Financial Markets Monthly - April 2020

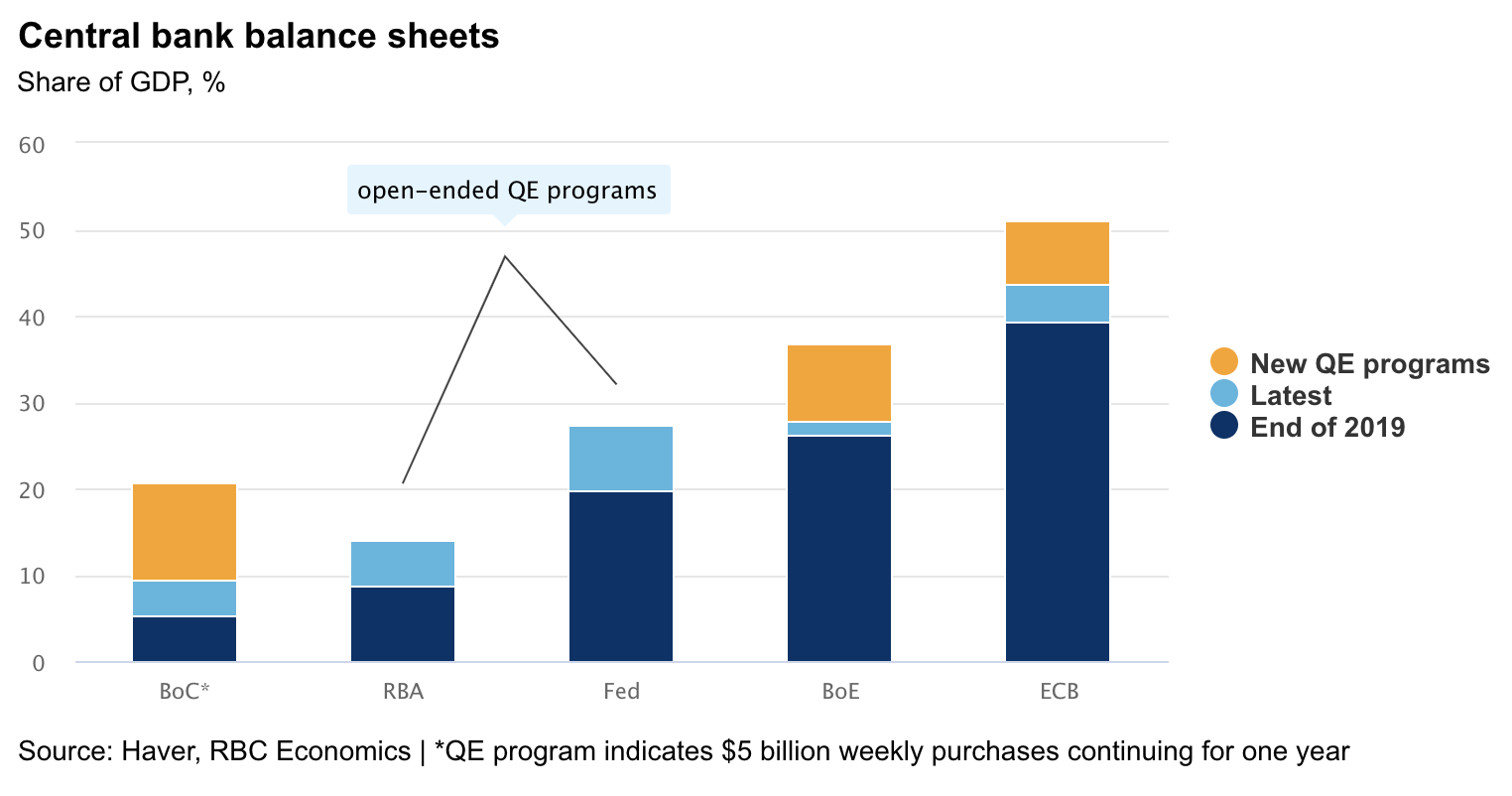

The response from fiscal and monetary authorities has been unprecedented in its size and speed. Central banks have cooked up an alphabet soup of liquidity and lending programs to alleviate stress and improve the flow of credit to businesses. Governments have pledged billions in direct support for businesses and households and even more in loan guarantees. We think the policy support unveiled thus far will prevent a worst case scenario and underpin an eventual recovery. Already, it’s inspired a moderate rebound in equity markets in the last two weeks. Oil prices, too, are up from their recent lows on the prospect of coordinated supply cuts. But the near term economic hit will still be dictated by the scale, duration and effectiveness of containment measures. After what will likely be record declines in the second quarter, we are projecting a sizeable rebound in GDP over the second half of the year, though all of the economies we track are expected to close the year with significantly more slack than they entered with.

Highlights:

- Our projections now assume current shutdowns and social distancing policies will remain in place for at least another two months and will only gradually be scaled back in June and July.

- In both Canada and the US we think GDP declines in Q2 will exceed 30% on an annualized basis.

- Based on claims for employment insurance and other benefits, Canada’s unemployment rate is likely nearing 20% and the US rate is also most likely in double digits.

- In the UK and euro area, we are expecting similar declines in economic activity over the first half of the year—nearly 20% on an average, annualized basis.

- The significant fiscal support announced (generally 2-5% of GDP, and in some cases even more) will prevent a worst case scenario from materializing, and underpin an eventual economic recovery. But we don’t think it will be the hoped-for V-shaped recovery—that is, a quick and nearly full rebound in activity.

Josh Nye is a senior economist at RBC. His focus is on macroeconomic outlook and monetary policy in Canada and the United States. His comments on economic data and policy developments provide valuable insights to clients and colleagues, and are often featured in the media.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.