Below is a summary of some of the relevant news items from the Capital Markets and the Economy from the past week extracted from RBC Global Insights and FactSet Research.

You can catch up on the past four weeks’ Weekly Update in the link to my Blog.

Read my latest Smart Investor newsletter on my website. The Q1 2026 edition covers Market Review for the year 2025, some long-term themes that drive investments, and how to achieve a balanced approach to wealth and health. Shiuman’s Corner covers the books I read last year.

Markets

Market scorecard as of close on Friday January 23, 2026.

| Country | Equity Indices | Level | 1 week | YTD |

| Canada | S&P/TSX Composite | 33,145 | 0.3% | 4.5% |

| U.S. | S&P 500 | 6,916 | -0.4% | 1.0% |

| U.S. | NASDAQ | 23,501 | -0.1% | 1.1% |

| Europe/Asia | MSCI EAFE | 2,996 | 0.1% | 3.6% |

Source: FactSet

- TSX finished higher on Friday, a bit off best levels. Most sectors higher. Canadian equities up 0.3% on the week as materials strength again offset tech weakness.

- US equities finished mixed in Friday trading, ending off best levels. S&P and Nasdaq logged weekly declines. Big tech was mostly higher.

- The stock market also wobbled on the Greenland conflict. The S&P 500 fell 2.1% on Tuesday, during the holiday-shortened week, when tensions were most acute. However, stock prices recovered much of that lost ground thereafter as the situation de-escalated and the Q4 earnings season and economic data came back into focus.

- ECONOMY

- Each year heads of government, CEOs and a who’s who gather at Davos, a mountain resort in Switzerland. You can read a full report from RBC’s man on the ground here.

- You’re invited to an exclusive virtual client event with Senior Vice President and Chief Economist, Frances Donald, hosted by Kim Mason, Executive Vice President and Head of RBC Private Banking Canada. Thursday, February 12, 2026 at 3:00 p.m. – 4:00 p.m. PST.

-

- If you are interested, please register by February 11, 2026. A recording will be available to watch on-demand following the live event, but you’ll have to register. To register, click here.

- Canada

- Canadian headline CPI growth rose to 2.4% y/y in December, exceeding the consensus expectations of 2.2% y/y, which was also the prior month’s reading. However, the Bank of Canada’s (BoC) preferred core inflation measures—median and trimmed-mean CPI—showed signs of easing, coming in at 2.5% y/y and 2.7% y/y, respectively. On a three-month annualized basis, both measures declined significantly.

- Business confidence edged higher in Q4, according to the BoC’s quarterly Business Outlook Survey. Most exporting firms surveyed reported that they remained exempt from tariffs under CUSMA. However, industries heavily affected by tariffs, such as metals and automotive, continued to report weaker outlooks, highlighting ongoing sector-specific challenges.

U.S.

- The U.S. economy expanded in Q3 2025 due to stronger exports and less drag from inflated inventories. According to the Bureau of Economic Analysis, inflation-adjusted gross GDP increased at an annualized rate of 4.4%, the fastest pace in two years. Consumer spending—the main growth engine of the U.S. economy—advanced at a 3.5% annualized pace, reflecting strong services activity while spending on goods also accelerated from the prior quarter.

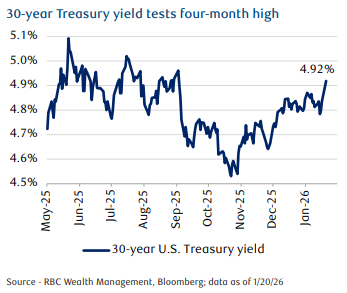

- In U.S. Treasury markets, while yields have increased across the entire curve this week, longer-dated maturities experienced the most selling pressure with 10- and 30-year yields testing their four-month highs.

Further Afield

- In Europe, the week was dominated by U.S. President Donald Trump’s threat to impose additional tariffs on eight European countries, including the UK, which had opposed his plan to annex Greenland, the Danish-controlled island. Though Western Europe weathered trade tensions surprisingly well last year, the transatlantic rift adds to uncertainty and is a potential headwind for the economy.

- Much of the focus the week has been on the extreme volatility in Japanese government bonds (JGBs) as Prime Minister Sanae Takaichi’s pledge to cut food taxes and her decision to call a snap election triggered a surge in long-end yields. Japan’s 40-year bond yield spiked as much as 27 basis points (bps) to 4.215%.

Notes About Companies in Model Portfolio

- The Procter & Gamble Company (NYSE:PG) reported second quarter fiscal year 2026 net sales of $22.2 billion, an increase of one percent versus the prior year. Organic sales, which excludes the impacts of foreign exchange and acquisitions and divestitures, were unchanged versus the prior year. Diluted net earnings per share were $1.78, a decrease of five percent versus prior year, due primarily to incremental restructuring charges in the current year. Core earnings per share were $1.88, in-line versus prior year.

Feel free to contact me with any questions and/or to discuss investment ideas.

Regards,

Shiuman

PS: To unsubscribe, simply reply with “Unsubscribe” in the subject line.