Inflation shock dissipating

Aside from China, inflation soared to multi-decade highs across most major economies in 2022. Even though inflation is still too high for the liking of many central banks, there is mounting evidence that price pressures have peaked. Recent inflation reports in the U.S. and Canada revealed that price increases have been smaller and less broad-based. Meanwhile, lower crude oil prices, easing supply-side constraints, and softening consumer/business demand all suggest to us that inflation’s direction of travel should stay on an improving trend.

Nevertheless, some aspects of recent inflation data caution that inflation’s descent towards pre-pandemic levels, which were consistent with central bank targets, could be a long and winding one. Signs that drivers of core inflation are transitioning from goods to services, together with still-robust wage gains, raise the prospect that prices could prove “stickier” at a higher level for longer than expected. In our view, the degree to which inflation subsides and to what level over the coming year will largely hinge on whether goods prices continue to deflate, when and how much shelter (housing and rent) costs cool, and to what extent labour shortages alleviate.

A period of disinflation likely on the way

But the forces fueling inflation may be shifting towards stickier services components

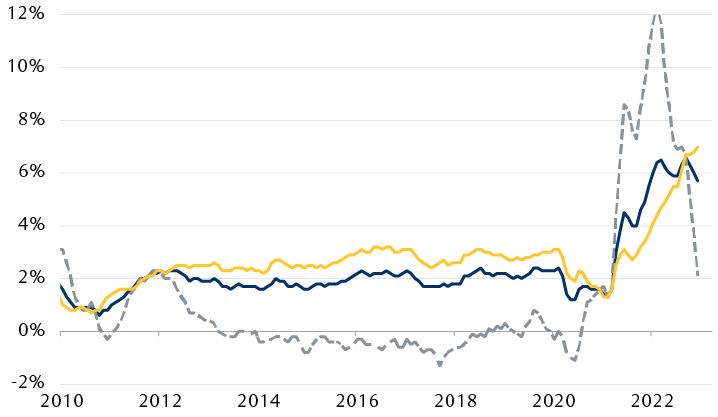

Line chart showing U.S. Core Consumer Price Index (CPI), Core Goods CPI and Core Services CPI on a year-over-year basis since 2010. Softening demand for goods, lower energy prices and easing supply-side constraints suggest inflationary impulses have likely peaked, but forces fueling inflation may be shifting towards stickier services components, which are now running at a higher level of inflation than goods in aggregate on a year-over-year basis.

Source - RBC Wealth Management, Bloomberg; data through 12/31/22

Smaller rate hikes ahead

The synchronized interest rate hikes implemented by many central banks in 2022 reflected a concerted effort to combat persistently high inflation. With price impulses finally showing signs of abating and economic momentum fading, we believe that monetary policy seems to be edging closer to a turning point.

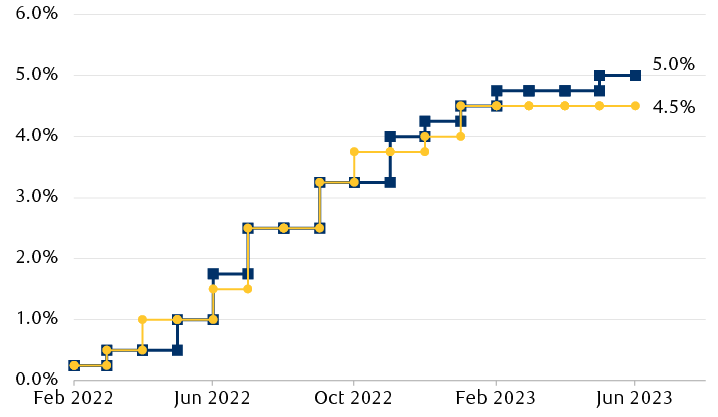

After delivering a series of outsized rate increases last year, both the Fed and Bank of Canada have hinted at the possibility of downsizing rate moves at future policy meetings. For the most part, this is already embedded in market-implied projections which now anticipate policy rates in Canada and the U.S. to rise by a more modest 50 basis points over the next two quarters to reach a cycle peak of around 4.5 percent to five percent by June.

Interest rate expectations

Line chart showing the path of benchmark interest rates in the U.S. and Canada from February 2022 to December 2022 and market expectations thereafter until June 2023. After delivering a series of outsized rate increases last year, both of the Fed and Bank of Canada have hinted at the possibility of downsizing rate moves at future policy meetings. Market-implied projections now anticipate policy rates in Canada and the U.S. to rise by a more modest 50 basis points over the next two quarters to reach a cycle peak of around 4.5%–5% by June.

Source - RBC Wealth Management, Bloomberg; data through 1/6/23

Inflation’s trajectory remains the key wildcard. If the nascent retreat in inflation can be sustained over the next few months, this could allow policymakers to not only scale back the pace of rate hikes but also to eventually pause their tightening campaigns, perhaps in the first half of this year. This, alongside a decelerating economy, could help temper upward pressure on bond yields.

Late cycle vibes

Turning to the economy, global growth has slowed sharply over the past year under the strain of tightening financial conditions as a result of higher borrowing costs, more stringent lending standards, and a stronger U.S. dollar. Setting the tone for the rest of the world, the U.S. economy is likely to confront a downturn this year, with a range of economic and financial indicators monitored by RBC Global Asset Management conveying that the U.S. is most likely at the late or end stage of the business cycle. To be clear, recent economic releases continue to point towards resiliency in consumer spending and the labour market, and broadly remain consistent with an economy in an expansion phase.

