Reallocating Your Wealth: taking a look at pools of capital

We all have the same traditional pools of capital, within which to accumulate and invest our wealth and draw income – pension, registered and non-registered assets. Within the non-registered option there are such vehicles as equities, fixed income and mutual funds. Proper diversification and consideration of your wealth may help you to achieve your lifestyle needs/bequests and philanthropic planning desires in a tax-efficient manner than may ultimately enhance your overall wealth.

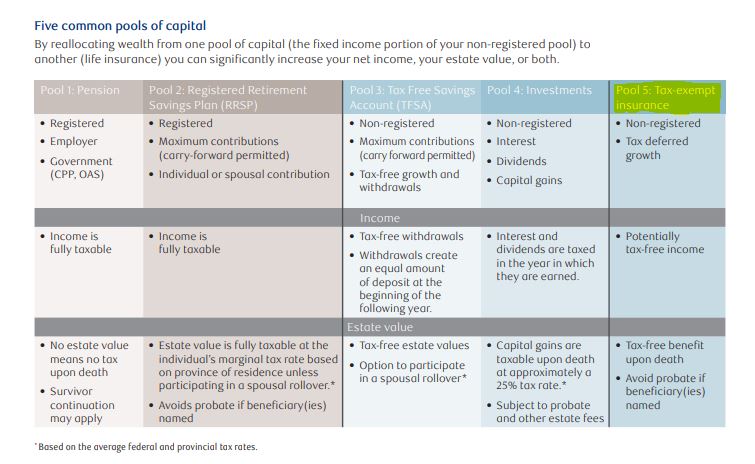

Five common pools of capital

Pool one: your pension from government, your employer or both

- Income is taxable while you live, but there is no residual estate value, and therefore no taxes payable at death.

Pool two: your registered investments

- A tax-effective way of building wealth for your retirement

- Limited by the minimum and maximum deposits and withdrawals allowed by the Canada Revenue Agency.

- Must mature by age 71, at which time taxable income is withdrawn unless participating in a spousal/other rollover.

- Estate value is fully taxable resulting in the loss of approximately 50% of those assets, depending on your provincial marginal tax rate.

Pool three: tax-free savings

- This is often the next option after maximizing your registered contributions.

Pool four: your non-registered investments

- Interest and foreign dividends: the full amount received will be taxed at your marginal rate.

- Canadian dividends: Eligible dividends have an effective marginal tax rate of 34%. Ineligible dividends are taxed at approximately 44%.

- Capital gains: 50% of any capital gains realized are included in your taxable income and taxed at your marginal tax rate.

Pool five: tax-exempt insurance

- This pool is tax-exempt life insurance. Similar to your RRSP, the contributions you make to a tax-exempt life insurance policy are limited.

- However, there is much more flexibility with respect to maximum deposits.

Tax-exempt life insurance is a tremendous tool for asset accumulation and wealth preservation. It can also enhance your portfolio since it adds a layer of diversification to your investments. It works by allocating deposits above the life insurance minimum premiums payable within a variety of different investments. This has the ability for tax-exempt growth over your lifetime.

Not only can tax-exempt life insurance significantly enhance the overall value of your portfolio – because the growth is not taxable. The tax-free death benefit can be used to pay the tax payable on your other pools of capital upon death. Additionally, all proceeds are tax-free at death and go directly to your named beneficiaries.

Tax-exempt life insurance can also be used to enhance your retirement income by complementing what you’ve saved in your RRSP and TFSA. You can employ a unique strategy that utilizes annual tax-free bank loans. By transferring a portion of your wealth every year into this solution, you not only gain access to a tax shelter, you purchase an immediate and significant benefit for your estate. The immediate benefit is the insurance coverage and you continue to maintain some degree of liquidity.

In the event of your death, the bank loan is paid from your policy and the remainder of the funds from the insurance policy is paid tax-free to your named beneficiaries.

To learn more, reach out to Stephanie Woo at 604.257.3234 or stephanie.woo@rbc.com and she will provide you with personalized advice and review these options with you and those you care about.