Since its introduction in 2009, the Tax-Free Savings Account (TFSA) has continued to grow in popularity as a registered savings plan option, with recent Government of Canada data showing that over half of eligible Canadians have one.1 At the same time, however, not all TFSA holders regularly contribute to their TFSAs or maximize the range of potential benefits it offers.

As a flexible savings vehicle that provides tax-free income and growth, anytime withdrawals and the ability to carry forward contribution room, a TFSA can be effective for a wide range of short-term and long-term financial goals. For saving and investing throughout your lifetime and providing a source of income in retirement, a TFSA can be used as a complement within your overall financial plans.

Here’s an overview of six potential strategies or aspects to give thought to in maximizing the use of your TFSA.

Optimizing investments within your TFSA

While the name itself highlights the TFSA as a “savings account,” the tax-free aspect specifically relates to the income or growth of investments held within the account. With that in mind, it’s important to look at how you invest your contributions. If you were to simply hold funds in your TFSA and not invest them, you would miss out on the tax benefits associated with growth and income inside the account.

In a TFSA, any income (including capital gains) earned is exempt from tax, and TFSAs can hold a wide variety of investments, including guaranteed investment certificates (GICs), bonds, stocks and mutual funds. And, while there may be a tendency to think of a TFSA more as a shorter-term savings vehicle, depending on your needs and circumstances, shifting the focus to use it more for longer-term saving may broaden the range of options that can positively impact growth potential.

Additionally, in times of market volatility, it may be a good opportunity to revisit your investment types or how you’re diversified. You may want to consider investing in fixed-income securities inside of your TFSA. Because fixed income isn’t taxed efficiently in a non-registered account, it may be beneficial to hold these types of investments in your TFSA.

Creating an emergency fund

Having funds set aside in case of an emergency, unexpected life event or significant change in your circumstances is an important part of financial planning. With the impacts of the COVID-19 pandemic, the importance of this has been heightened even more. For some, the TFSA may be an effective option for creating an emergency fund, because it’s possible to withdraw assets (both your original contributions and growth/income) at any time, whenever you need them, tax-free.

To help in determining what may be appropriate to set aside, RBC offers an Emergency Fund Calculator, which can be accessed by visiting The Savings Spot.

As a general rule of thumb, it’s recommended to have three to six months’ salary set aside in an emergency fund. You may want to give some thought to this amount and what makes sense for your personal circumstances and if you have children, for example.

If you do use your TFSA to create or hold an emergency fund, keep in mind that because these funds may be needed urgently, you may want to consider investing in more secure, less volatile interest-earning securities.