However, as we pointed out in the focus article from the Global Insight 2023 Outlook, a U.S. recession will likely arrive in the year ahead. This view is mainly predicated on the cautionary signals issued by two of the most historically reliable leading recession indicators, namely the position of short-term interest rates compared with that of long-term rates (also known as the “shape of the yield curve”) and the Conference Board’s Leading Economic Index. These two indicators—with historical average lead times of six to 12 months—signaled back in July and September that a U.S. recession is likely on the way, potentially arriving as soon as this summer.

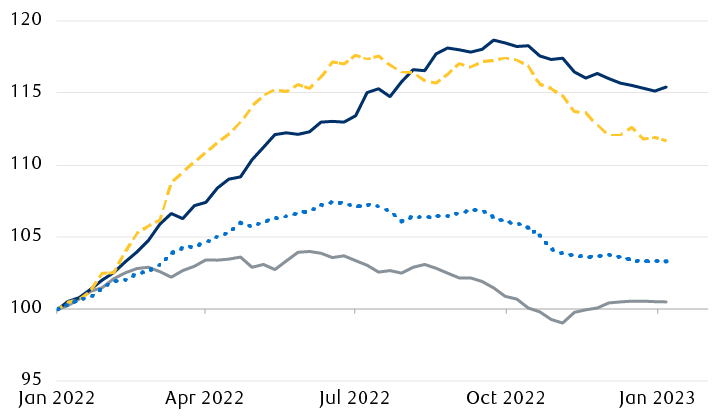

Consequently, we believe corporate fundamentals will be challenged by worsening macro conditions. Given notably slower economic growth and higher cost structures, our sense is that consensus earnings expectations may need to be revised lower to reflect the reality of a meaningfully less favourable operating environment for revenues and margins. We are also mindful that recessions have usually been accompanied by substantial declines in corporate profits, a key reason why every U.S. recession has been associated with an equity bear market.

Profit estimates likely to see downward revisions

Consensus forward 12-month EPS estimate (Jan. 1, 2022 = 100)

Line chart showing the evolution of consensus forward 12-month EPS estimates for the MSCI All Country World Index, the S&P 500, the STOXX Europe 500 Index and the TSX Composite. The corporate earnings outlook has exhibited resilience, but given notably slower economic growth and higher cost structures, our sense is that earnings expectations will need to be revised lower to reflect the reality of a significantly less favourable operating environment for revenues and margins in the near term.

Source - RBC Wealth Management, Bloomberg; data through 1/6/23

Investment implications

Navigating a late-cycle environment against a backdrop of elevated uncertainty around recession risk, inflation, and monetary policy is a formidable task. The lagged growth-dampening effects of synchronized monetary tightening around the world will continue to percolate through major economies in the quarters ahead, in our view. Although we take some comfort in the fact that most asset markets are entering 2023 on improved valuation grounds, we believe that nagging headwinds emanating from increasingly restrictive borrowing costs, shrinking liquidity, and corporate earnings vulnerability means this is not an environment particularly conducive for assertive risk-taking.

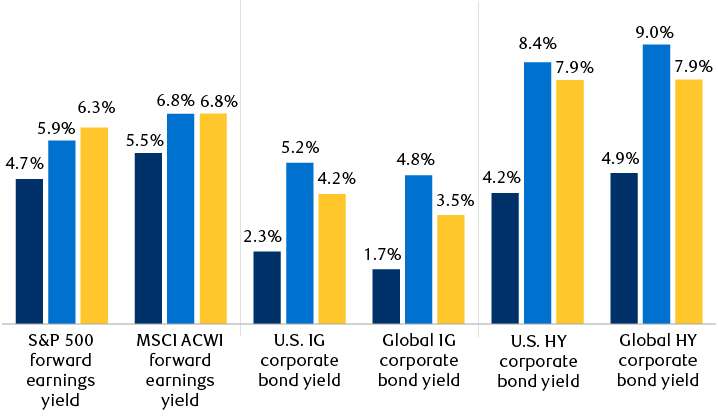

Risk premiums look more attractive across major asset classes

Relative value has shifted in favour of fixed income

Column chart showing the current forward earnings yield for the MSCI All-Country World Index and the S&P 500 and the yield to worst for the Bloomberg U.S. Corporate Index, the Bloomberg Global Agg Credit Index, the Bloomberg U.S. Corporate High Yield Index and the Bloomberg Global Corporate High Yield Index, compared to a year ago and the average since 2002. On a relative basis, the yield advantage that equities commanded over corporate bonds has sharply diminished over the past year.

Note: Earnings yield is the inverse of the forward price-to-earnings ratio. Bond yield refers to yield to worst for the Bloomberg U.S. Corporate Index, the Bloomberg Global Agg Credit Index, the Bloomberg U.S. Corporate High Yield Index, and the Bloomberg Global Corporate High Yield Index.

Source - RBC Wealth Management, Bloomberg; data through 1/6/23

From a cross-asset perspective, we believe it is sensible to take a relatively more constructive stance on fixed income securities, where the opportunity set across corporate credit markets has expanded considerably. With many segments offering attractive all-in yield (return) profiles, we believe corporate bonds are reasonably well cushioned against further spread widening and rate increases before returns turn negative. We see the balance of risks as favouring higher-quality bonds in the short-to-intermediate term that lock in improved yields today, but without taking on excessive interest rate risk should inflation prove to be more stubborn than expected. While valuation risk in equities has diminished following the selloff last year, the heightened likelihood of a U.S. recession leads us to maintain a defensive posture and we believe equity portfolios should lean more heavily towards quality and sustainable dividends and away from individual company risks that may come home to roost in an economic downturn.