Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can catch up on the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q1 2026 edition covers Market Review for the year 2025, some long-term themes that drive investments, and how to achieve a balanced approach to wealth and health. Shiuman’s Corner covers the books I read last year.

Markets

Market scorecard as of close on Friday February 13, 2026.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 33,074 | 2.2% | 4.3% |

| U.S. | S&P 500 | 6,836 | -1.2% | -0.1% |

| U.S. | NASDAQ | 22,547 | -1.8% | -3.0% |

| Europe/Asia | MSCI EAFE | 3,117 | 2.9% | 7.7% |

Source: FactSet

- TSX closed sharply higher afternoon in Friday midday trading near best levels. Most sectors higher. Materials the best performer. Canadian equities posted 1.9% weekly gain.

- US equities finished mostly higher in Friday trading, with major indices giving up some midday strength into the close. However, breadth was positive and the equal-weight S&P logged solid gains. Major indices were down for the week.

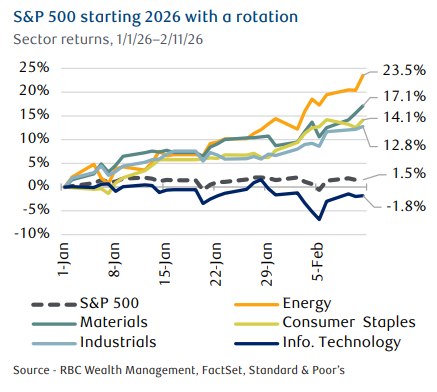

- Financial markets continue to navigate competing forces from corporate earnings, investor sentiment and economic data. We share our perspectives on recent volatility in technology stocks.

- Artificial intelligence (AI), a key driver of equity market trends, has recently been a source of volatility. Across the technology sector, concerns about AI-related disruption alongside rising expectations for tangible returns on AI spending have led to sharp share price swings in both U.S. and Canadian markets.

- We remain constructive on the AI theme over the long term but recognize that transformative technologies often bring periods of volatility and elevated uncertainty.

ECONOMY

- Canada

- Bank of Canada Governor Tiff Macklem stated that interest rate cuts alone won’t solve Canada’s economic challenges, which stem from U.S. trade tensions, AI disruption, and slower population growth. He emphasized the economy is undergoing structural shifts requiring action from policymakers, businesses, and households—not just monetary policy. With modest 1.5% growth expected over two years, Macklem warned against misdiagnosing economic weakness as cyclical when it’s structural, cautioning that rate cuts risk fuelling future inflation.

- Statistics Canada’s Labour Force Survey showed employment declining by 25,000 in January, reversing cumulative gains of 189,000 over the previous four months. Despite the job losses, the unemployment rate fell unexpectedly to 6.5%. This decline was driven by fewer Canadians actively seeking work.

- Janice Charette -- who served as the clerk of the privy council twice and has nearly 40 years of experience – has been appointed Canada’s new chief trade negotiator with the U.S. The former high commissioner to the United Kingdom is stepping into the role with just a few months until the CUSMA review begins.

U.S.

- Six House Republicans joined Democrats in a 219-211 vote to repeal President Donald Trump’s tariffs on the U.S.’s northern trading partner. However, the House did not secure two-thirds of the votes necessary to override a veto from the President. The Senate had already passed a similar measure to cancel Trump’s tariffs on Canada. Democrats also unlocked a procedural move to force more votes, including on tariffs on Mexico and “liberation day” tariffs in the coming weeks. Markets are also waiting on a Supreme Court ruling on U.S. tariffs.

- Conflict with Iran drives energy stocks higher. An extra factor contributing to the rally in energy stocks is the escalating conflict between Iran and the United States. The U.S. and Iran are engaged in negotiations in Oman, with the U.S. looking for Iran to cease nuclear enrichment activities and ballistic missile development.

Further Afield

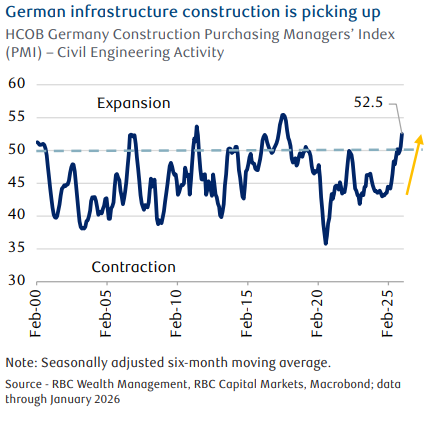

- Early evidence of Germany deploying its €500 billion infrastructure programme appeared in rising civil engineering activity, as measured by the sector’s economic activity index.

- Japanese voters handed Prime Minister Sanae Takaichi a powerful mandate, delivering her Liberal Democratic Party (LDP) and its coalition partner, the Japan Innovation Party (Ishin), a strong victory in the lower house election. Areas we expect to benefit under the strong LDP mandate include defense, AI semiconductors, and nuclear energy. We think consumer stocks should also benefit as private consumption potentially improves as the government weighs in on inflation.

Notes About Companies in Model Portfolio

- Fortis Inc. (FTS) released its 2025 fourth quarter and annual financial results. Net earnings attributable to common shareholders of $1.7 billion, or $3.40 per common share, for 2025 compared to $1.6 billion, or $3.24 per common share, for 2024. 4.1% increase in fourth quarter common share dividend achieving 52 consecutive years of common share dividend increases.

- Intact Financial (IFC) reported Q4 2025 financial results. Net operating income per share was up 12% to $5.50, driven by strong underwriting performance. Quarterly dividend increased by $0.14 (11%) to $1.47 per common share, maintaining a 10-year compounded annual growth rate of 10%

- Waste Connections (WCN) reported Q3 2025 results. Revenue in the third quarter totaled $2.458 billion, up from $2.338 billion in the year ago period. Net income in the third quarter was $286.3 million, or $1.11 per share on a diluted basis of 257.6 million shares.

Feel free to contact me with any questions and/or to discuss investment ideas.

Regards,

Shiuman

PS: To unsubscribe, simply reply with “Unsubscribe” in the subject line.