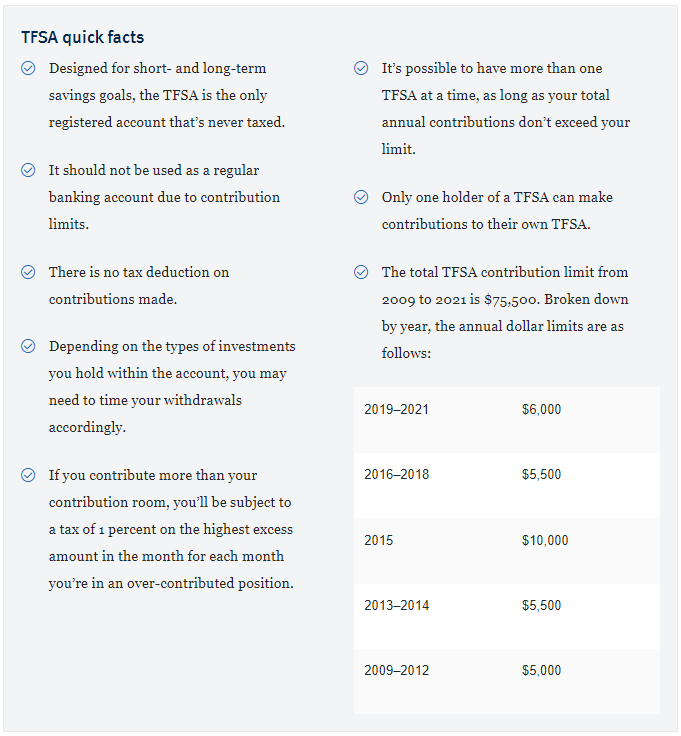

Being mindful of your contribution room

With TFSAs, there are pre-determined annual contribution limits. For Canadian residents, your contribution room starts to accumulate when you become age 18 (or starting in 2009, whichever occurred last), even if you haven’t opened a TFSA or filed an income tax return to earn contribution room. Note: In certain provinces and territories, the age of majority is 19. In these jurisdictions, a person who’s 18 will accumulate TFSA contribution room for the year, but won’t be able to open the TFSA until they reach the age of majority.

If there’s a situation where you haven’t used or don’t use your contribution room in a particular year, that unused room can be carried forward to any future year. In other words, if you have accumulation room and you haven’t always contributed the maximum amount to your TFSA, in times when you have funds available and it makes sense in conjunction with your other savings approaches or plans, it may be possible to take advantage of your accumulated contribution room for increased growth potential. A withdrawal made in a given year is added to contribution room the following year.

Also, unlike a Registered Retirement Savings Plan (RRSP), there’s also no set age limit on your ability to contribute and there’s no lifetime limit on the amount you can contribute.

When you make any contribution to your TFSA, keep in mind that your contribution room will decrease, even if it’s a re-contribution of funds you withdrew in previous years. And if you’ve reached your maximum contribution limit for the year, that room won’t be restored until the following calendar year.

Strategizing with income splitting

If your family is in a situation where one spouse or parent is a high-income earner, you may be able to benefit from income splitting opportunities using the TFSA, either by gifting funds to your spouse or to your adult child.

Say you’re the higher-income spouse and you provide funds to your lower-income spouse to contribute to their TFSA. In this scenario, the attribution rules won’t apply, so any income or capital gains earned on those funds while they are held in the TFSA won’t be attributed back to you (as long as the contribution doesn’t result in, or add to, an over-contribution).

With this approach, both you and your spouse can earn tax-free investment income and growth, irrespective of which spouse provided the funds. In other words, you may be able to boost the amount of your combined investments that can grow tax-free.

If you gift funds to a child who’s 18 or over, they can use these funds to contribute to their own TFSA. (It’s important to remember that in some provinces or territories, you must be 19 or older to open a TFSA.) This type of gifting may be a good income-splitting strategy to consider when you’ve maxed out your own TFSA contribution room and have excess non-registered funds. Again here, the attribution rules won’t apply to income and capital gains earned on the gifted funds, so they can grow tax-free in your child’s hands to be used in the future.

Keep in mind, however, that once you make the gift, you’ll give up control over those funds, how they’re invested (you can’t make a gift contingent on the recipient putting the funds into a TFSA), when and how much is withdrawn, and how the funds are used.

Saving and generating income in retirement

Some may not realize there are many potential benefits a TFSA offers for retirees. If you’ve retired but have excess cash flow, a TFSA may be a good option to continue building your savings. And because of the flexibility this savings vehicle offers, you can withdraw funds when you need them and re-contribute them without the tax consequences in the following year.

If you’re retired and no longer have earned income that will generate new RRSP contribution room, a TFSA provides a savings opportunity in that regard as well. And because there aren’t age limits, even after the end of the year you turn age 71 — when you can’t contribute to your RRSP anymore — you’ll be able to preserve some tax-free growth and income. You also won’t need to convert your TFSA to an income vehicle like you have to with an RRSP based on your age.

Lastly, a TFSA may be used as another source of tax-efficient retirement income if you think you may be in the same or a higher marginal tax bracket in retirement. Unlike withdrawals from an RRSP or Registered Retirement Income Fund (RRIF), which are fully taxed at your marginal tax rate, withdrawals from a TFSA are not taxable.

