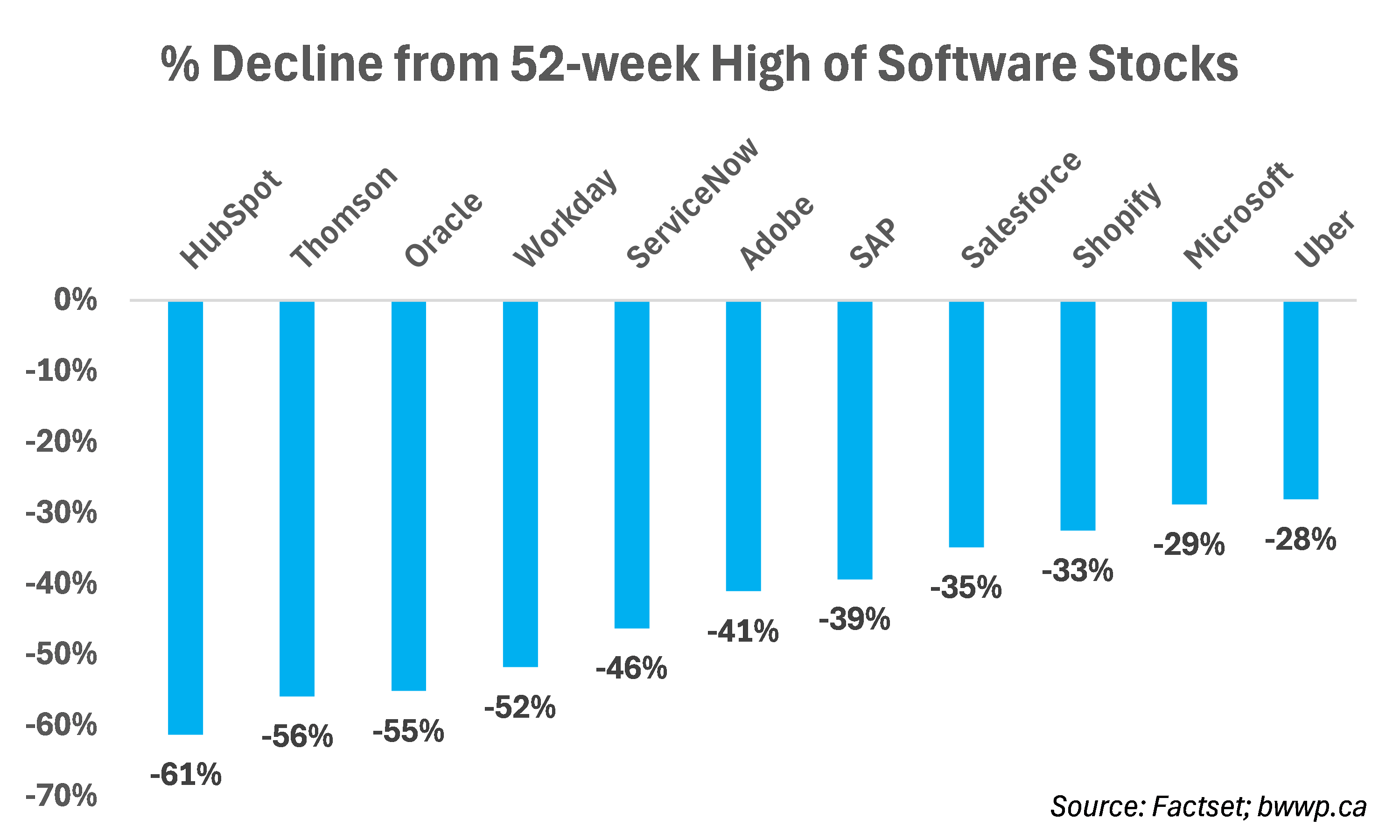

As a result, the enterprise software sector is experiencing its most severe share repricing since the dotcom bust of 2000–2002 — and it is happening in slow motion rather than overnight. Unlike the dot-com crash, which was driven by companies with no earnings, no revenue, and speculative business models, today's software selloff is hitting highly profitable, cash-generative businesses with deeply entrenched enterprise relationships and real, recurring revenue. That distinction matters enormously for the investment thesis, even as it does nothing to stop the share price pain.

The catalyst is a challenge to the premise of the entire “Software as a Service” (SaaS) era: if AI agents can perform the cognitive work that human employees currently do — and that enterprise software currently enables — then the per-seat license model on which $2 trillion in software market capitalization is based may be permanently impaired. This is not a question of whether or not individual companies will grow revenues. It is a question of what those revenues are worth if the number of human "seats" they can charge for shrinks.

The fundamental issue is not that software companies are becoming worthless - it is that their pricing model is becoming obsolete. For two decades, SaaS was built on a beautifully simple equation: more employees = more seats = more revenue. AI breaks this equation. If one AI agent can do the work of ten customer service representatives, a company needs one “software” seat, not ten.

How will this play out from here?

While the launch of upgraded agentic AI technology has sent a chill through the software sector, we have yet to actually see any real impact on their business models. Revenue growth is still strong and the CEOs from these various businesses have argued that AI will be additive to their models rather than something to be feared.

Rather, what we have seen in the past six months or so is an enormous valuation reset with the sector collectively going from price-to-sales (P/S) multiples of 12–18x - levels that assumed perpetual double-digit revenue growth and expanding seat counts – to P/S multiples of 4–6x - levels that assume much slower growth if not outright declines in their businesses.

Goldman Sachs strategist Ben Snider likens this to the newspaper/tobacco sectors: industries where disruptive technology – the Internet for print newspapers - or regulation – tobacco -caused prolonged share price declines, with equity value significantly impaired before earnings recovered. This is the bear case. In newspaper stocks, share prices fell 95% between 2002 and 2009 as internet advertising cannibalized print revenue. By the time print newspapers found new business models, most of the equity value was gone.

But we believe the analogy has important limits. Enterprise software is not advertising-dependent media. It is deeply embedded in mission-critical business processes, subject to multi-year contracts, regulatory compliance requirements, and switching costs that took years to build. Will the Royal Banks or JP Morgans of the world be willing to hand over the keys of their enterprises to agentic AI and give up their relationships with various CRMs? Maybe in the long-term, but these decisions are likely to take years and require a significant amount of handholding, considering how entrenched and trusted many of their SaaS partners have become.

While we are not yet brave enough to call a bottom in SaaS stocks, the valuation reset has been profound. Although we would not call these stocks “cheap”, their current multiples suggest significant impairment that is not yet supported by any real data. Yes, AI is scary and potentially disruptive to their business models, but there is a pathway in which some of these businesses build AI into their software and it ultimately expands their businesses as opposed to hinders them.

Okay, that’s enough for this week. Next week, we will wrap it all up with our forecast as to how this is likely to play out over the next decade.