Despite central banks’ efforts to tame it, inflation remains elevated in North America, while economic growth has begun to stall, especially in Canada. These conditions raise the threat of a sustained period of high and increasing prices and low or even negative growth in the months ahead. And this real and present threat of “stagflation” is hitting the economy and investment markets hard, punishing bond prices through rising yields and stock prices over worries of falling profits. The term combines “stagnant” with “inflation” – and here’s what you need to know about it, and four tips to mitigate its impact.

Inflation inflammation

As the economy transitioned through and past the COVID pandemic, demand for goods, and then eventually services, skyrocketed over 2021 and 2022. In the wake of reopening economies across the globe, the pull of surging demand strained global supply chains, and geopolitical events exacerbated the issue. In response, prices and inflation soared, forcing central banks to raise interest rates to quell demand, in turn increasing the threat of an economic slowdown – or even recession.

Ongoing “stagflationary” conditions impact investors too, by affecting both bond and stock markets:

- Bonds: When investing in new bonds, investors now receive higher interest rates. On the other hand, the market value of their existing bonds, because they pay lower interest rates, is down. That’s less of a concern for investors simply holding their bonds to maturity – they can expect their principal to be fully repaid. But it’s more of a concern for investors investing in funds which trade bonds before maturity at prevailing market values.

- Stocks: Stocks can also be affected, as investors increasingly anticipate companies will struggle to generate sustained profits in these challenging conditions, as inflation drives up costs and reduced spending lowers revenues.

Sticking the landing – aiming for soft, bracing for hard

Unfortunately, the accepted remedy to tame inflation often adds to investors’ pain, at least in the short run. In response to rising prices, central banks have had to raise interest rates, in turn increasing borrowing costs for businesses and consumers, and further crimping their dwindling resources. While this can stifle demand and gradually inflation, it can also stifle economic growth. If the central banks cause a recession, especially a painful one, that’s called a “hard landing.” If they manage to finesse a slowdown but it doesn’t result in a recession – or at least a prolonged and nasty one – that’s called a “soft landing.”

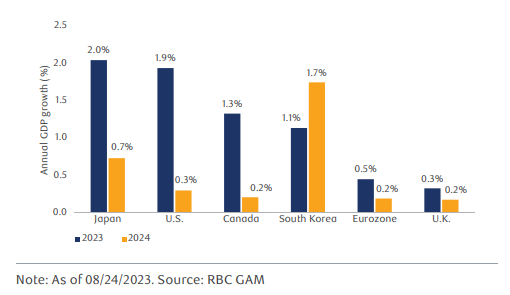

Bumpy road ahead: Global GDP outlook for 2024

Fortunately, there is still time for central bankers to engineer a soft landing and avoid a hard one, and a recession, especially a painful one, is not a forgone conclusion – but in Canada, the evidence continues to point to a recession on the horizon, if not one already underway.

Stagflation mitigation

Here are four steps to consider to help mitigate the impact of stagflation:

- Debt: If borrowing costs are rising, it can be timely to review your debt service costs, and to consider reducing debt or deferring purchases that may increase it. Increasing mortgage terms or disposing of debt-laden assets can also reduce the strain on cashflow.

- Investment portfolio: The market’s negative response to stagflation and rising interest rates can provide a “stress test” and an opportunity to review your portfolio with us to determine whether it requires any rebalancing. Taking advantage of lower asset prices can also be a smart strategy when markets are stressed.

- Quality: In times of economic and market stress, certain types of assets tend to perform better –or “less bad” – than others. A focus on assets that are considered high quality – such as blue-chip stocks and investment-grade corporate debt – because they can more consistently perform through challenging economic circumstances can help reduce volatility.

- Fixed income: As central banks have rapidly increased interest rates, the bond market has seen yields soar and prices fall. On the positive side, fixed-interest-rate investments (e.g., GICs) tend to see their returns rise, while newly higher yields on bonds offer the opportunity to “reset” coupon payments at higher levels, and creating the opportunity to enhance fixed-income returns over the longer term.

If you have questions about stagflation and how to mitigate its impact on your portfolio and investment plan, speak to us today.

This information is not intended as nor does it constitute tax or legal advice. Readers should consult their own lawyer, accountant or other professional advisor when planning to implement a strategy. This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that action is taken on the latest available information. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / TM Trademark(s) of Royal Bank of Canada. Used under license.