Complementing your existing registered savings plans

If you have an RRSP or Registered Education Savings Plan (RESP), depending on your circumstances and life stage, a TFSA may help augment your savings in combination with your other registered plans. For example, if you make a contribution to your RRSP and receive a tax refund, you may want to consider using that refund to contribute to your TFSA. By doing so, those funds will be set aside in a tax-sheltered way, helping you save for whatever financial goals you may have.

When it comes to saving for a child’s education, TFSAs can be used to accumulate funds in addition to an RESP, providing tax-sheltered education savings. By using your own TFSA for this purpose, you can also start investing long before your child is able to open their own account, and when the funds are ultimately needed, you can withdraw them tax-free.

References

- Government of Canada. Tax-Free Savings Account Statistics. Accessed September 2020. https://www.canada.ca/en/revenue-agency/programs/about-canada-revenue-agency-cra/income-statistics-gst-hst-statistics/tax-free-savings-account-statistics/tax-free-savings-account-statistics-2017-tax-year.html

This document has been prepared for use by the RBC Wealth Management member companies, RBC Dominion Securities Inc.*, RBC Phillips, Hager & North Investment Counsel Inc., RBC Global Asset Management Inc., Royal Trust Corporation of Canada and The Royal Trust Company (collectively, the “Companies”) and their affiliate, Royal Mutual Funds Inc. (RMFI). *Member – Canada Investor Protection Fund. Each of the Companies, RMFI and Royal Bank of Canada are separate corporate entities which are affiliates. “RBC advisor” refers to Private Bankers who are employees of Royal Bank of Canada and licenced representatives of RMFI, Investment Counsellors who are employees of RBC Phillips, Hager & North Investment Counsel Inc. and the private client division of RBC Global Asset Management Inc., Senior Trust Advisors and Trust Officers who are employees of The Royal Trust Company or Royal Trust Corporation of Canada, or Investment Advisors who are employees of RBC Dominion Securities Inc. In Quebec, financial planning services are provided by RMFI which is licenced as a financial services firm in that province. In the rest of Canada, financial planning services are available through RMFI, Royal Trust Corporation of Canada, The Royal Trust Company, or RBC Dominion Securities Inc. Estate and trust services are provided by Royal Trust Corporation of Canada and The Royal Trust Company. If specific products or services are not offered by one of the Companies, clients may request a referral to another RBC partner. The strategies, advice and technical content in this publication are provided for the general guidance and benefit of our clients, based on information believed to be accurate and complete, but neither the Companies, RMFI, nor Royal Bank of Canada, nor any of its affiliates nor any other person can guarantee accuracy or completeness. This publication is not intended as nor does it constitute tax or legal advice. Readers should consult a qualified legal, tax or other professional advisor when planning to implement a strategy. This will ensure that their individual circumstances have been considered properly and that action is taken on the latest available information. Interest rates, market conditions, tax rules, and other investment factors are subject to change. This information is not investment advice and should only be used in conjunction with a discussion with your RBC advisor. None of the Companies, RMFI, Royal Bank of Canada nor any of its affiliates nor any other person accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or the information contained herein. In certain branch locations, one or more of the Companies may carry on business from premises shared with other Royal Bank of Canada affiliates. Notwithstanding this fact, each of the Companies is a separate business and personal information and confidential information relating to client accounts can only be disclosed to other RBC affiliates if required to service your needs, by law or with your consent. Under the RBC Code of Conduct, RBC Privacy Principles and RBC Conflict of Interest Policy confidential information may not be shared between RBC affiliates without a valid reason.

® / TM Trademark(s) of Royal Bank of Canada. RBC Wealth Management is a registered trademark of Royal Bank of Canada. Used under licence. © 2021 Royal Bank of Canada. All rights reserved. Printed in Canada.